Shocking Changes Coming to Medicare Advantage in 2025: What You Need to Know

Medicare Advantage plans are changing dramatically in 2025, and if you’re a beneficiary you need to know about that. In this blog, you’ll learn about those changes, why we’re seeing so many insurance companies leave the market, and what all this means for you and your healthcare decisions. This information is critical to your understanding of your Medicare Advantage choices this year.

Table of Contents

- Shocking Changes Coming to Medicare Advantage in 2025

- What to Do if Your Plan is Terminated

- Provider Insights on Medicare Advantage

- How to Get Off a Medicare Advantage Plan

- Changing Your Medicare Supplement Plan

- Understanding Part D

- Navigating Medicare.gov

- Medicare Advantage Open Enrollment Period Explained

- FAQ

Shocking Changes Coming to Medicare Advantage in 2025

What You Need to Know Right Now

If you’re on a Medicare Advantage plan now or considering enrolling, the changes that come in to effect in 2025 are going to have a significant impact on your health care and how you access it. You’ll get an annual notice of change in the mail this fall that will spell out the exact changes. If you’re not vigilant, you may not realise the extent of these changes.

But many beneficiaries might not know that they can request such notifications via email, which they would likely miss if they were used to, say, getting their other updates in print form. And this year should be no exception: the changes are even more dramatic than in past years, and will affect tens of millions of people in this country.

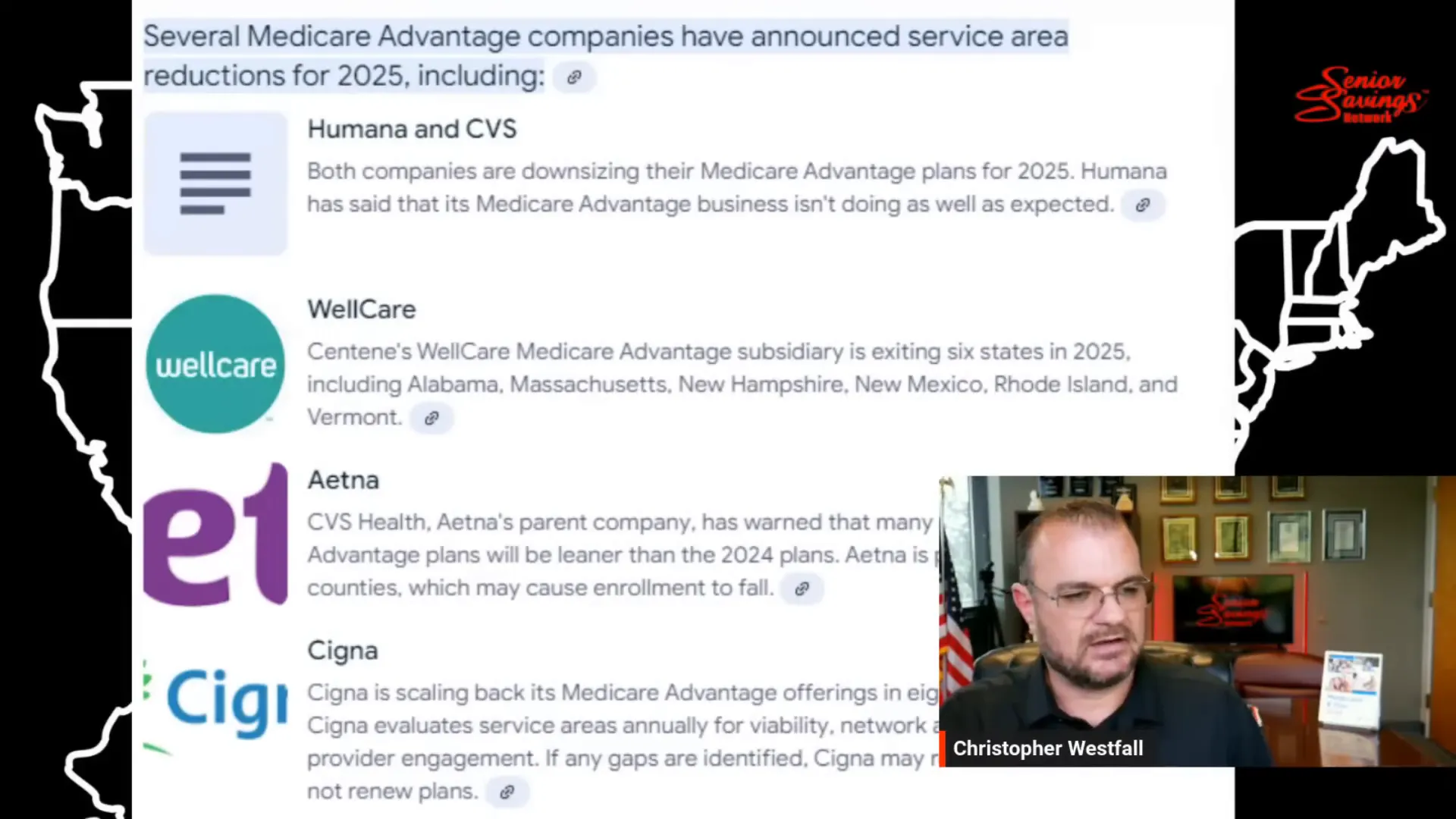

Why Are Insurance Companies Leaving Medicare Advantage?

Medicare Advantage losses are also driving insurance companies out of some markets. Humana said it would pull out of 13 markets next year, affecting up to 560,000 members. Mutual of Omaha is also getting out of the business, saying rising costs are causing it to withdraw from offering a stand-alone Part D drug plan.

Such decisions are often about profit. Insurers are pulling out of unprofitable markets, and many beneficiaries, if one plan suddenly disappears, might find they need to shop for a new one. Taken together, these developments suggest something alarming. A new MPCO dissolution is announced every 17 hours.

Medicare Advantage vs Original Medicare: Cost Comparison

It helps to have a handle on how the financial impacts might vary between Medicare Advantage and Original Medicare – even though advertised monthly premiums on Medicare Advantage plans can be fairly low, it doesn’t take long before you’re incurring out-of-pocket costs for services and medications to make these low premiums much more meaningful.

For example, a so-called zero-premium plan isn’t always as good a bargain as it sounds if you tack on co-pays for hospital stays and medication – some policies that used to charge a $250 co-pay for a three-day hospital stay have increased to 12 days in 2025 where costs are your responsibility.

Medicare Advantage Plans Are Reducing Benefits

Perhaps the most worrisome trend: Medicare Advantage plans, which have a long history of increasing benefits, are now contracting them. A spate of recent stories have discussed this trend; several plans are drastically changing drug tiers and hospital costs to the point where your total healthcare outlay might increase considerably.

Now, however, as health insurers react to the benefits changes wrought by the Inflation Reduction Act, they can retain profitability by trimming coverage here while raising its cost there. These trends are responsible for the administrative thicket that beneficiaries must navigate to make full use of their benefits, as they respond to ever-changing rules and cost-shifting.

What to Do if Your Plan is Terminated

Getting notification that your Medicare Advantage plan was cancelled is unsettling. If this happens, you need to act quickly to prevent a gap in your coverage. You need to decide between selecting another Medicare Advantage plan or reverting to Original Medicare. But what does that mean for you?

Understanding Your Options

Of course, if you don’t like what you’re getting from your current Medicare Advantage plan, you can switch plans during the Open Enrollment Period (15 October – 7 December) and look for one that offers better benefits to suit your healthcare needs.

Or you could choose to switch back to Original Medicare, which can be done easily, especially if you have a plan cancellation notice because you were guaranteed the right to purchase a Medicare Supplement Plan with no medical underwriting. That means no questions about your health, and no getting turned down.

Special Enrollment Periods

There are specific situations that will allow you to enrol in a new plan outside of the annual or special enrolment periods. For example, moving out of your plan’s service area provides grounds for a Special Enrolment Period, especially if you have an illness and need to keep your course of treatment intact.

However, you can take that termination notice and buy a Medicare Supplement from any insurer and have all the flexibility to pick your own doctors and facilities you want, whether or not they’re in a network.

Provider Insights on Medicare Advantage

Physicians are also speaking out about their experience with Medicare Advantage. Many describe the restrictions put in place by the plans, as well as the burdensome administrative barriers that crop up when their patients need care outside of the network.

Real-World Experiences

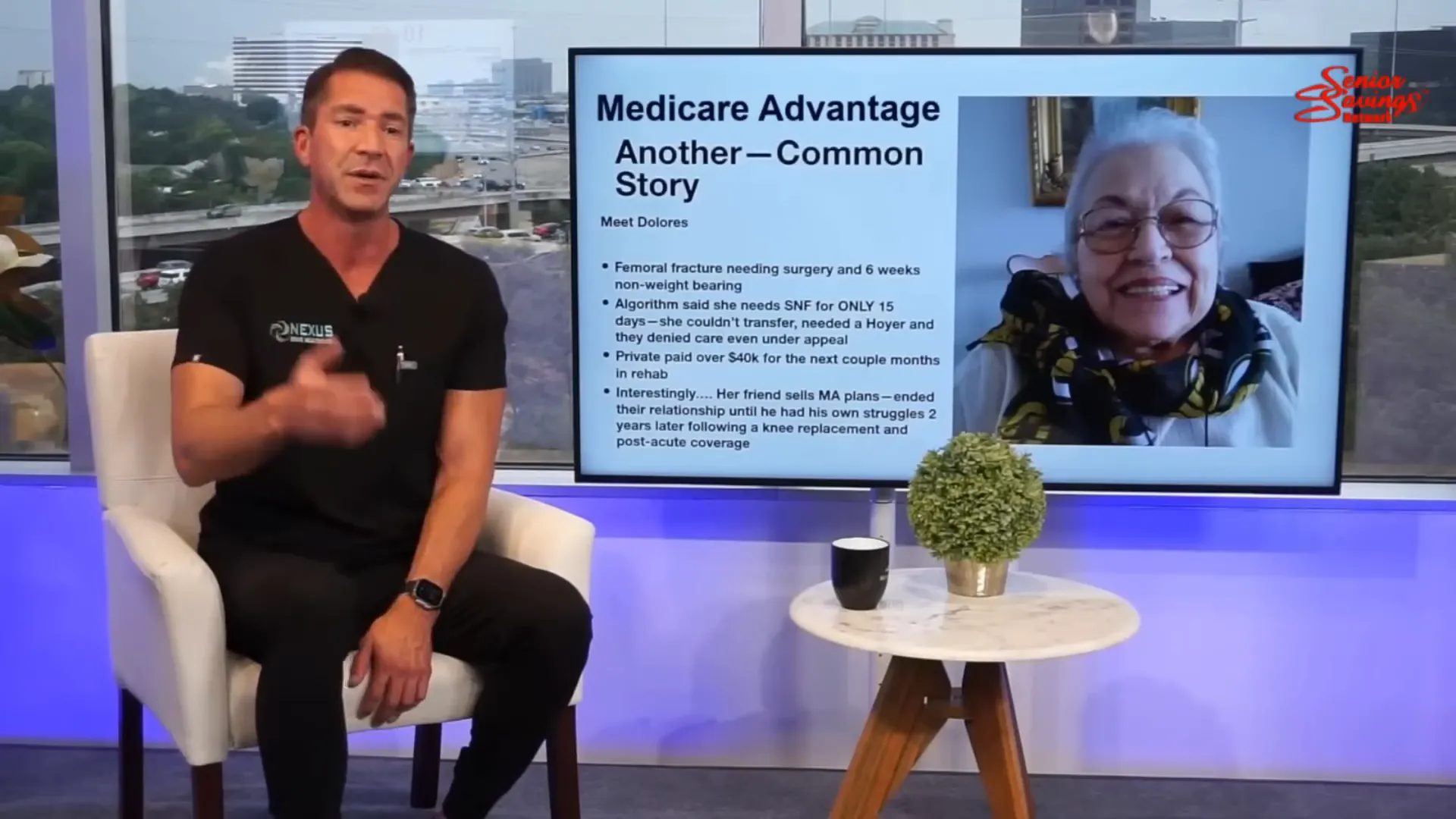

In practice, providers say, algorithms can lead to ‘denials of necessary services’ in favour of coverage for less expensive options depending on computer-generated assessment over physician recommendation. As one doctor told the Institute of Medicine last year: ‘Patients might find out that they have to pay thousands of dollars out of pocket for a service that should have been covered.’

A provider discussed a patient named Dolores who was catastrophically injured due to a severe hip fracture requiring lengthy rehabilitation. The automated system determined that her rehabilitation wasn’t ‘medically necessary’, denying the patient a stay at a skilled-nursing facility, resulting in providing inadequate care, forcing Dolores to pay out of pocket for her care, approximately $40,000, which could have been avoided if the care was re-evaluated by a human being.

Concerns with Algorithm-Based Care Decisions

Some clinicians are concerned that this trend signals a growing alienation between the patient and physician. With more care decisions being made by algorithms than clinician judgments, patients might not receive the care they need. It’s one thing to undermine clinician expertise in simple medical cases – one could argue that those patients might not mind the care experience – but it’s quite another to impair a patient’s care on a medical case that requires more subtle understanding.

Notably for patients, however, this trend is likely to increase frustration and confusion about what’s covered by their payment plan. Beneficiaries must be active self-advocates, and make sure they are getting the care they need, whether under Medicare Advantage or Original Medicare.

How to Get Off a Medicare Advantage Plan

Many people find it scary to leave Medicare Advantage, and this makes sense. There are steps you need to take. Here’s a quick overview of what to do.

Steps to Transition

- Review your current plan: Understand the benefits you’re currently receiving and identify what is lacking or what has changed.

- Explore your options: Research other Medicare Advantage plans or consider switching back to Original Medicare. Utilize resources available online or through local organizations.

- Complete the necessary paperwork: Whether you’re switching plans or reverting to Original Medicare, ensure you fill out the required forms accurately.

- Keep track of deadlines: Make sure to submit your applications before the December 7 cutoff to ensure your new coverage begins on January 1.

Working with an Insurance Broker

It can be worth reaching out to a licensed insurance broker – they can help you compare your options, navigate the application process, and ensure you pick the plan that’s the best fit for you. They will also be able to advise you on some of the traps you might fall into when learning about Medicare.

Changing Your Medicare Supplement Plan

You can switch Medicare Supplement plans anytime, even after your enrollment window has passed. (This isn’t like Medicare Advantage.) If you’re on a Medicare Supplement plan but want to change it, go right ahead. Do it anytime.

Key Considerations When Changing Plans

- Understand the differences: Each Medicare Supplement plan offers different coverage levels and premiums. Familiarize yourself with the benefits of Plans A, B, C, D, F, G, K, L, M, and N.

- Evaluate your health needs: Consider any ongoing health issues or potential future needs when selecting a plan.

- Compare premiums: Since the benefits are standardized, the main difference between plans is the premium. Shop around to find the best rate.

- Check for underwriting requirements: In most states, you may be subject to medical underwriting when switching plans, so be prepared to answer health questions.

Swapping out your Medicare Supplement plan might get you better coverage or lower premiums, and is something to revisit annually. Stay informed and proactive and you’ll likely end up with the best health coverage for you.

Understanding Part D

Are you enrolled in the federal government prescription drug benefit plan, Medicare Part D? If so, it is important that you pay attention to some upcoming changes to the program because they might affect your prescription drug choices and costs. The program was developed to assist prescription drug beneficiaries in sharing the expenses of purchasing drugs. But proposed changes might affect what exactly those expenses will be over the next several years.

What is Medicare Part D?

As a federal programme, Medicare Part D helps to pay for prescription drugs. Beneficiaries can either enrol in a standalone drug plan, or they can sign up for a Medicare Advantage (or ‘Part C’) plan that bundles drug coverage. And through it all, the environment changes, and your decisions could be more important than ever.

Recent Changes to Part D

By 2025, you may find that your Part D plan operates a little differently than it did a year or two ago, in terms of premiums, deductibles and co-pays. Changes in the Inflation Reduction Act could impact how much you pay for drugs.

- Premium Increases: Expect some plans to raise their premiums as insurers adjust to new regulations.

- Formulary Changes: Some drugs may be moved to higher tiers, resulting in increased co-pays.

- Special Programs: The new demonstration project could provide temporary subsidies, but it’s essential to read the fine print.

How to Choose the Right Part D Plan

Picking the right Part D plan takes work. But these steps can help: 1) Get and look over each plan’s Annual Notice of Change, also called the ‘Annual Enrolment Certificate’. All plans are required to send these to seniors who are enrolled in those plans. 2) Get documents that explain the plan’s costs, coverage, and rules. 3) Call your personal doctor’s office and discuss whether it meets the plan’s coverage.

- List Your Medications: Write down all the medications you currently take, including dosages.

- Compare Plans: Use tools like startpartd.com to compare different plans based on your medications and preferred pharmacies.

- Check for Coverage Gaps: Ensure that the plans you are considering cover your medications without excessive out-of-pocket costs.

- Review Annually: Your healthcare needs may change, so review your plan each year during the Open Enrollment Period.

Navigating Medicare.gov

Medicare.gov is the official website for information on Medicare, but it can feel like a maze. Here’s how I find what I’m looking for.

Using Medicare.gov for Part D Plans

When searching for Part D plans, Medicare.gov can be a valuable resource. Here’s how to use it:

- Start with the Plan Finder: This tool allows you to enter your medications and compare different plans based on costs and coverage.

- Understand the Terminology: Familiarize yourself with terms like “deductible,” “premium,” and “co-pay” to make better comparisons.

- Contact Support: If you have questions, Medicare.gov offers assistance via phone and online chat.

Medicare Advantage Open Enrollment Period Explained

When for you can consider making changes – and how – matters more than ever during the Medicare Advantage Open Enrollment Period. If you’re a beneficiary, knowing the rules of the game can make all the difference.

What is the Open Enrollment Period?

Each year, the Open Enrollment Period takes place from 15 October to 7 December. During that period, beneficiaries can join a Medicare Advantage plan, switch from Original Medicare to Medicare Advantage, or leave Medicare Advantage and return to Original Medicare. You must take action during this time and make decisions that will best serve your needs for the coming year.

Disenrollment Period

But in addition to the AEP, there is a separate, later window of time that runs from 1 January through 31 March: this unilateral disenrollment opportunity enables a beneficiary to walk away completely from a Medicare Advantage plan and return to Original Medicare if things aren’t working out. Here’s how it happens:

- Identify Your Needs: If you find that your current plan isn’t meeting your healthcare needs, consider this period your opportunity to switch.

- Contact a Broker: For personalized assistance, reaching out to an independent broker can provide tailored guidance based on your situation.

- Act Quickly: Don’t wait until the last minute; ensure all paperwork is completed and submitted promptly.

FAQ

Here are some frequently asked questions regarding Medicare Advantage and Part D plans:

What if I miss the Open Enrollment Period?

If you miss the Open Enrolment Period, you might have to wait until the next enrolment period or qualify for a Special Enrolment Period because of a special situation.

Can I switch from Medicare Advantage to Original Medicare at any time?

When you switch out of Original Medicare, you can switch back during a disenrollment period or during a Special Enrollment Period if you qualify for one.

How do I know if my Part D plan covers my medications?

If you’re curious to see what medications are covered under your prescription drug plan, search for your plan’s formulary on the Medicare.gov website or check with your plan’s website to see what medications your plan covers and at which tier.

Is it worth it to work with an insurance broker?

Yes indeed! You could think of an insurance broker as your knight in armour navigating through the maze of Medicare product selections to secure the best deal.

Knowing these four key elements of Medicare Advantage and Part D will keep you on the cutting edge of upcoming changes so that you can make the best decisions for your health and financial well-being.