What John Oliver Just Revealed About Medicare

What John Oliver Just Revealed About Medicare — A Deep Dive into Medicare Advantage, Risks, and Real Choices

Medicare is a word that carries authority and comfort for millions of Americans. It evokes the idea of stable, reliable healthcare provided through a federal program. But there is a common wrinkle in the Medicare landscape that uses that name while operating differently: Medicare Advantage. Over the last decade these plans have grown rapidly, now enrolling more than half of eligible beneficiaries and projected to cover nearly two thirds by 2034. That popularity makes it crucial to understand how they work, where they diverge from Original Medicare, and what that means for patients, caregivers, doctors, and hospitals.

This article pulls together the most important facts, examples, and cautionary tales so you can make choices with your eyes open. I will explain how Medicare Advantage plans are paid, why diagnosis coding matters, how health risk assessments and home visits can alter medical records, why provider directories and networks are unreliable, how prior authorization and appeal systems can delay or deny needed care, and what happens when someone tries to leave Medicare Advantage for Original Medicare. I will also outline realistic alternatives, like Medicare supplement plans and high deductible Plan G, and give practical steps to protect yourself when choosing coverage.

What Medicare Advantage Really Is — And Why the Name Can Be Misleading

On paper, Medicare Advantage plans sound appealing. They are marketed as a single-plan solution that bundles Parts A and B and often adds Part D or extra benefits like dental, vision, or gym memberships. They frequently come with low or zero monthly premiums and slick advertisements promising more services for less money. The problem is the word Medicare in the name creates the impression that these plans operate exactly like Original Medicare. They do not.

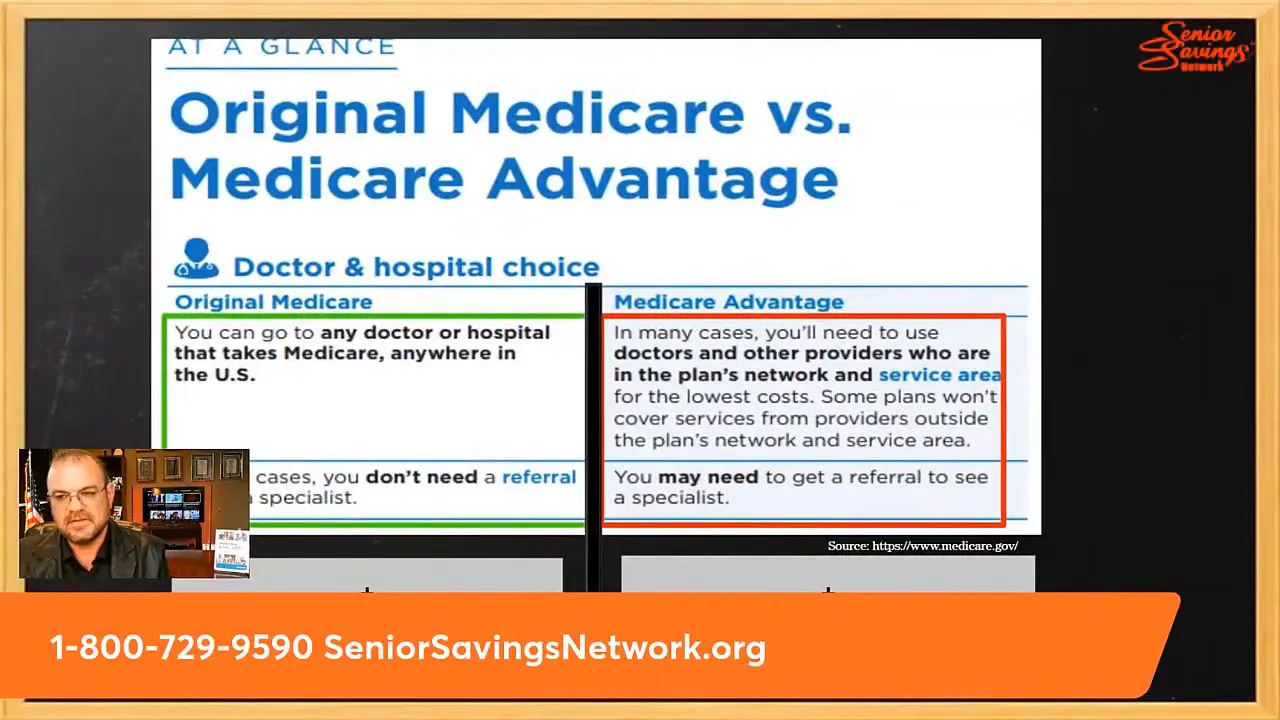

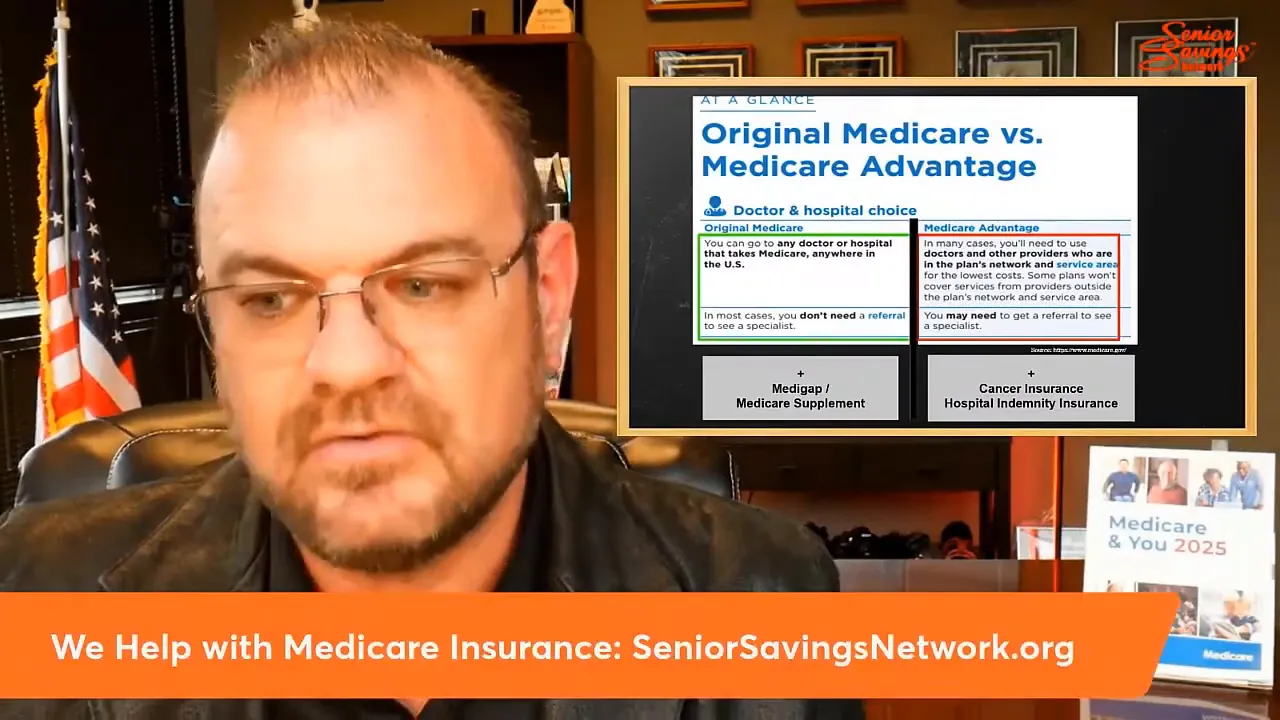

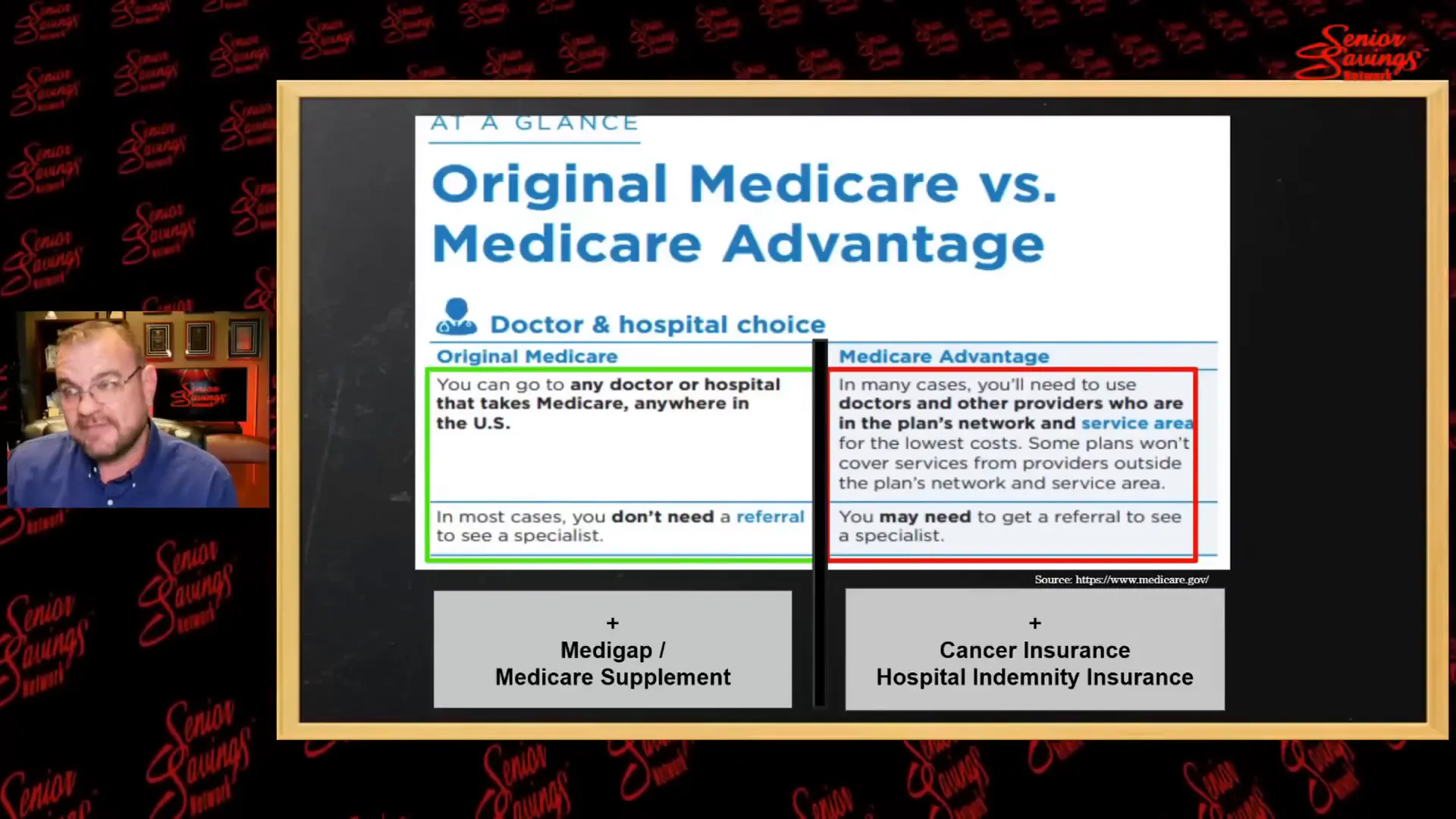

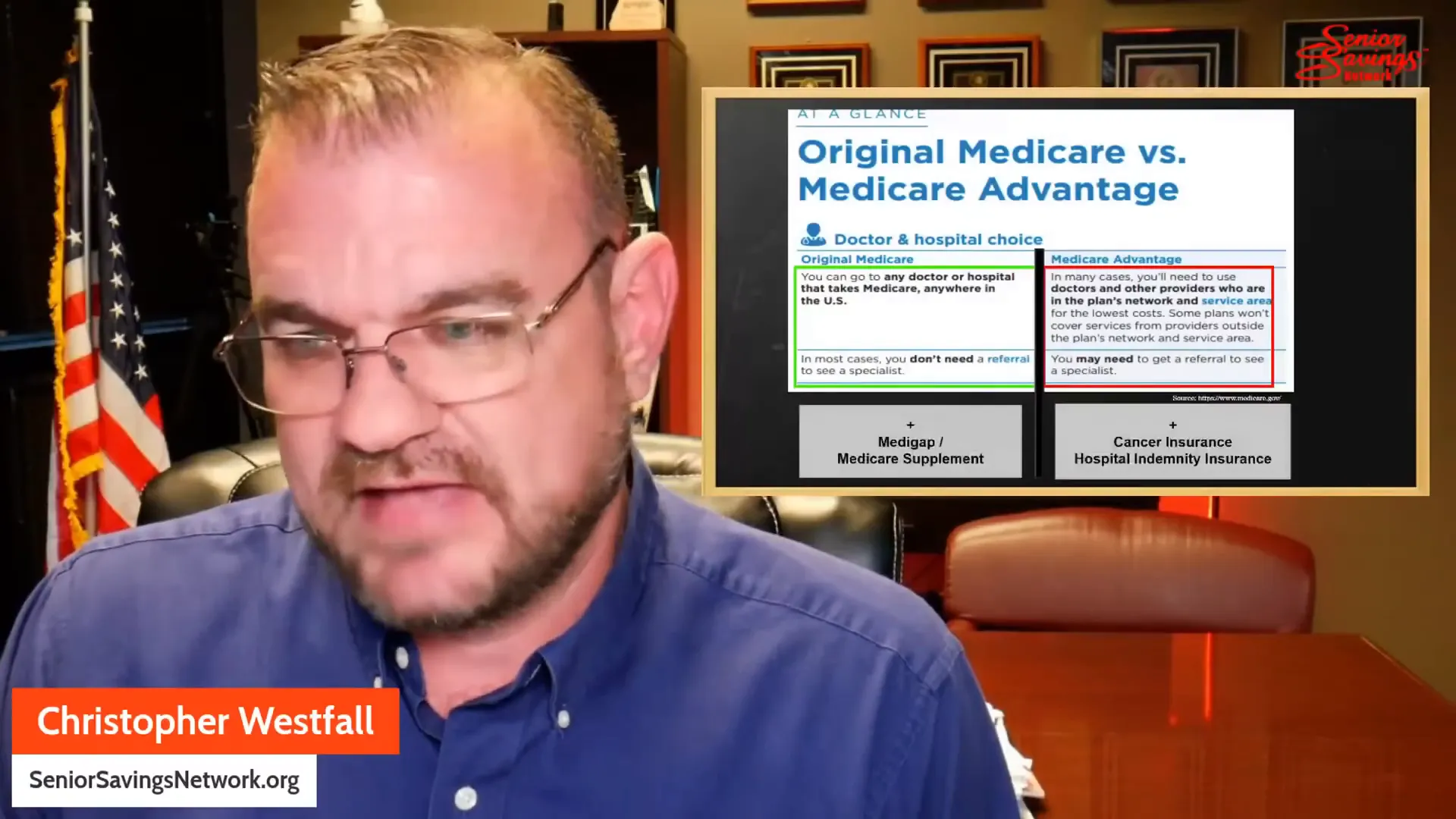

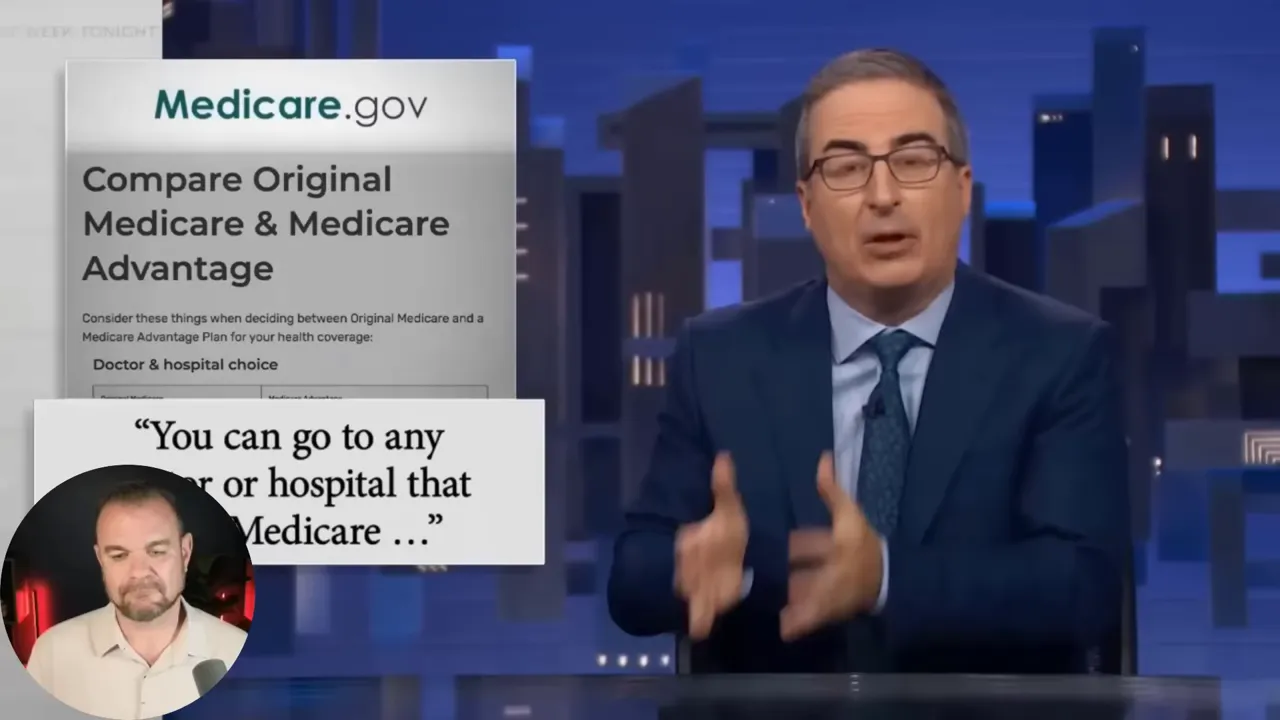

Original Medicare is a fee-for-service program administered directly through the federal government. Under Original Medicare, a doctor provides care, bills Medicare, and that bill is paid directly without prior approval from a private gatekeeper. There are no provider networks, no contractual prior authorization required by the insurer, and, crucially, providers treat patients without seeking permission from an intermediary.

Medicare Advantage, on the other hand, is a privatized alternative. The federal government pays private insurers a fixed monthly amount for each enrolled beneficiary. Those insurers manage benefits, set provider networks, enforce prior authorization rules, and collect the difference between what they are paid and what they spend on care. For people who prefer one-stop plans with low monthly costs, that structure can be attractive at first glance. But when care needs grow, the differences become consequential.

How Medicare Advantage Plans Get Paid: Capitation and Incentives

Understanding payment flows is fundamental because incentives shape behavior. Traditional Medicare reimburses providers based on services delivered. Medicare Advantage plans receive capitation payments: a fixed per member per month (PMPM) amount for each enrollee, regardless of whether that person receives care.

That PMPM payment is adjusted based on how sick the enrollee appears on paper. Plans report diagnosis codes that indicate the presence and severity of health conditions. Higher-risk codes raise the government’s monthly payment to the plan. That system is meant to compensate plans that take on sicker patients. In practice, it creates a financial incentive for plans to document as many lucrative diagnoses as possible.

There is a real danger here. If plans are paid more when enrollees have more or more serious diagnoses recorded, those plans benefit when health records show greater disease burden. Meanwhile, because they receive the same PMPM no matter how much care is delivered, their profit margin increases when patients receive less care. That mismatch of incentives is the root of many of the problems described in the following sections.

Diagnosis Coding and Upcoding: When Paper Gets Profitable

Diagnosis codes are the language plans use to explain a member’s health status to the government. In theory, they are a fair system. Diabetes without complications yields one payment level. Diabetes with complications yields higher payments. But where the danger emerges is in how easily coding can be amplified without meaningful clinical evidence.

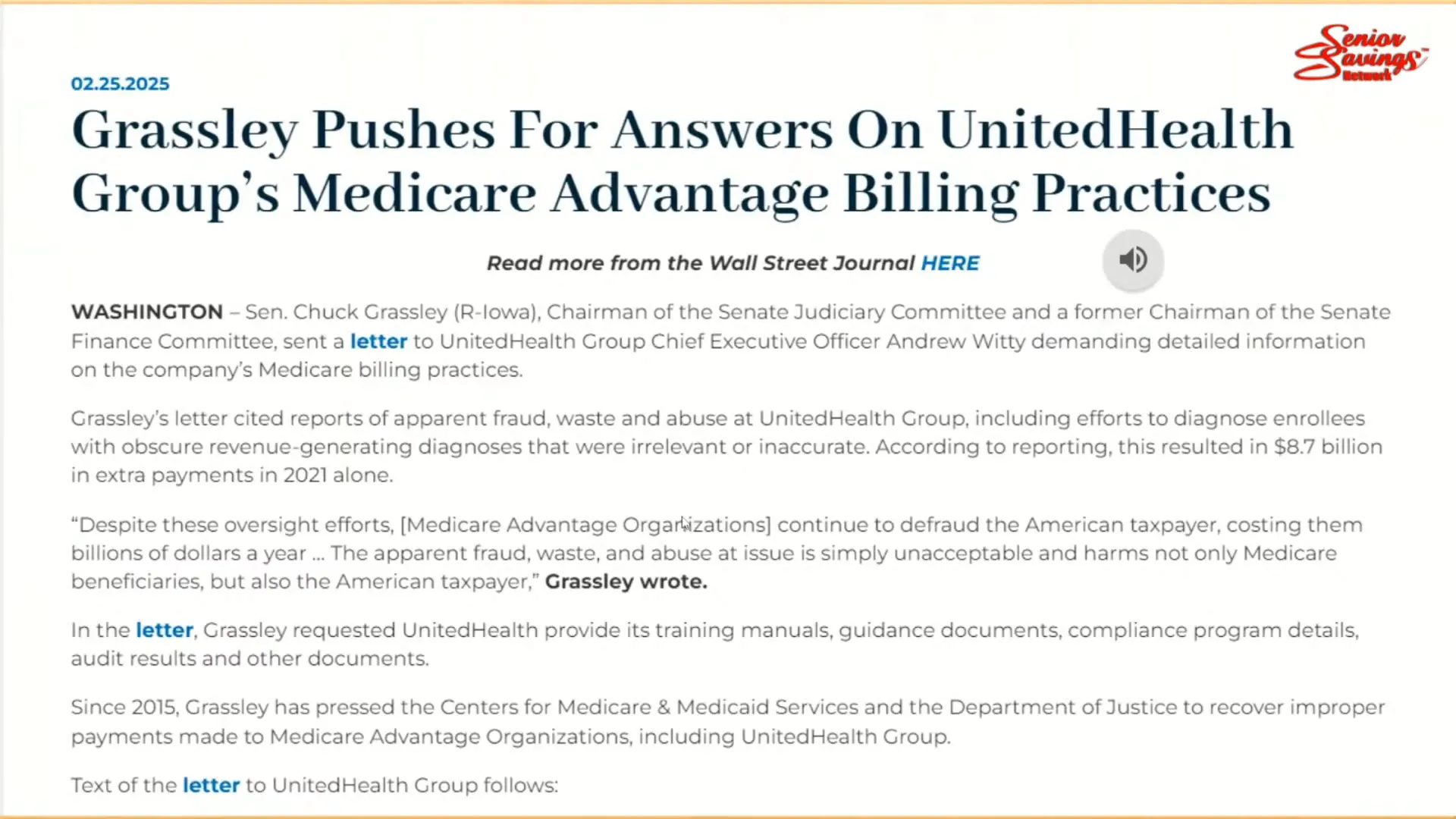

Multiple investigations and federal audits have found major Medicare Advantage insurers submitting inflated diagnosis profiles for their enrollees. In practice this can mean adding conditions to a patient’s chart without actual treatment or confirmation, or interpreting routine notes as warranting higher-risk codes. Regulators have flagged hundreds of millions of dollars and in some cases billions of dollars in overpayments tied to such coding practices.

For the beneficiary, the consequences are more than theoretical. Inflated diagnosis lists can follow a person for years and show up in medical records. That can affect eligibility and pricing for other insurance products, like life insurance or long-term care insurance, and create an enormous burden to correct. Removing a wrongly coded diagnosis is a lengthy, stressful process that often requires review of medical records, formal appeals, and persistent follow up with providers and insurers.

Practical example: Life insurance applications ruined by coding

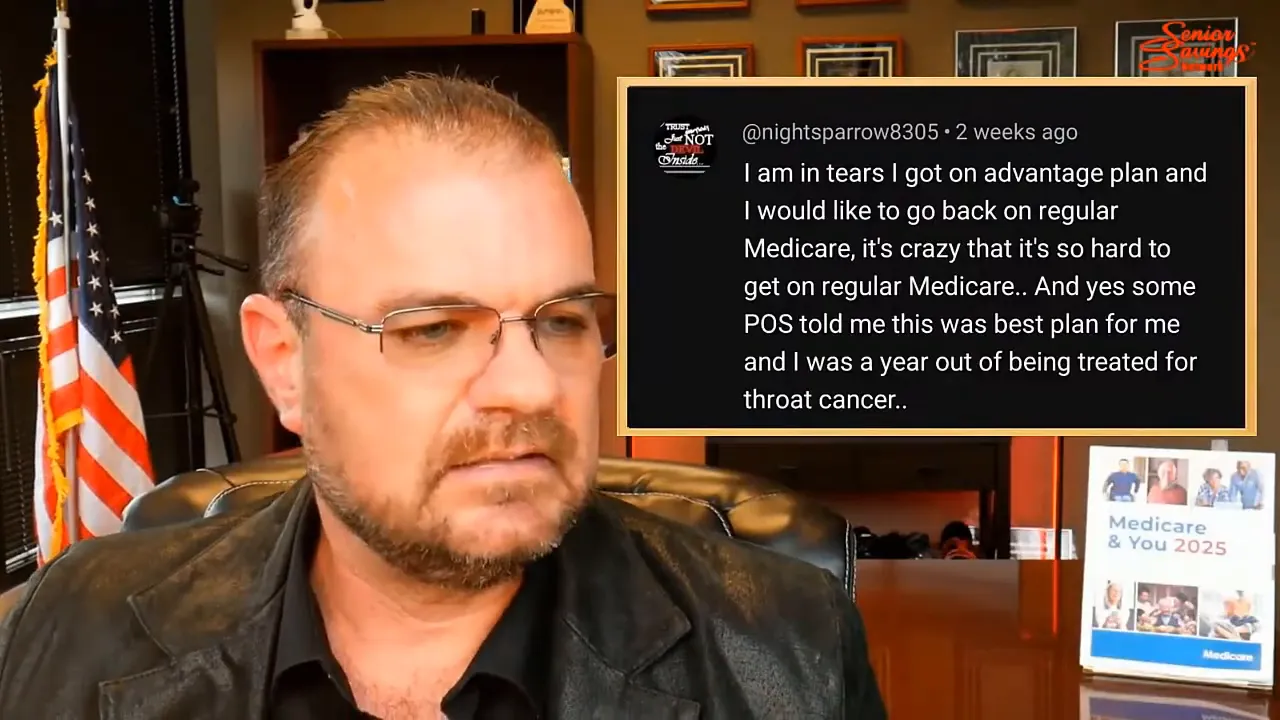

Imagine a 65-year-old who signs up for a Medicare Advantage plan and later wants a substantial life insurance policy to fund an estate plan. Underwriters review that person’s medical records and see multiple serious conditions recorded during Medicare Advantage assessments. Even if those conditions were never treated or known to the patient, the underwriter can decline coverage or charge much higher premiums. The individual then faces months of correcting records and fighting to get off inappropriate codes. That scenario has occurred in hundreds of documented cases.

Health Risk Assessments and Agent Incentives

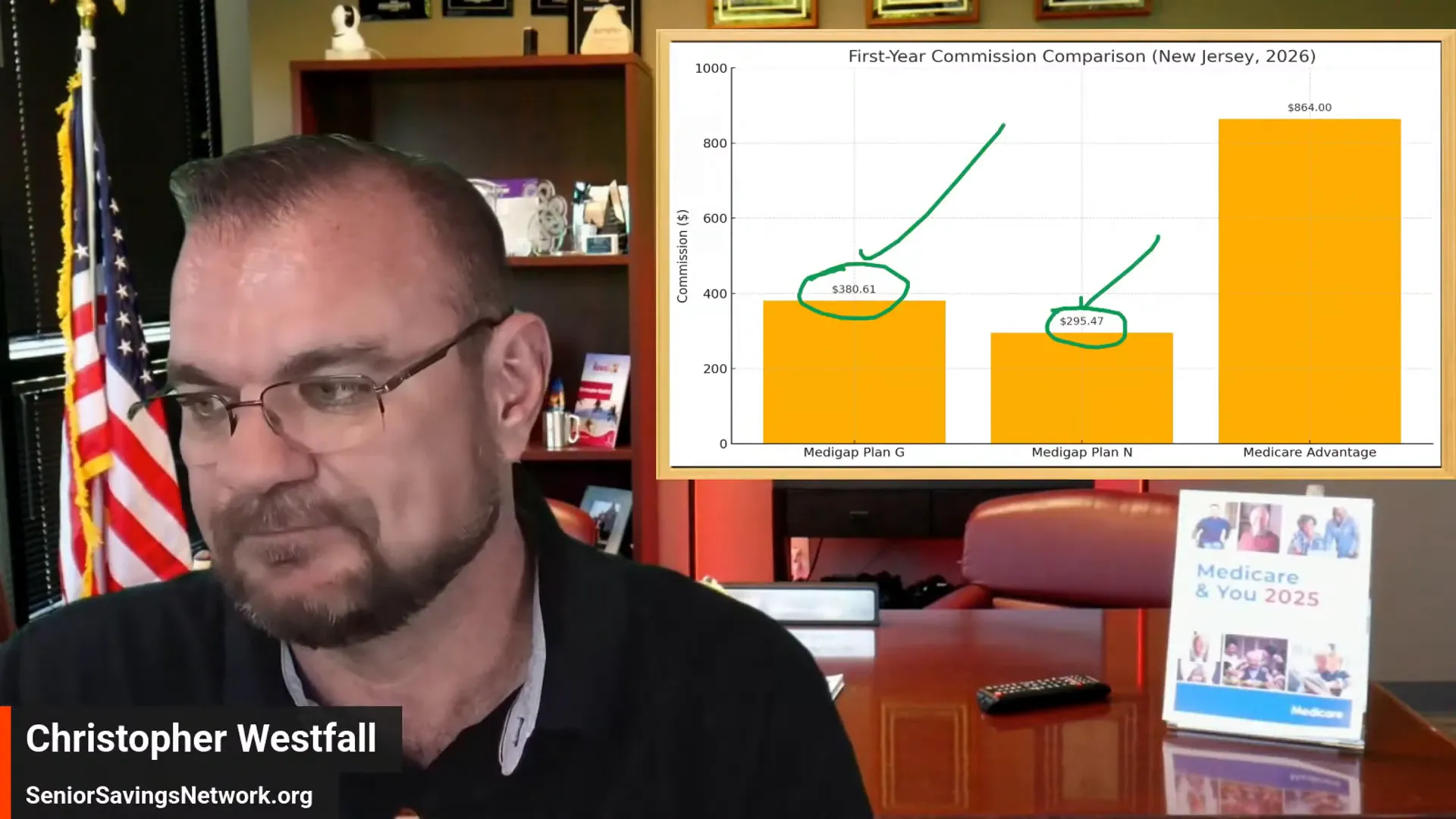

Health risk assessments (HRAs) are one of the specific tools insurers use to identify billable conditions. An HRA is usually a short questionnaire completed by the member or an agent that asks about current symptoms and conditions. Insurers use the information to update diagnoses and thus increase risk scores.

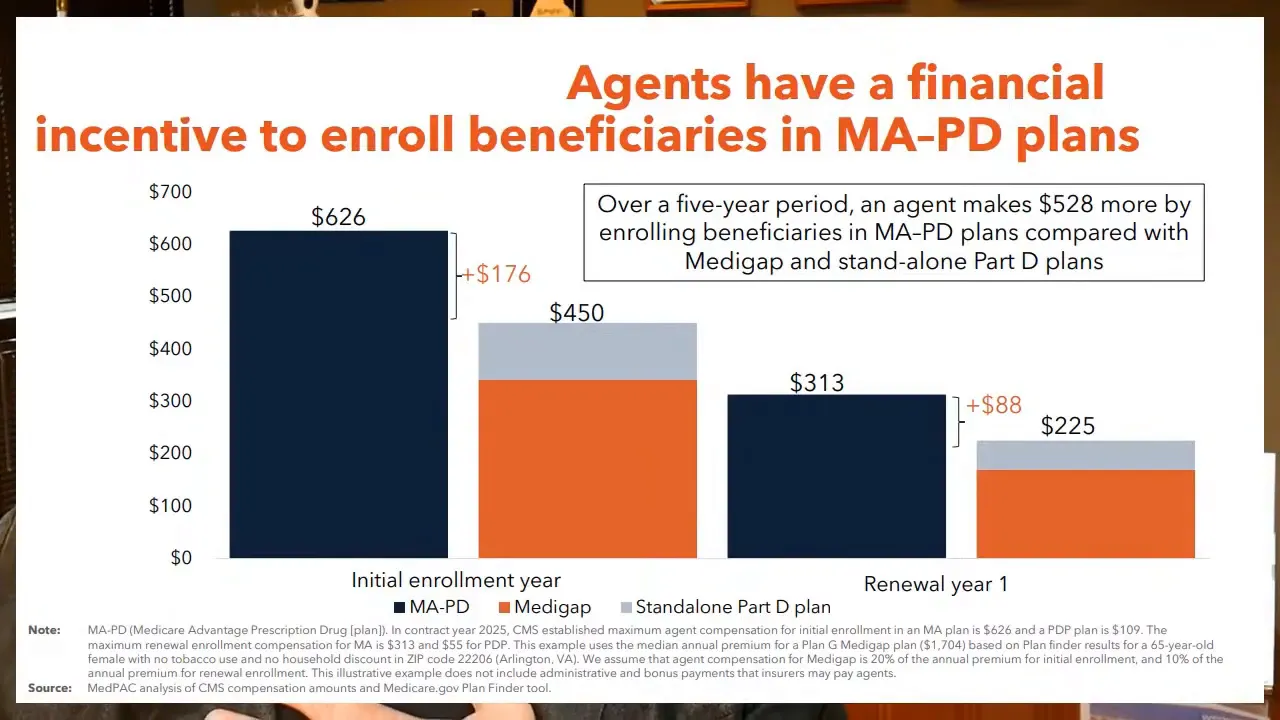

Here is the troubling reality: agents and brokers are often paid significant commissions for enrolling new members in Medicare Advantage. In some markets a new enrollee generates hundreds of dollars in commission immediately, and plans may also pay agents a bonus for completing HRAs. That creates a potential conflict of interest. An agent may be incentivized to complete HRAs or document issues in a way that boosts plan payments, while the member may not fully understand the long-term consequences of those added diagnoses.

It is not illegal for agents to be paid commissions. It does become problematic when the incentives distort patient records and long-term financial prospects. That is why anyone considering a Medicare Advantage plan should ask direct questions about who is performing health assessments, what is being recorded, and whether the agent or clinician explained the possible downstream consequences.

Home Visits, House Calls, and Questionable Coding

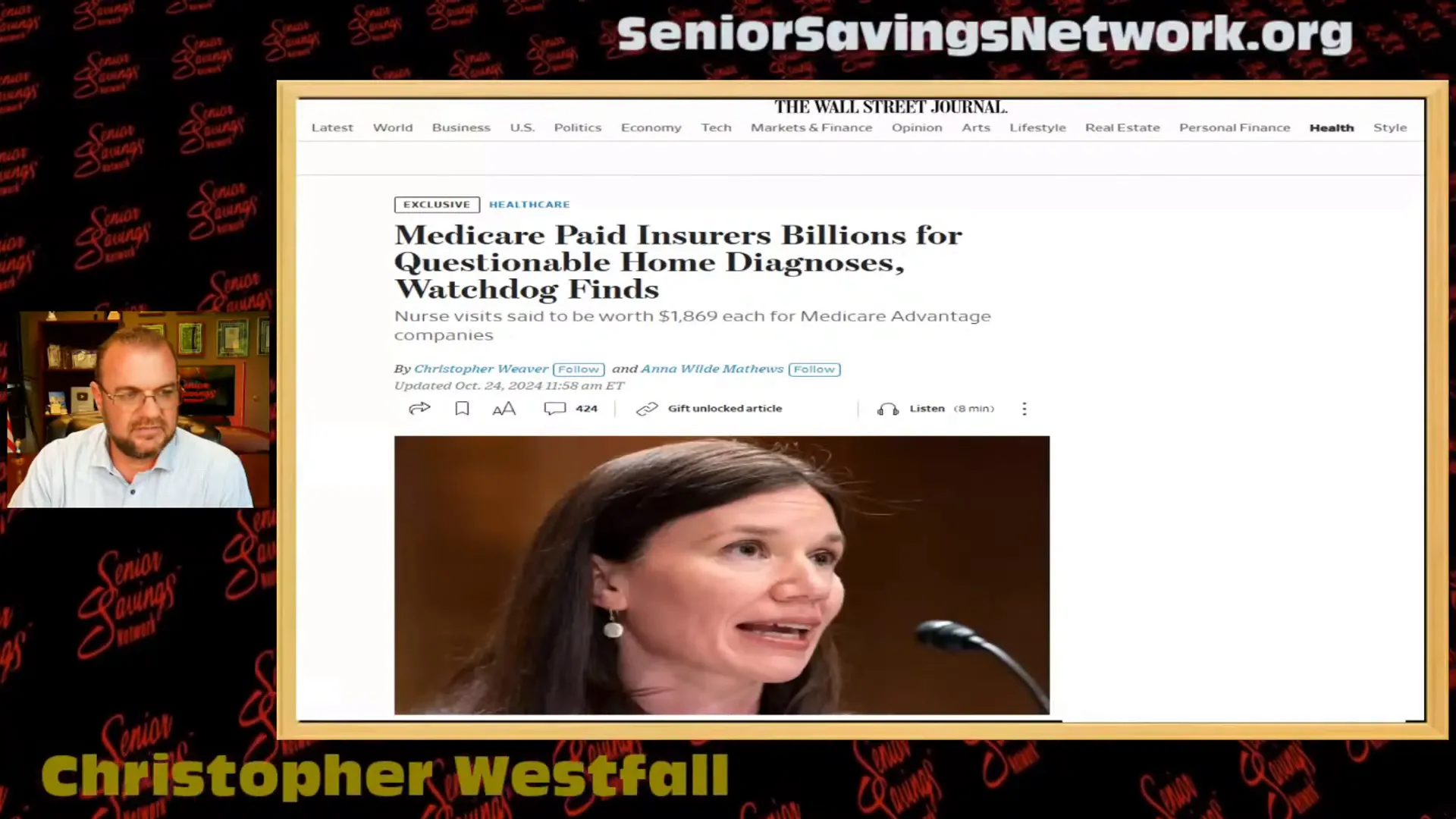

Another attention-grabbing practice is home visit programs. Many Medicare Advantage plans now advertise a “house call” by a clinician as a benefit. On the surface this is a wonderful idea: a nurse or clinician checks vitals, reviews medications, and identifies care gaps at no out-of-pocket charge. For socially isolated seniors, it is also an appealing human contact. But investigations have raised red flags about how some home visit programs are used to generate lucrative diagnoses without confirmatory testing.

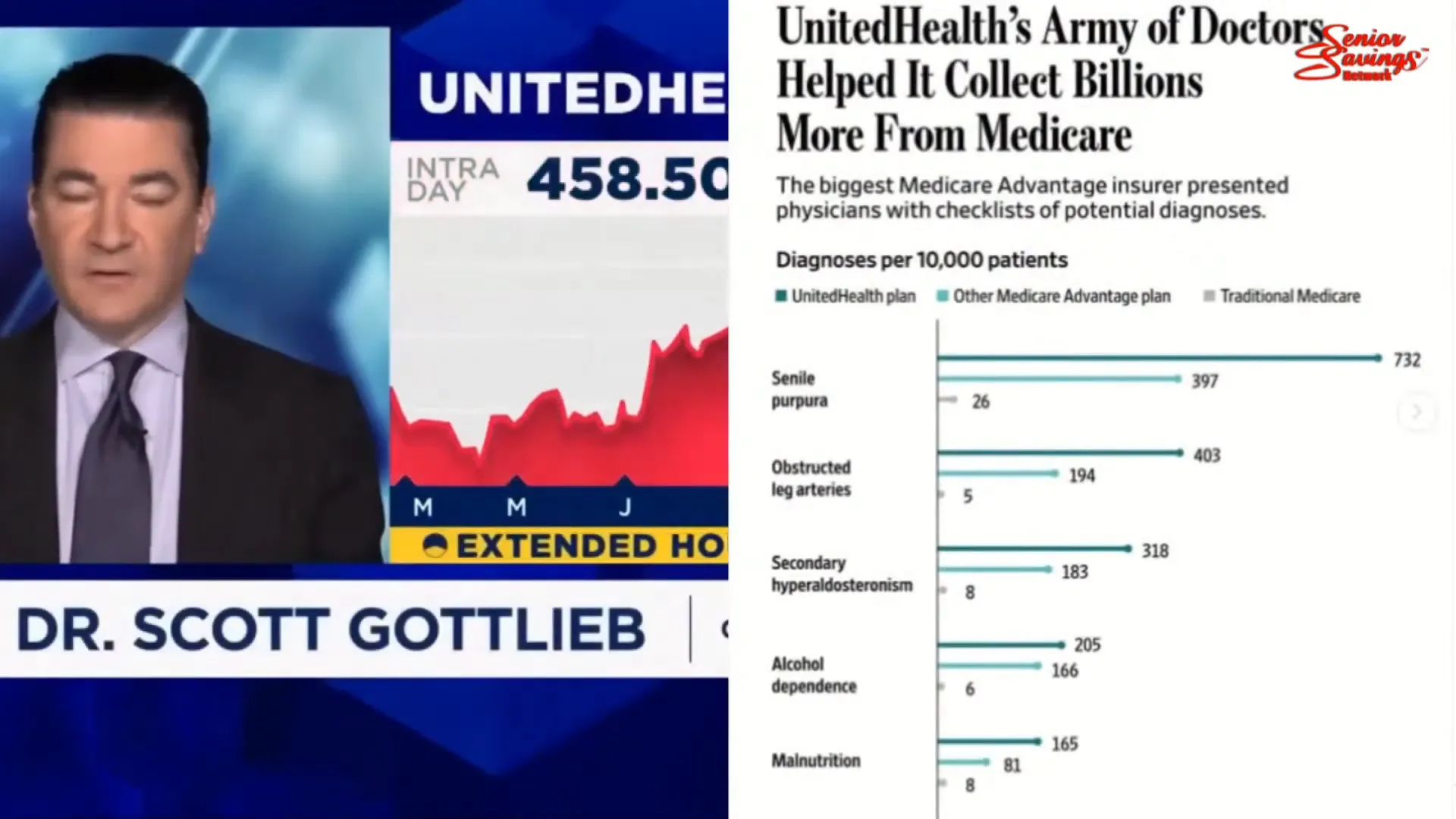

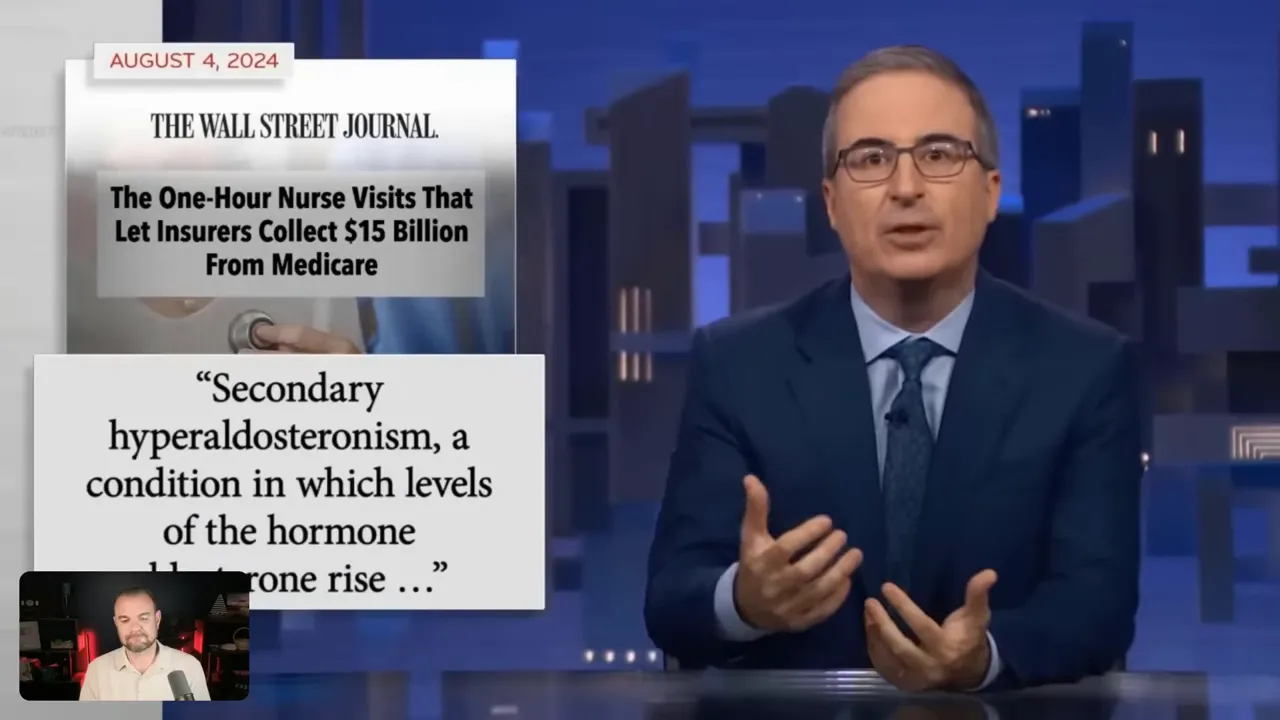

In reported investigations, clinicians conducting home visits were encouraged or required to run wide screening tests and select diagnoses suggested by software prompts. In some cases, the software proposed specific diagnostic codes that increased plan revenue despite no laboratory tests or specialist confirmations. One example is a diagnosis of secondary hyperaldosteronism that was added hundreds of thousands of times during home visit programs, producing hundreds of millions of dollars in additional government payments over a few years.

A former house calls nurse described the pressure to assign certain codes as absurd, stating she would never have made such a diagnosis in clinical practice. That mismatch between clinical judgment and coding prompts undermines trust and highlights how systems designed to enhance care can be repurposed as revenue engines.

What the Big Studies and Hearings Reveal

When academic and investigative journalists review industry-funded studies, many experts find fundamental flaws and biases. Independent reviews of Medicare Advantage studies often conclude that favorable findings are skewed by selective data, inadequate risk adjustment, or conflicts of interest. Leading health policy experts have flagged industry-funded studies as lacking transparency and methodological rigor.

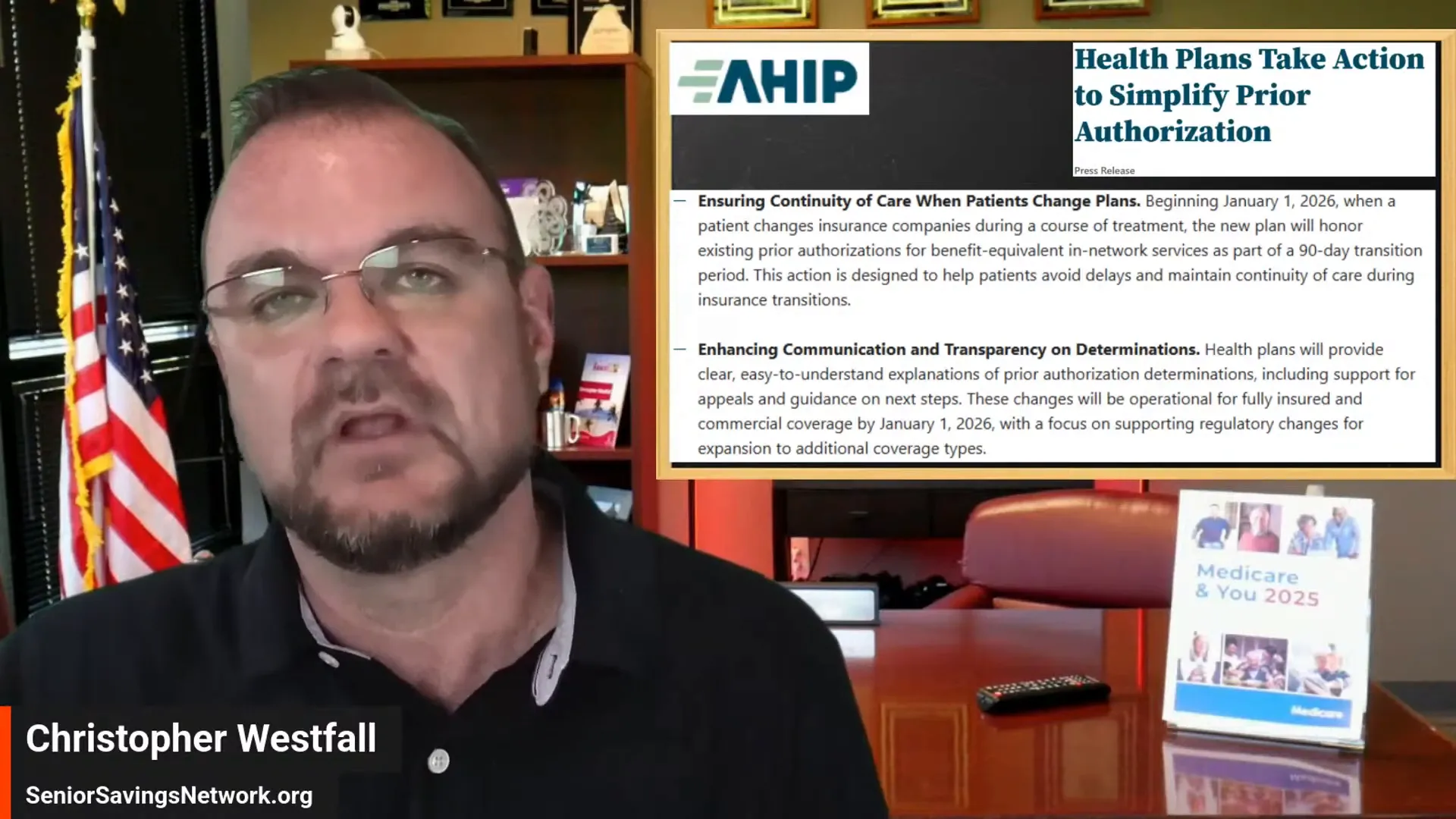

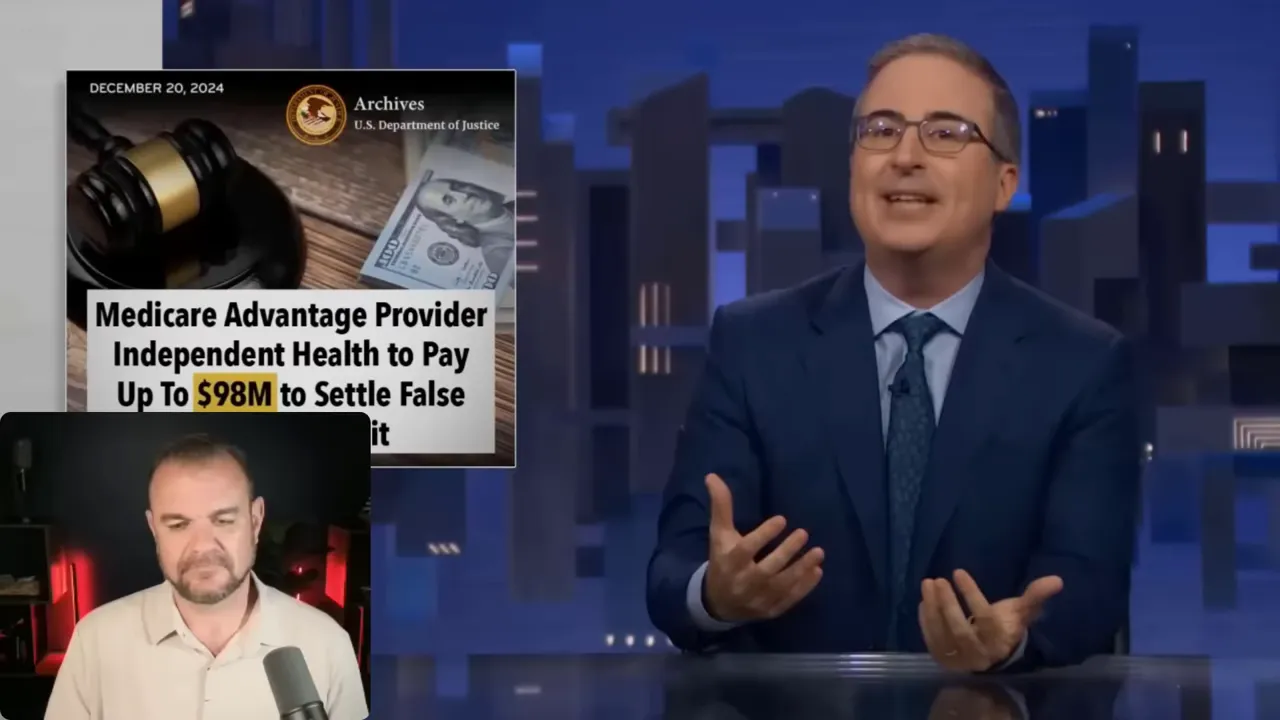

Congressional hearings have also brought evidence forward: federal audits, internal company documents, and whistleblower complaints show patterns of questionable coding, inflated billing, and aggressive revenue-seeking tactics. Some of the largest Medicare Advantage providers have faced multimillion-dollar settlements and federal investigations. Those findings led to a broader public conversation about whether private plans using the Medicare brand are delivering better care or simply shifting costs and extracting profits from the federal program.

Who Medicare Advantage Is Built For — And Who It Leaves Exposed

There is an important nuance that often gets lost amid the criticism: Medicare Advantage can be a reasonable choice for certain beneficiaries. For relatively healthy seniors who rarely need specialty care, a Medicare Advantage plan with low or zero premiums plus dental and vision perks can be a practical short-term option. Gym memberships and preventive benefits appeal to people who are active and want predictable, small monthly payments.

But the risk lies in longevity and future needs. A plan that looks great at 65 when someone plays pickleball twice a week might be disastrous at 72 when chronic conditions or sudden illness require specialists, long hospital stays, or rehabilitation. Disability and functional decline among seniors commonly increase in the early seventies. If you select a plan at 65 that restricts networks and imposes prior authorization hurdles, you may be trapped in that system for years.

The bottom line: Medicare Advantage can be appropriate for a narrowly defined profile — relatively healthy people who value low premiums and are comfortable navigating restrictions. For everyone else, the tradeoffs are significant and potentially costly.

Provider Networks and Directory Accuracy

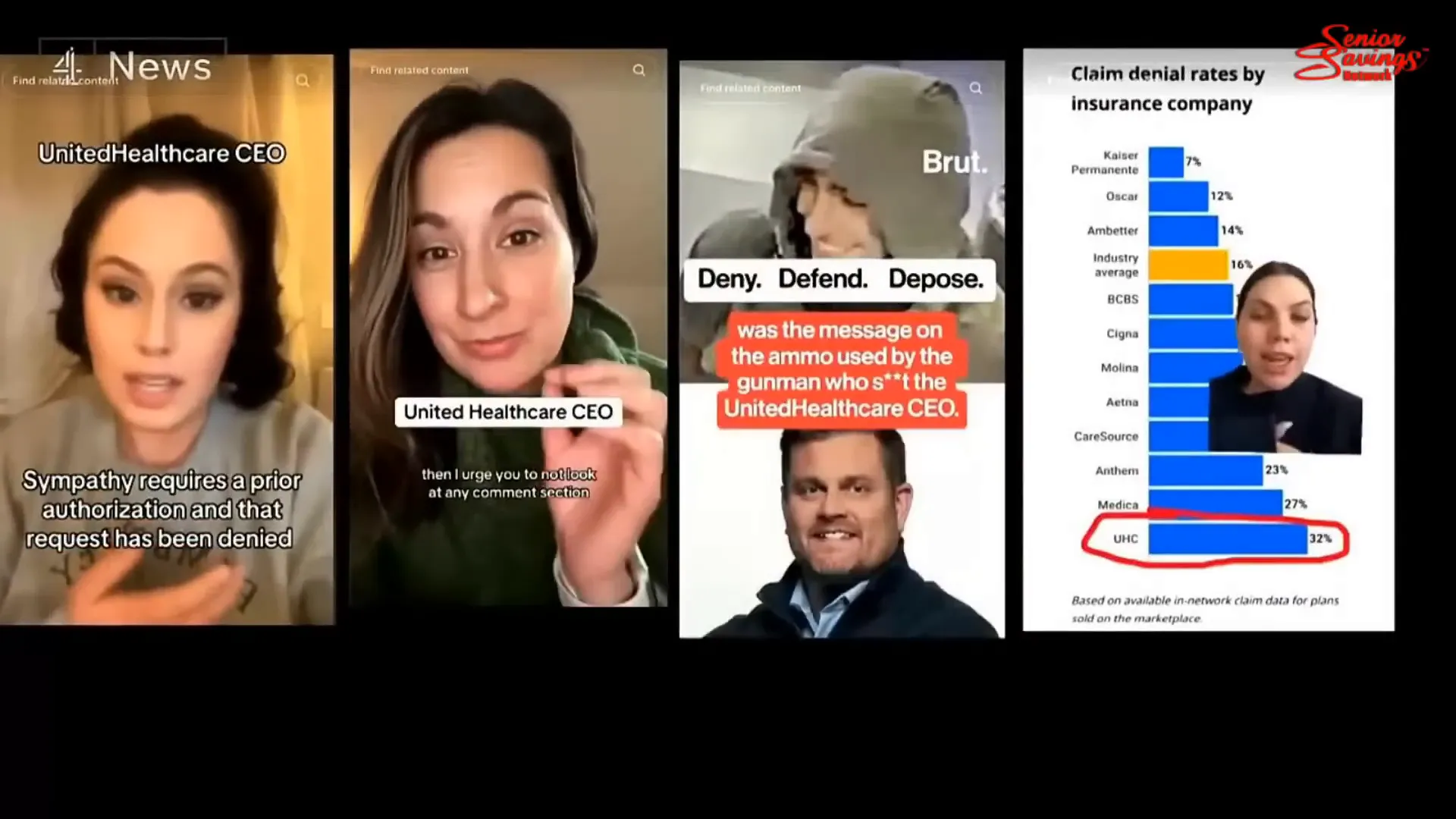

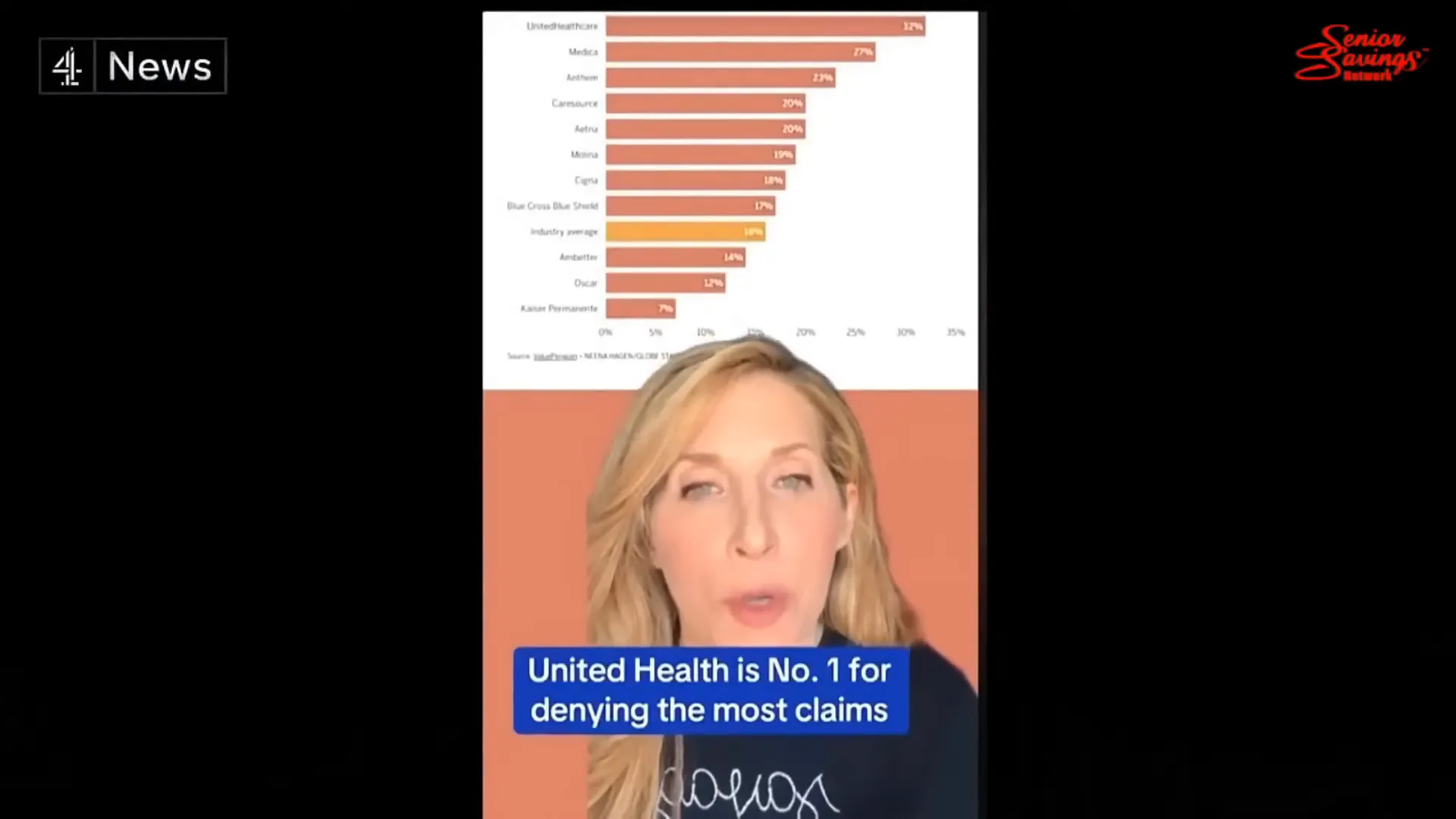

One of the most persistent complaints about Medicare Advantage is inaccurate provider directories and unreliable networks. Under Original Medicare, the patient can see any doctor or facility that accepts Medicare. Under most Medicare Advantage plans, care is limited to a provider network, and coverage outside that network may be subject to higher cost sharing or outright denial.

Investigations show a startling number of inaccuracies in provider directories. Reviews found that between 30 and 60 percent of listed locations were incorrect. Providers listed as in-network may be offices that no longer accept the plan, outdated addresses, or even non-existent clinicians. Mental health access is especially problematic. One investigation that attempted to schedule appointments across various mental health networks could only make appointments 18 percent of the time — meaning patients were turned away more than 80 percent of the time when they sought care.

These directory errors are not mere clerical issues. They can have immediate consequences: a beneficiary chooses a plan believing key specialists and hospitals are in-network, then discovers they are out of network when treatment is needed. Out-of-network care can lead to surprise bills, denied claims, and delays while the patient scrambles for authorization or appeals.

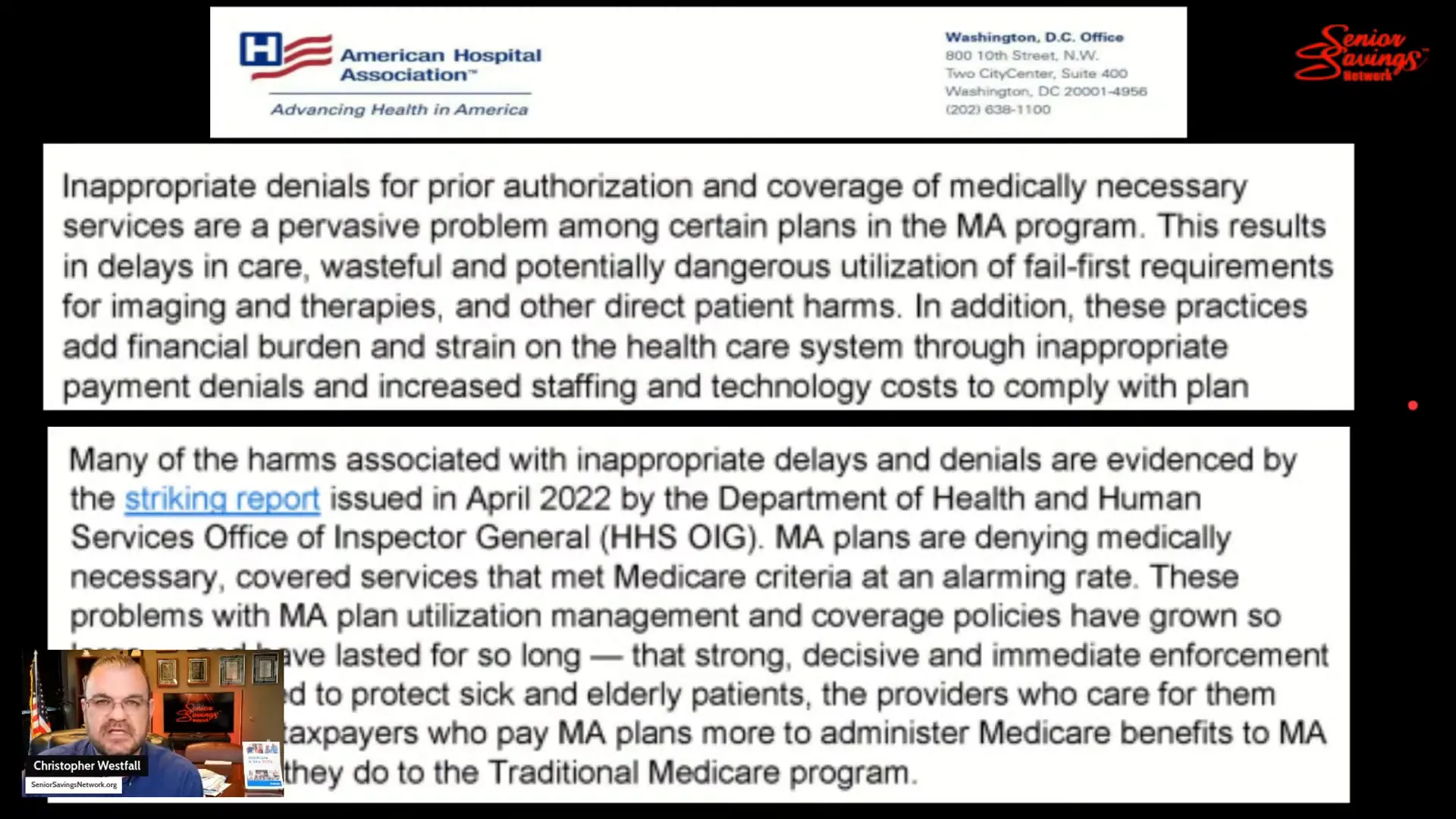

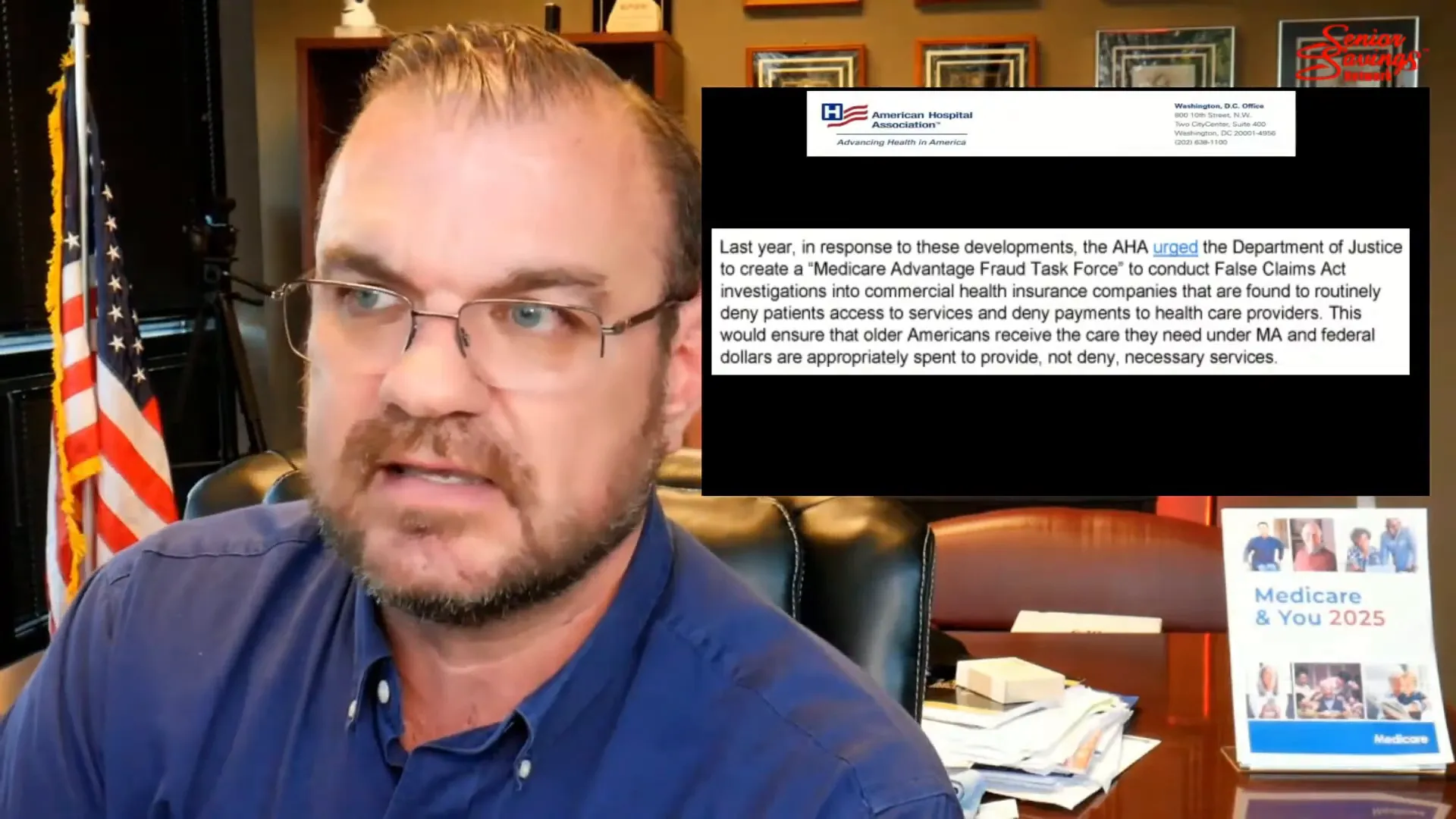

Prior Authorization: A Gatekeeper That Can Delay Care

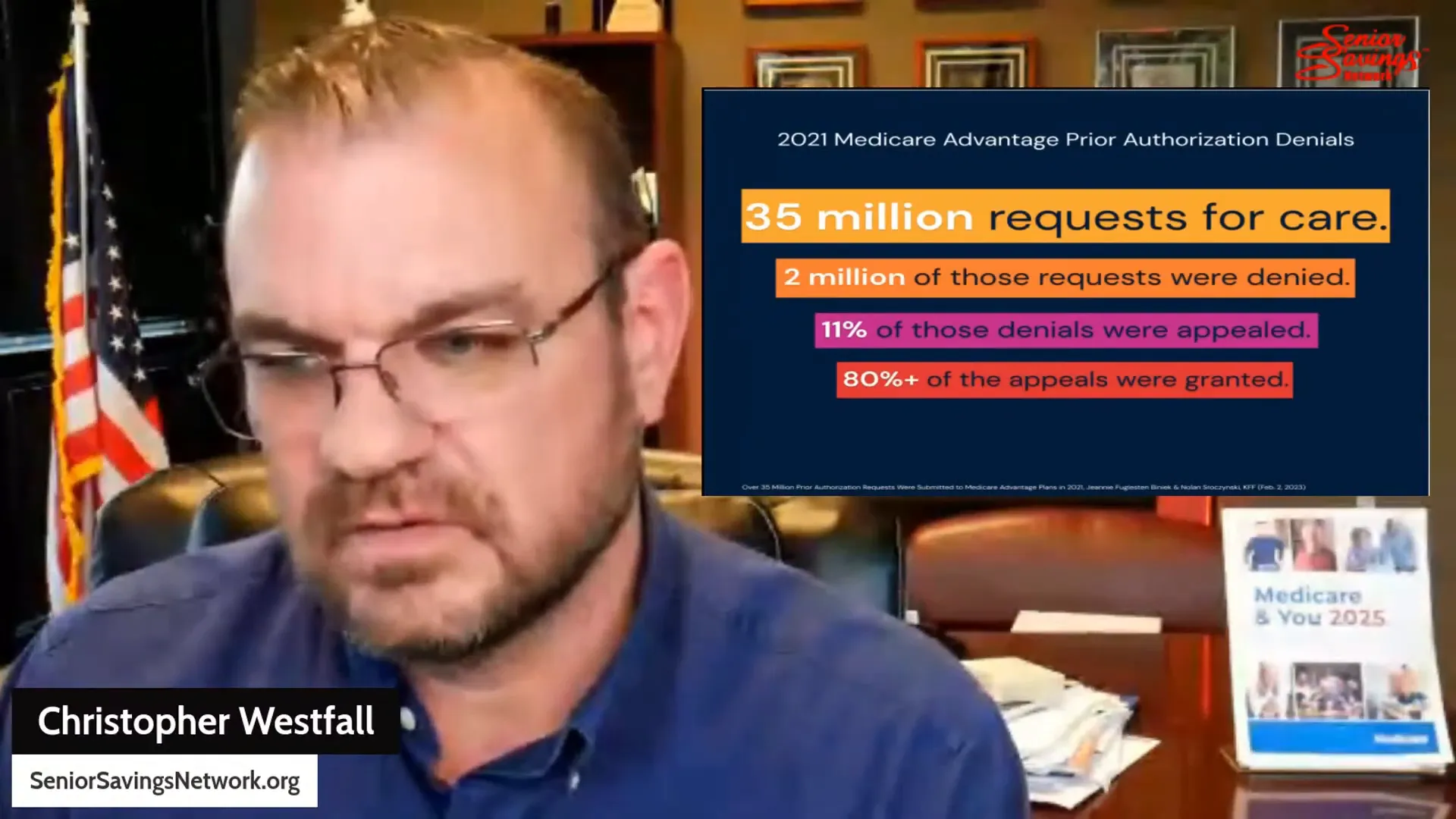

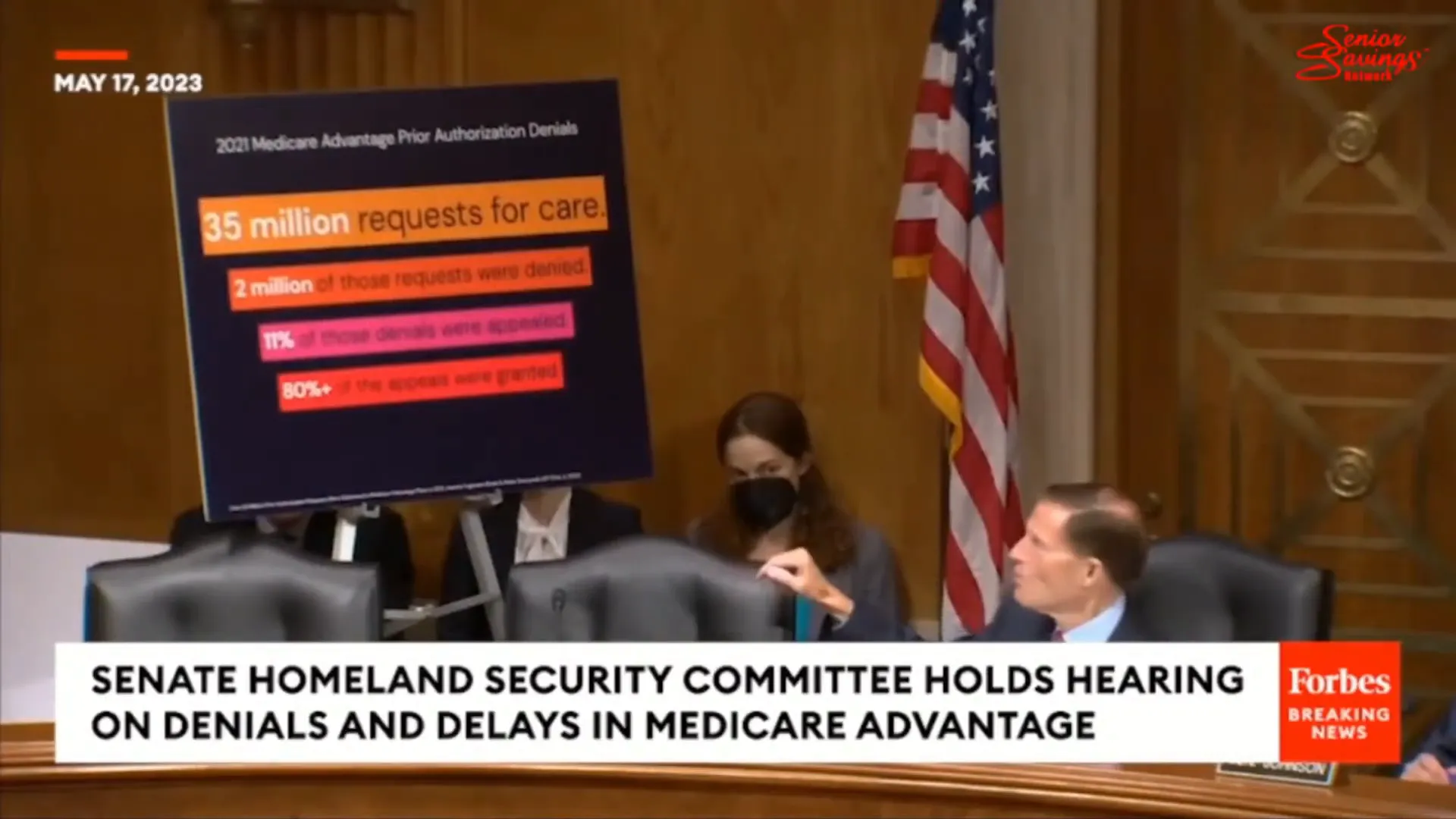

Prior authorization is a process where a plan must approve certain tests, procedures, or prescriptions before they are provided. While prior authorization exists in many commercial insurance products, its ubiquity and scope in Medicare Advantage are significant. Nearly all Medicare Advantage enrollees face prior authorization for some services.

Prior authorization often requires long phone calls, faxes, or uploading reams of documentation. Doctors report spending hours each week handling these requests. One physician described a process where staff must call an 800 number, provide patient and clinical details, request permission to fax documents, then call back to discuss the case — a prior authorization to get a prior authorization. That administrative burden drains clinical time and shifts resources away from patient care.

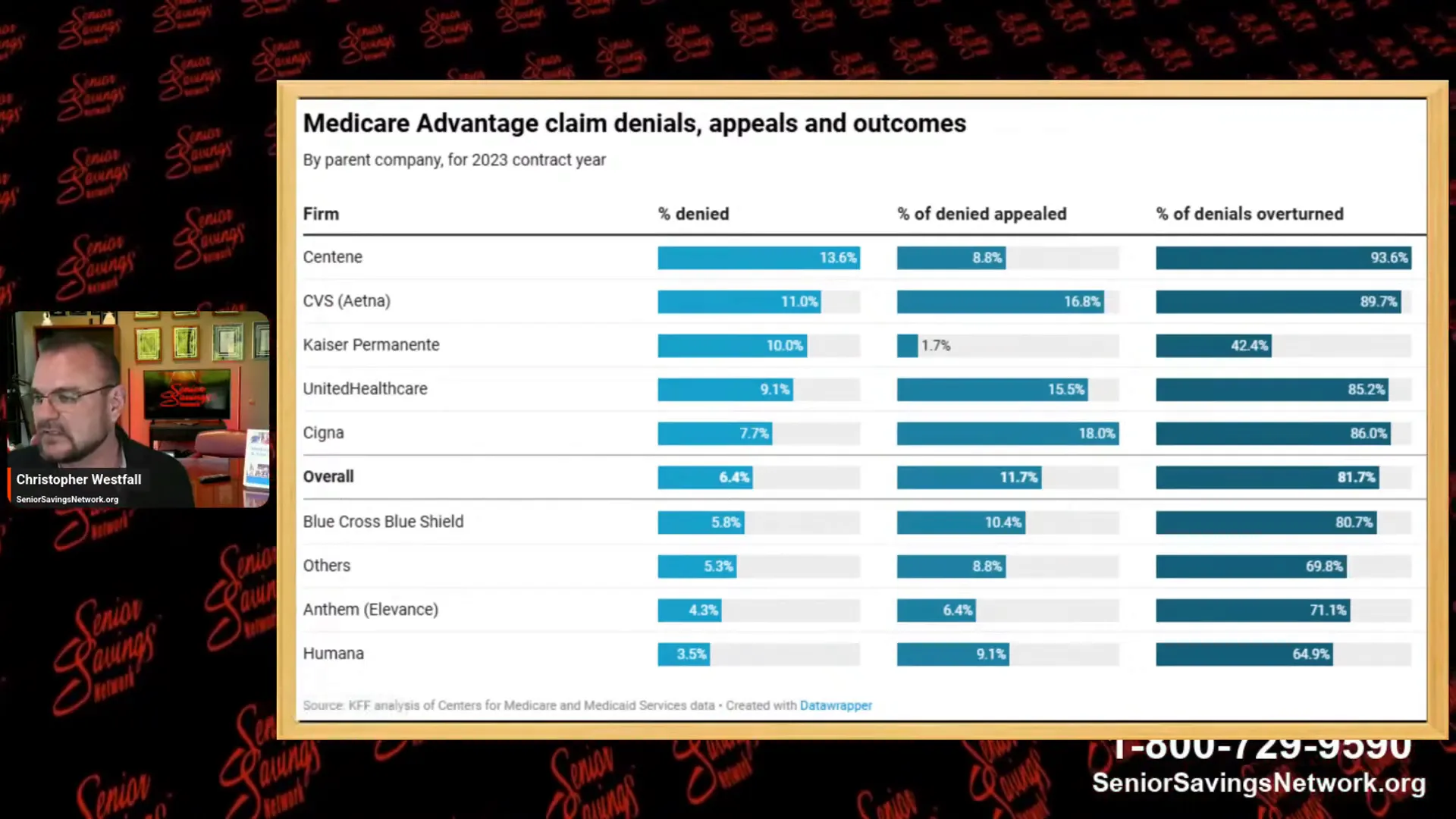

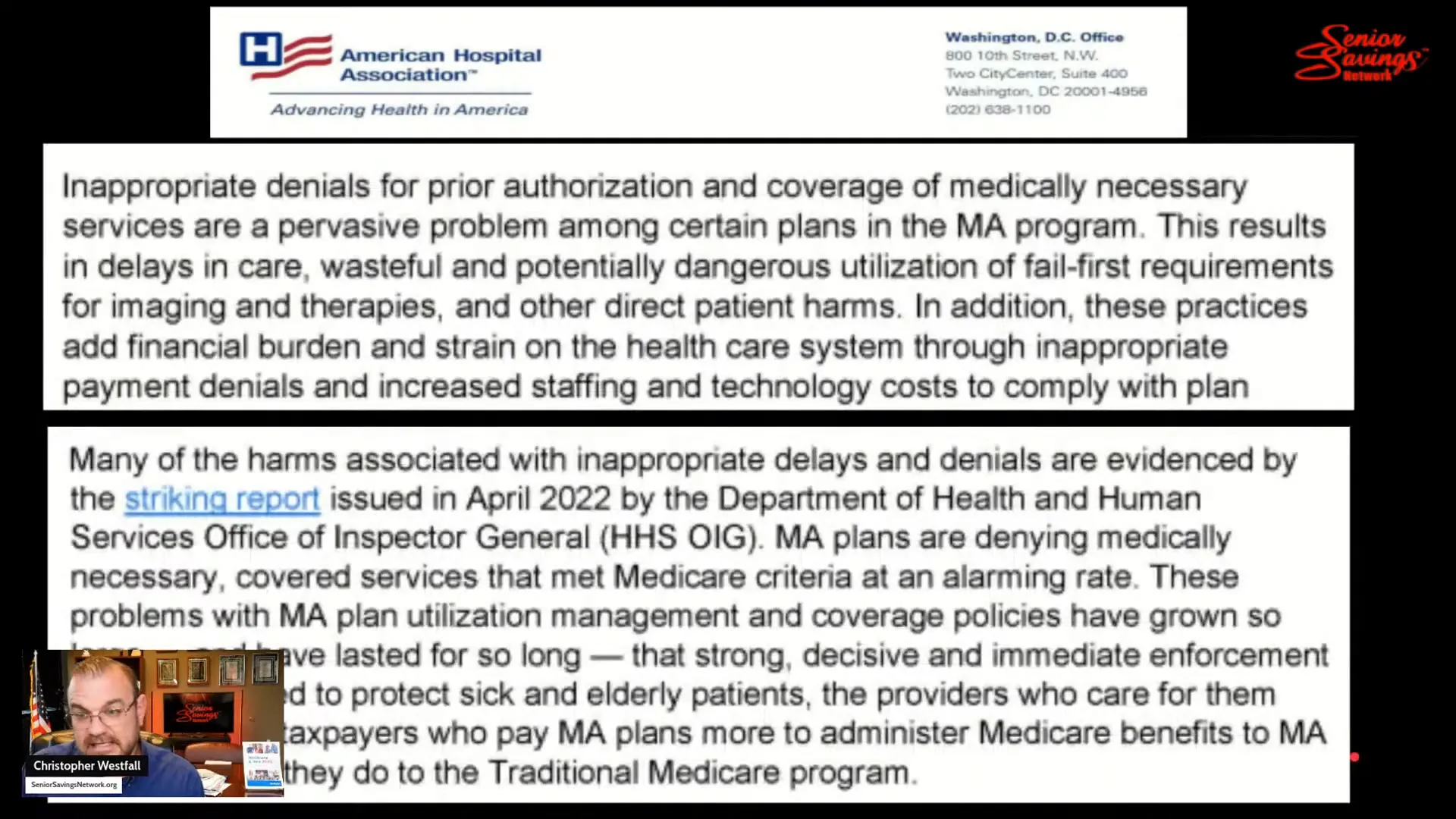

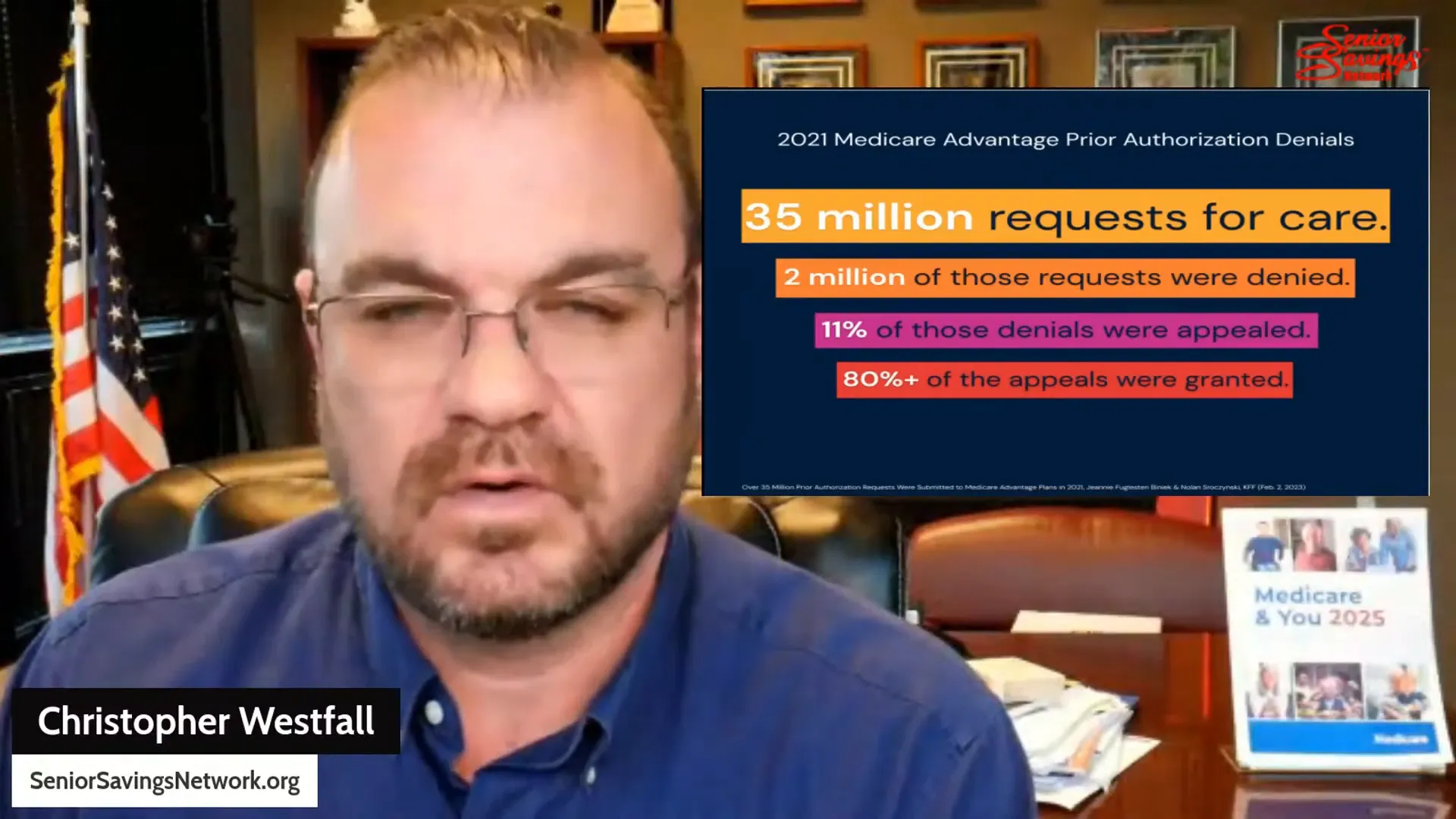

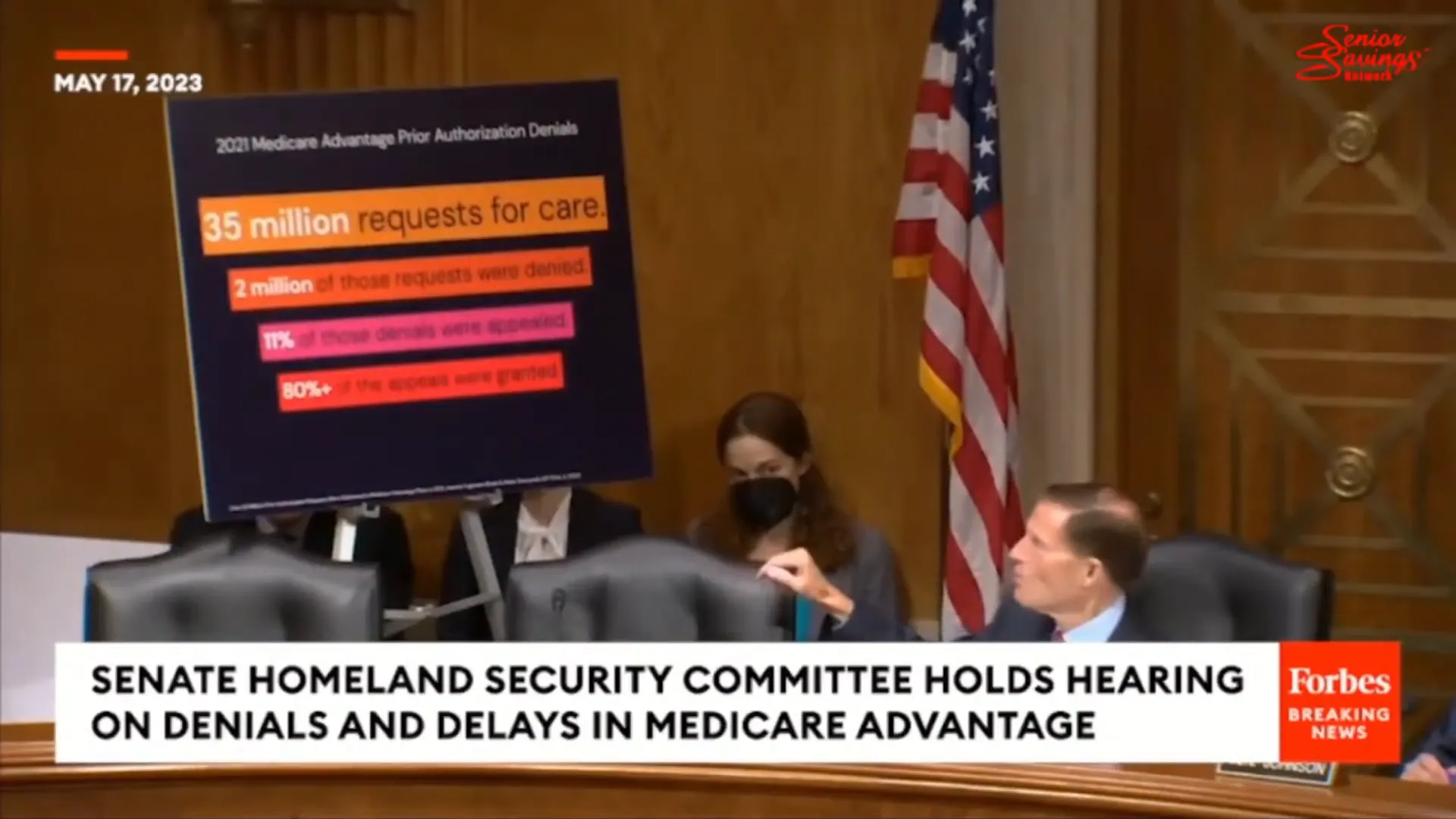

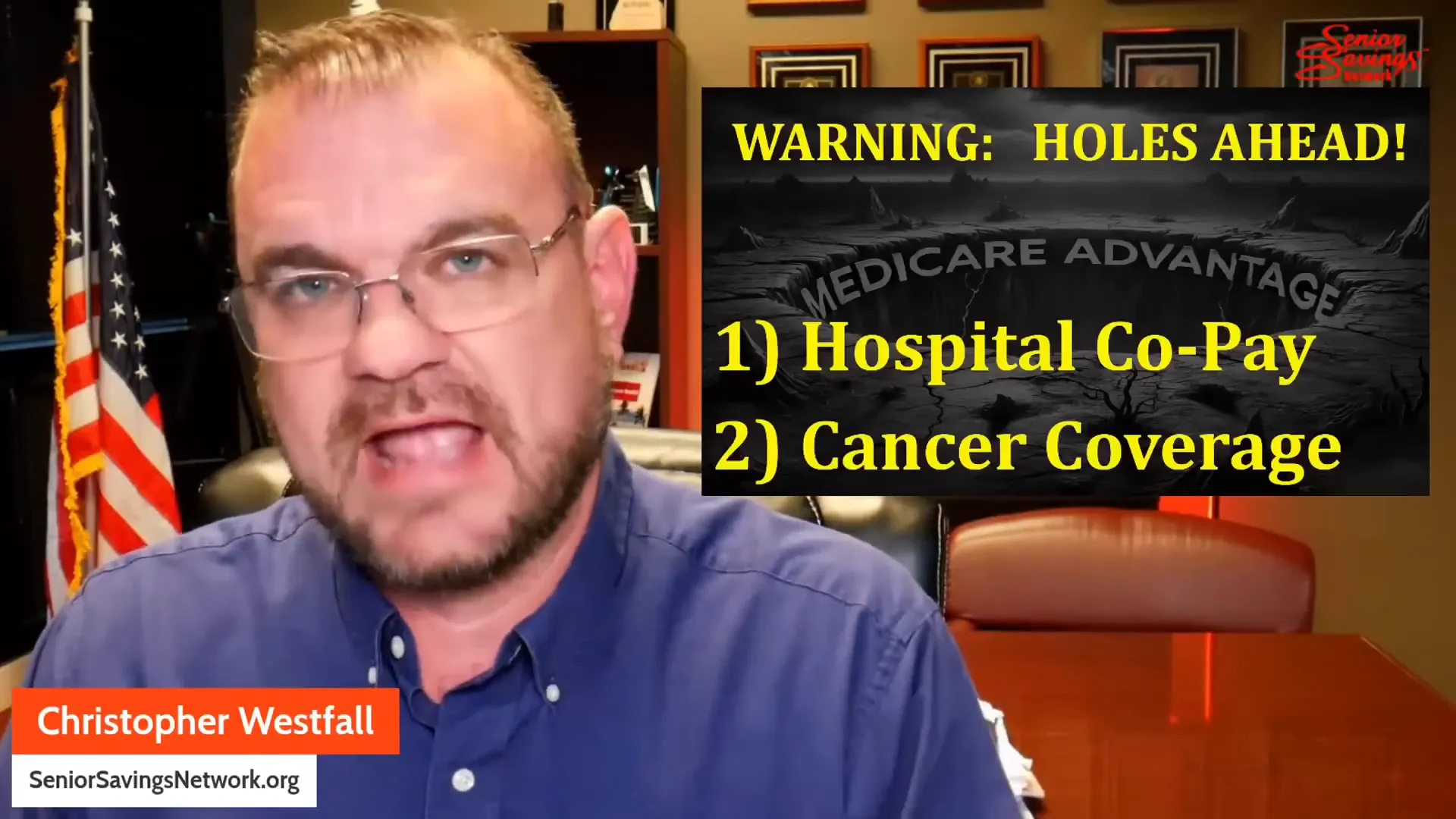

More consequentially, denials of prior authorization are common. Millions of authorizations are partially or fully denied each year. Those denials can delay essential treatments for weeks or longer, and the appeals process is complex and time-consuming. When a doctor prescribes a treatment because it is medically necessary, a prior authorization denial can feel like an arbitrary block to care. The cumulative effect is decreased access and increased stress for patients and clinicians alike.

Approvals Revoked, Appeals That Wear You Down

Even when a patient secures prior authorization, plans can revoke approvals. The appeals labyrinth is another harsh reality. Families report repeated, shifting denials and approvals that are then overturned, causing patients to cycle between hope and denial for weeks. The system can be so exhausting that some families stop appealing because the time, energy, and emotional toll are unsustainable.

One painful example involves a patient who needed extended inpatient rehabilitation after brain surgery. Under Original Medicare, such care would commonly be covered for the medically necessary duration. Under Medicare Advantage, the plan initially approved a short stay, then repeatedly denied extensions. The family won a couple of appeals but ultimately lost later ones. The patient was discharged prematurely and returned to the hospital within hours with life-threatening complications. That family attributes some of the decline and trauma to the exhausting fight over needed care.

External Reviewers, Algorithms, and the Illusion of Neutrality

Many denials are generated by third-party contractors using algorithmic tools to predict lengths of stay and service needs. Those algorithms examine millions of past data points to predict expected utilization, but they are not substitutes for individual clinical judgment. At appeal stages, quality improvement organizations or external reviewers often uphold initial denials, sometimes with minimal explanation. Patients and families face an uphill battle convincing reviewers that the unique facts of a case warrant more time or a different treatment path.

That process creates a chilling effect for clinicians. Physicians may hesitate to prescribe or recommend certain services they believe are appropriate if the path to approval is uncertain and the appeals process is onerous. Patients caught in that system can end up making impossible choices: remain in a facility and pay thousands out of pocket while continuing to appeal, or go home against medical advice without the necessary support for recovery.

Impact on Hospitals and Health Systems

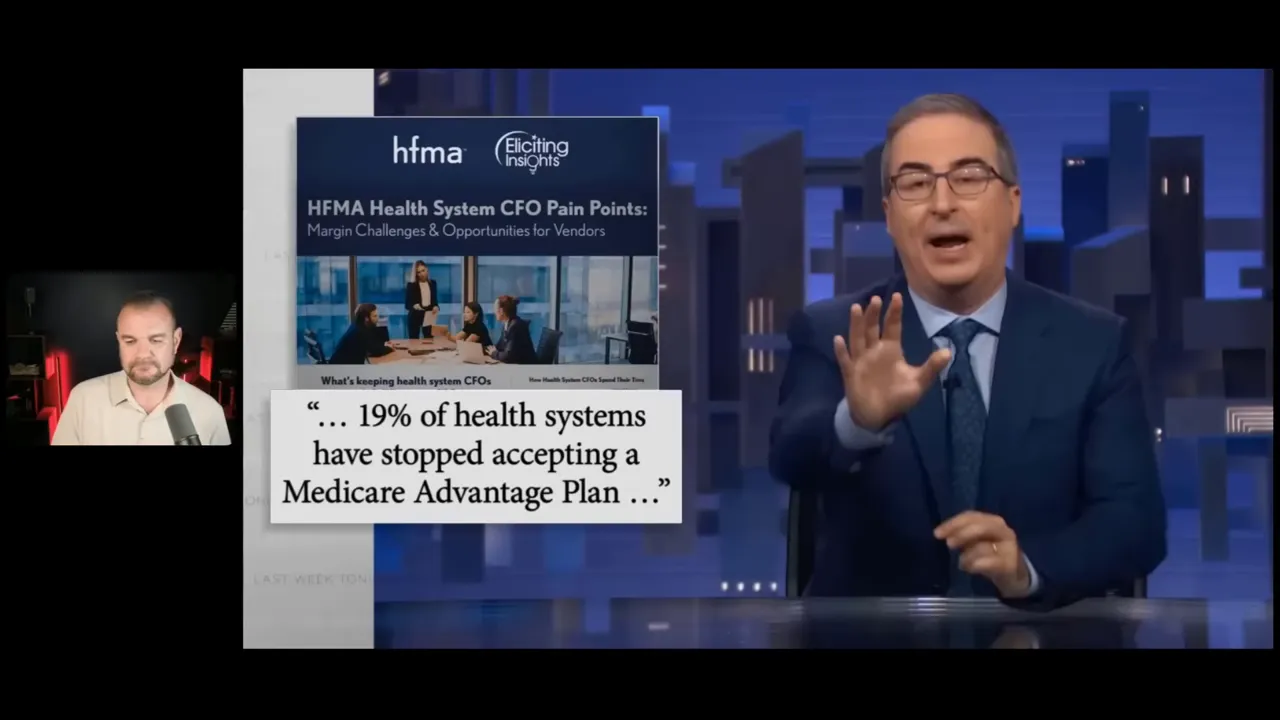

Denials and delayed payments also strain hospitals, especially smaller and rural systems. Hospitals have limited administrative bandwidth to repeatedly appeal plan decisions. Constant denials for inpatient stays, therapy services, or complex care can result in financial losses, cascading into reduced availability of services and even unit closures.

There are documented cases of entire hospital wings or units closing because reimbursements and payment delays rendered them unsustainable. Large academic systems have also publicly walked away from certain Medicare Advantage contracts after protracted negotiations, citing excessive prior authorization requirements, treatment denials, administrative burden, and delayed payment. Those contract disputes have consequences for patients who live near facilities that discontinue accepting certain plans.

Can You Leave Medicare Advantage? It Is Not Always Easy

One of the most common questions is whether someone can switch back from Medicare Advantage to Original Medicare. The technical answer is yes, but the practical answer is more complicated. There are limited enrollment windows when you can switch without underwriting consequences, and in many states, once you leave Medicare Advantage you may face barriers to obtaining a Medicare supplement plan.

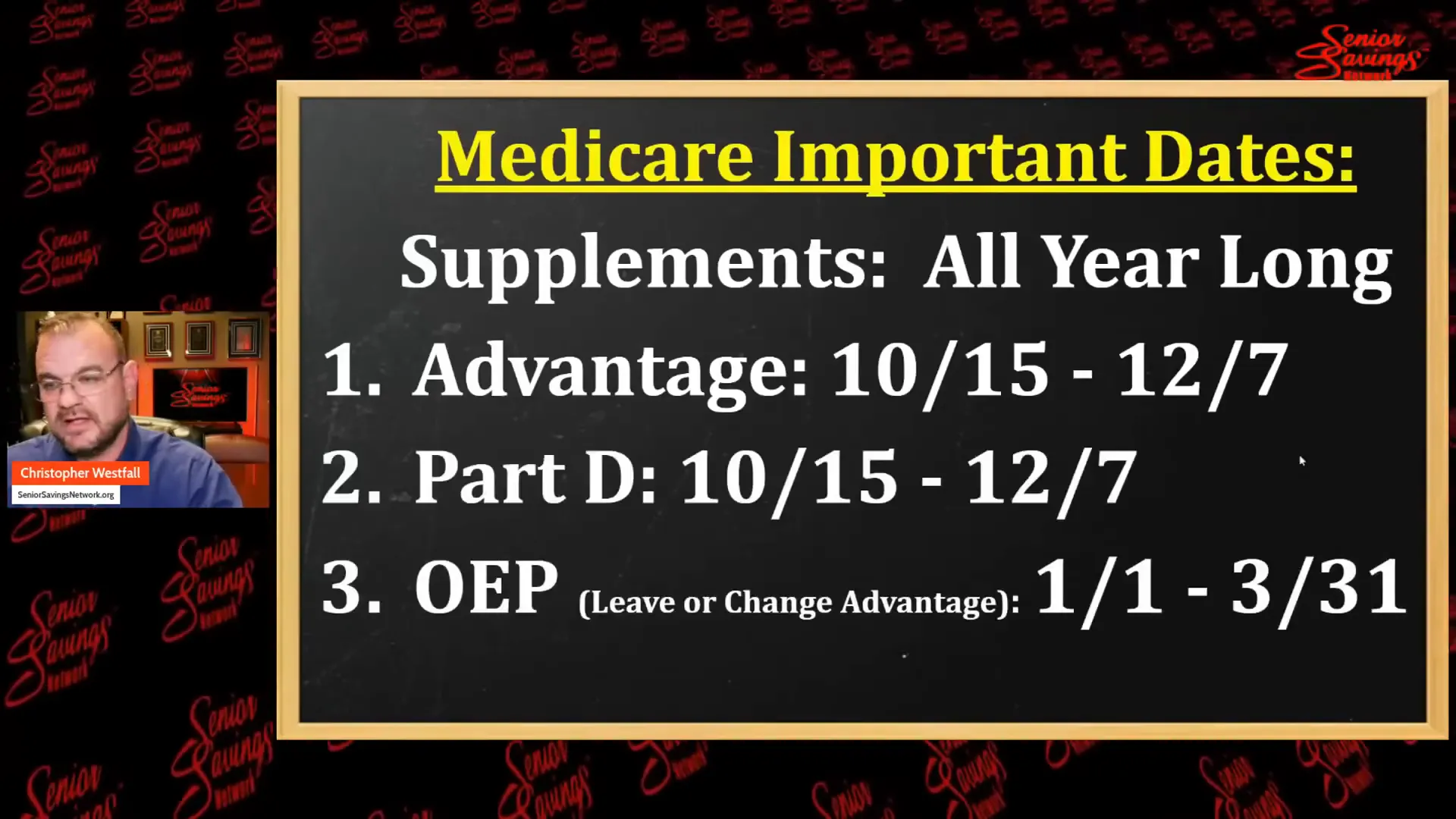

The key enrollment periods to remember are:

- Annual Election Period: October 15 through December 7. Any change selected during this window takes effect January 1 of the following year.

- Medigap Underwriting Window: January 1 through March 31. If you want to move back to Original Medicare and obtain a Medigap (Medicare supplement) policy, many insurers underwrite applications and may deny coverage based on pre-existing conditions unless you have guaranteed issue rights or state-specific protections.

Medigap plans can protect you from the 20 percent Part B coinsurance and large hospital deductibles, but insurers can, in most states, decline applicants who previously enrolled in Medicare Advantage. Some states offer protections like birthday rules that make switching easier, but that patchwork of state policies means outcomes vary widely. The practical advice: don’t abandon a Medicare Advantage plan until you have a confirmed, approved replacement plan in hand. Underwriting decisions should be finalized before you give up the coverage you currently have.

Underwriting Basics: What Can Lead to a Decline?

If you hope to purchase a Medigap policy after leaving Medicare Advantage, you will likely face underwriting unless you have a guaranteed issue right. Underwriting typically involves health questions about heart attacks, strokes, cancer within recent years, chronic conditions such as rheumatoid arthritis, and sometimes even height and weight. Recent serious illnesses within five years frequently lead to declines. That creates a perverse situation where people who chose Medicare Advantage when they were healthy cannot get back into a supplement once they become sicker.

An independent broker who understands multiple carriers can guide applicants toward companies that historically are more willing to accept certain conditions. That knowledge can be invaluable: two insurance companies might offer the same named plan, but one carrier’s underwriting practices could be more accepting than the other’s. Applying blindly at medicare.gov without a broker’s insight can lead to a surprising denial and leave people trapped in a plan that no longer meets their needs.

Practical Alternatives: High Deductible Plan G and Other Options

For those who want protection against large out-of-pocket costs but must balance monthly affordability, a high deductible Plan G can be a strong compromise. Plan G is a Medigap policy that covers almost everything Original Medicare does, except for the Part B deductible — which Plan G covers, but only after the high deductible is met in the high deductible version.

The high deductible Plan G typically has a very low monthly premium, often between $40 and $80 depending on age and geography. You pay medical costs out of pocket up to the deductible amount, and once you meet that threshold, the supplement pays the rest for the year. Conceptually, it behaves like a safety net: you have the low monthly cost of a less comprehensive plan combined with catastrophic protection in case of a severe health event.

There are major advantages to Plan G compared with Medicare Advantage:

- No networks. You can see any provider who accepts Medicare anywhere in the country. That is especially important for travel, second opinions, or specialists at major academic centers.

- Minimal prior authorization interference. Original Medicare generally pays for services that Medicare considers medically necessary without gatekeeping from insurers.

- Predictable cost structure and a clearer contract. The rules of Original Medicare do not change yearly in the same way plan networks and covered services can vary under Medicare Advantage.

The main tradeoff is monthly premium. For many beneficiaries, the choice is between a zero-premium Medicare Advantage plan with more restrictions and a modest premium for a Medigap policy that preserves flexibility. If you can afford a supplement, it is often the safer bet for long-term peace of mind.

How to Think Through the Decision: A Decision Framework

Choosing between Medicare Advantage and Original Medicare with a supplement is not purely a financial decision. It is a strategic one that involves projecting possible healthcare needs, weighing risk tolerance, and understanding practical enrollment rules.

Use this checklist to evaluate your options:

- Assess your current and projected health needs. Do you have chronic conditions that require specialists? Do you expect to need long-term therapy or rehabilitation in the future?

- Check provider network accuracy. Don’t take directories at face value. Call the specialists and hospital billing departments to confirm participation in a plan’s network.

- Ask detailed questions about prior authorization. Which services require prior authorization? How long is the typical turnaround? Are there documented denial rates?

- Investigate the plan’s health risk assessment and home visit practices. Who performs assessments, and what is recorded in medical records?

- Verify whether agents or nurses receive incentives tied to completing HRAs. Transparency about incentives is important for informed consent.

- Understand your state’s Medigap rules. Can you return to Original Medicare and obtain a Medigap policy if needed? What underwriting standards apply?

- Talk to an independent broker. Brokers who represent multiple carriers can match underwriting profiles to likely-accepting carriers, helping you avoid a bad move.

- Plan for the long term. If you are 65 and healthy, ask whether the plan you pick will serve you equally well if your health changes in five to ten years.

Why an Independent Broker Matters

Independent brokers who understand the entire market add real value. They can advise on which carriers historically underwrite more leniently for specific conditions and which plans have better track records with networks and claim handling. Brokers can also time applications so that you have an approved replacement before canceling an existing plan. Good advice costs you nothing directly — commissions are typically paid by the carrier — but the correct guidance can prevent costly mistakes.

Without that guidance, people often make decisions based purely on monthly premiums or the allure of added perks like fitness memberships and dental. Those perks are nice but can become irrelevant if a serious medical need appears and the plan’s network or prior authorization rules limit care or impose high out-of-pocket costs.

What Regulators and Policymakers Can Do

The problems in Medicare Advantage are structural, not incidental. Solutions require alignment of incentives and stronger oversight. Some potential reforms include:

- Improving audit transparency and transparency of risk adjustment methodologies to catch and deter improper coding and upcoding.

- Reforming incentives tied to HRAs and home visits so that documentation reflects verified clinical diagnoses rather than revenue-maximizing prompts.

- Mandating provider directory accuracy with real penalties for outdated information and guaranteed appointment access standards for critical specialties like mental health.

- Limiting or standardizing prior authorization processes to reduce administrative burden and ensure medically necessary care is not delayed.

- Providing clearer, more accessible appeal routes with independent clinical reviewers who must explain denials transparently.

These steps would not eliminate private plans from Medicare, but they would reduce the worst abuses and protect beneficiaries who are least able to advocate for themselves.

Common Objections and Honest Responses

Many beneficiaries report excellent experiences with Medicare Advantage. That feedback is real and important to acknowledge. For a healthy, active 66-year-old who primarily needs preventive care and likes premium-free plans with lifestyle perks, an Advantage plan can deliver satisfaction for many years. But the issue is survivorship bias: those who have great experiences and rarely need specialty or inpatient care will report high satisfaction. The people most harmed are often those whose complex, expensive needs expose the limits of networked, capitation-driven plans.

Industry-funded studies sometimes claim that Medicare Advantage saves the government money and delivers equal or better outcomes than Original Medicare. Independent reviewers frequently find bias or methodological flaws in those studies. That does not automatically mean all MA plans are bad, but it should temper claims of broad superiority until transparent, unbiased evidence demonstrates otherwise.

How to Protect Yourself: Practical Next Steps

If you are considering Medicare choices today, here is a step-by-step action plan:

- Inventory your current providers and ask whether they accept the plan you are considering. Call the provider’s billing office for confirmation rather than relying on printed directories.

- Ask the plan to explain which services require prior authorization and what the appeals process looks like, including typical timelines.

- Find out who conducts HRAs and home visits. Ask what is documented and request copies of any record that would enter your medical chart.

- Contact an independent broker to review both MA plans and Medigap options. Ask the broker about state-specific underwriting rules and which carriers tend to underwrite more favorably for your conditions.

- If you prefer Original Medicare but need to reduce premiums, consider high deductible Plan G as a compromise that maintains provider freedom while offering catastrophic protection.

- If you are already on MA and thinking of leaving, do not cancel without confirmed approval for a replacement plan. Apply during the Annual Election Period and consider the Jan 1–Mar 31 window for Medigap underwriting where applicable.

- Retain records of any home visit or HRA conversation. If you find questionable diagnoses in your chart, request full medical records and correct them promptly with your provider and insurer.

Final Takeaway: Go In Eyes Wide Open

Medicare Advantage has grown quickly because of marketing, perceived convenience, and some real advantages for healthy seniors. But beneath the surface are practices shaped by capitation and revenue incentives. These include aggressive diagnosis coding, questionable use of home visits, inaccurate provider directories, restrictive networks, pervasive prior authorization, and an appeals process that can feel designed to wear patients and families down. Hospitals and providers have responded, in some cases refusing contracts with certain plans because of the administrative weight and reimbursement disputes.

The most important message is simple: go in eyes wide open. If you choose Medicare Advantage, make that choice deliberately and with full understanding of the tradeoffs. If you value unrestricted provider access, predictable coverage for big events, and minimal prior authorization risk, Original Medicare combined with a Medigap policy or a high deductible Plan G may be the safer long-term choice.

When making the decision, get help from a knowledgeable, independent broker, confirm provider participation directly, understand enrollment windows and underwriting rules, and document all interactions that could influence your medical record. Insurance is about risk and tradeoffs. For some people, Medicare Advantage is a workable tradeoff. For many others, especially those approaching more complex healthcare needs, the cost of that tradeoff is too high.

If you want practical help reviewing your options, consider contacting an independent, experienced broker who can compare carriers, explain underwriting, and help you avoid costly mistakes. A well-informed decision now can preserve both your peace of mind and your access to care when you need it most.

Thanks for reading. Be cautious, ask questions, and don’t let a catchy name alone determine the future of your healthcare coverage.

What John Oliver Just Revealed About Medicare Read More »