Major Changes in Prior Authorization for Medicare Advantage: What You Need to Know

Hello, I’m Christopher Westfall from Senior Savings Network. Today, I want to dive deep into a major development that’s shaking up the world of health insurance, specifically Medicare Advantage, and it involves something called prior authorization. You may have heard the buzz with RFK Jr. and Dr. Oz announcing reforms, but is everything really fixed now? Let me walk you through the details that most won’t tell you.

Prior authorization has long been a thorn in the side of patients, doctors, and even insurance companies. It’s a process where your health insurance plan needs to approve certain medical services or treatments before you can get them. While it’s meant to control costs and ensure appropriate care, it often causes frustrating delays—sometimes lasting weeks or longer. For Medicare Advantage patients, these delays can be especially stressful.

Let’s unpack what’s changing, what remains voluntary, and what you should watch out for when choosing your Medicare coverage.

Table of Contents

- 📢 The Big Announcement: RFK Jr. and Dr. Oz on Prior Authorization Reform

- 🔄 Continuity of Care and the 90-Day Transition Promise

- 🩺 Medical Review Over AI: Who Denies Claims?

- 📋 Is Your Medicare Advantage Plan Participating? Check the List

- 😡 Why Prior Authorization Frustrates Patients and Providers

- ⚠️ The Truth Most Medicare Agents Won’t Tell You About Prior Authorization

- 🏛️ Congress Weighs In: Doctors Speak Out on Prior Authorization

- 📊 How Are Medicare Advantage Companies Doing on Prior Authorization?

- 💸 Medicare Advantage Agents Just Got a Raise: What That Means for You

- 📉 Medicare Supplement Plan G vs. Plan N: What Agents Don’t Tell You

- 🕒 Medicare Supplement Changes Can Be Made Anytime, Not Just During Fall

- 🤝 Why It Pays to Get a Second Opinion on Your Medicare Coverage

- 🔍 Summary: What You Should Know About Prior Authorization and Medicare Advantage

- ❓ Frequently Asked Questions about Prior Authorization and Medicare Advantage

- 🙏 Final Thoughts

📢 The Big Announcement: RFK Jr. and Dr. Oz on Prior Authorization Reform

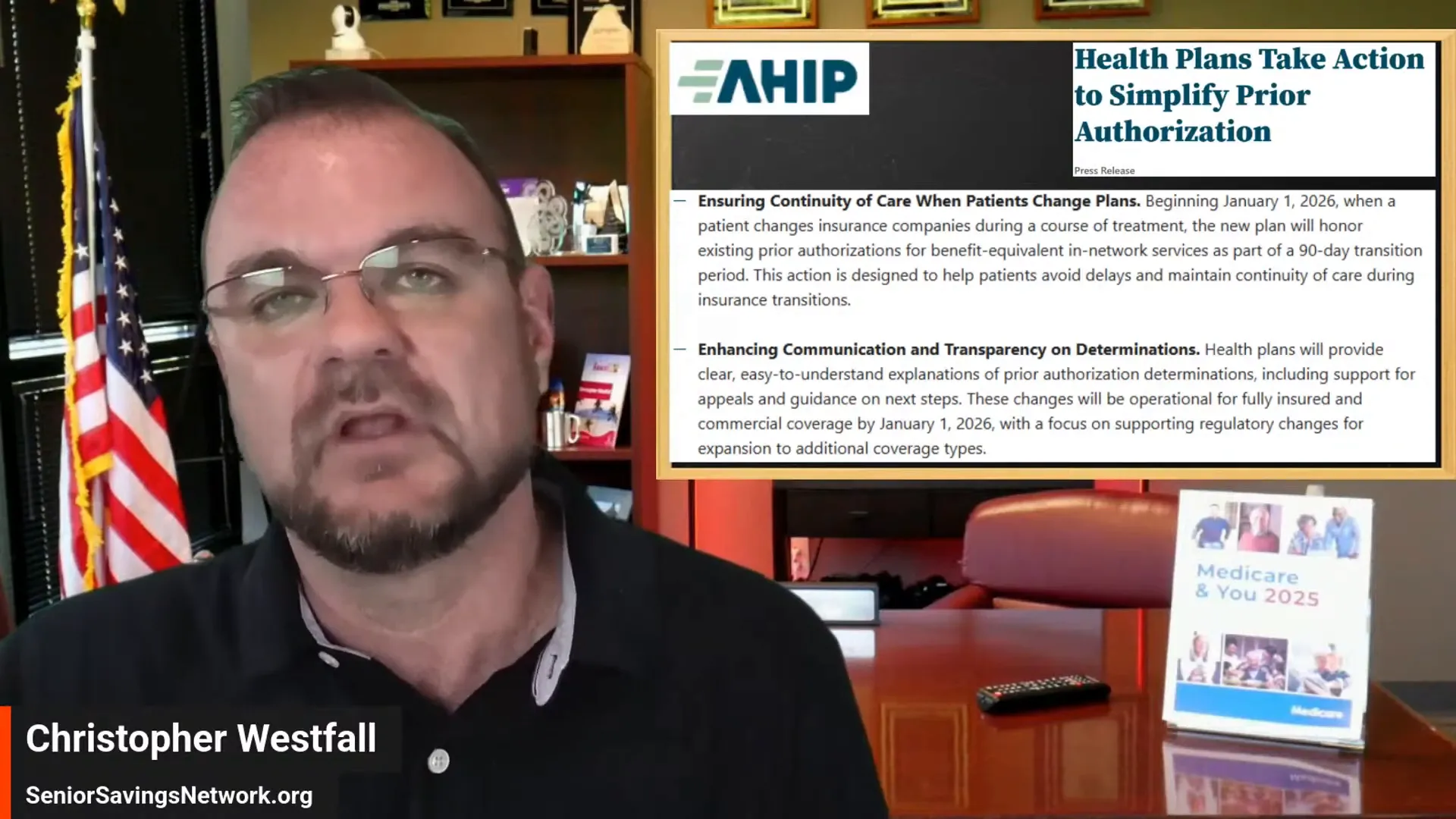

Earlier today, news outlets everywhere were buzzing about a joint announcement from RFK Jr. and Dr. Oz regarding changes to prior authorization in health insurance, especially Medicare Advantage. This announcement came through a press release from AHIP, the industry’s main spokesperson group. AHIP revealed that insurance companies are pledging to standardize the prior authorization process electronically by 2027.

Why does this matter? Right now, prior authorization is a chaotic mess. One insurance company might require a fax, another a phone call, and a third might have an entirely different electronic system. This patchwork creates confusion for providers and patients alike. The promise is to streamline this into one standardized electronic system, making it simpler and faster.

Dr. Oz also mentioned the goal of drastically reducing the number of procedures and plans that require prior authorization—from thousands down to about 500. While that sounds like a huge win, it’s important to note this change is voluntary and might only start happening in January 2026.

🔄 Continuity of Care and the 90-Day Transition Promise

One of the more hopeful parts of this announcement is around continuity of care. Imagine this scenario: You’re enrolled in a Medicare Advantage plan, and after a long prior authorization process, you finally get approval for an expensive treatment like chemotherapy or a costly medication. But it’s late in the year, and you’re thinking about switching to a different Medicare Advantage plan for the next year.

What happens to your treatment? Will your new insurance company honor the prior authorization you worked hard to get?

The pledge from participating insurance companies is to honor a 90-day transition period at the start of the year, allowing your treatment to continue without interruption as you switch plans. This is a big deal if it actually happens. In addition, insurers promise to provide clearer, easier-to-understand explanations when a prior authorization request is denied, outlining exactly what documentation is missing or needed to get approval.

Again, these changes are voluntary and won’t be fully realized until 2027, when they expect 80% of prior authorization approvals to be instant through real-time electronic responses.

🩺 Medical Review Over AI: Who Denies Claims?

Another important part of the pledge is that all denied prior authorization requests based on clinical reasons will continue to be reviewed by medical professionals, not just automated AI programs. This means if your request is initially denied, it should be reviewed by a doctor or medical reviewer to make sure the denial is fair and justified.

This is a crucial reassurance because many patients and doctors fear that automated denials happen without proper clinical oversight, leading to unnecessary delays or refusals of care.

📋 Is Your Medicare Advantage Plan Participating? Check the List

Since these reforms are voluntary, not every Medicare Advantage plan is onboard. To find out if your plan is participating, you can check an updated list provided by AHIP. I’ve linked it below for easy access, and you can also find it in the description of this post.

Knowing if your insurance company has pledged to follow these new rules can help you decide if your current plan will offer a smoother prior authorization experience or if you might want to consider alternatives.

😡 Why Prior Authorization Frustrates Patients and Providers

Dr. Oz summed up the patient experience well during his recent senate confirmation hearing. Imagine sitting in a doctor’s office with a serious diagnosis, and you and your doctor agree on a treatment plan. Then you learn you can’t start treatment for weeks or longer because your insurance hasn’t approved it yet. That frustration is overwhelming because it’s one of the few things you can’t control when facing a health crisis.

Secretary Xavier Becerra (who oversees HHS) also highlighted the burden prior authorization places on providers. He shared that 85% of Americans report delays in care due to prior authorization, and doctors spend 12-15 hours a week just filling out these forms. Nurses often spend over half their time managing prior authorization paperwork instead of patient care.

This administrative burden adds up to wasted resources and delayed care for millions of Medicare Advantage patients.

⚠️ The Truth Most Medicare Agents Won’t Tell You About Prior Authorization

Here’s a message many Medicare Advantage agents won’t share: Prior authorization is optional. It’s a feature tied only to Medicare Advantage plans. These plans determine the type of care you receive, when you begin treatment, and what documentation is required before your treatment is approved. Their profit depends on how much money they receive from the government minus what they pay for your care. So, they have a financial incentive to limit or delay care when possible.

If you choose original Medicare instead, which you’ve paid into your whole life, you can pair it with a Medicare Supplement plan (also known as Medigap). This combination:

- Covers the 20% that original Medicare doesn’t pay

- Grants you access to virtually all doctors and hospitals nationwide (as long as they accept Medicare)

- Has no networks, no prior authorizations, and no restrictions

For many, this is a less frustrating, more flexible option than Medicare Advantage with its prior authorization hurdles.

🏛️ Congress Weighs In: Doctors Speak Out on Prior Authorization

Two members of Congress who are also physicians have spoken out strongly against prior authorization in Medicare Advantage. Here’s what they said:

“I have had innumerable episodes where patients call back crying or upset that their insurance company would not allow a treatment plan that I, as their trusted physician, recommended.” – Congressman Doctor Marshall

“We must prioritize patients’ health over corporate profits and arbitrary cost-cutting measures. For nearly my entire time in Congress, I fought to reform the prior authorization process in Medicare Advantage.” – Congresswoman (name not specified)

These voices highlight the ongoing struggle between patient care and insurance company cost controls.

📊 How Are Medicare Advantage Companies Doing on Prior Authorization?

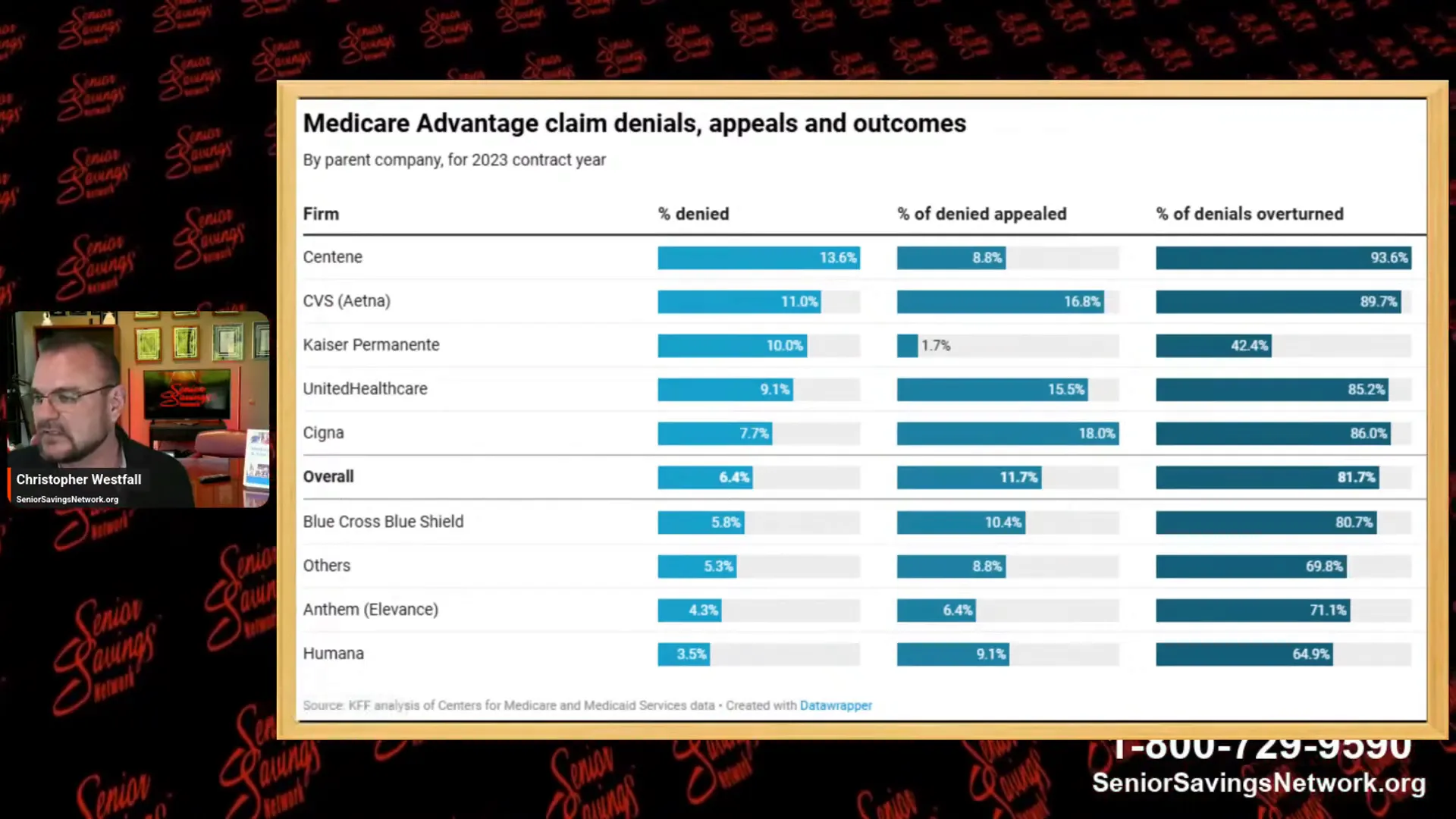

Let’s look at some data showing how often Medicare Advantage companies deny initial prior authorization claims and how often appeals overturn those denials.

- Centene: Denies 13.6% of claims; 8% of people appeal; 94% of appeals are approved—meaning most denials were wrong initially.

- CVS/Aetna: Denials near Centene’s rate.

- Kaiser Permanente (nonprofit): Denies 10% of claims.

- UnitedHealthcare: Denies 9.1% of claims.

- Cigna: Denies 7.7% of claims.

- Blue Cross Blue Shield and Anthem: Better than average denials.

- Humana: Denies fewer claims, and when they do, 64% of appeals are successful—indicating their denials are more often justified compared to others.

This data shows that while denials happen, appealing is critical because the vast majority of appeals are successful. If your claim is denied, don’t hesitate to appeal—it’s often the fastest path to getting the care you need.

💸 Medicare Advantage Agents Just Got a Raise: What That Means for You

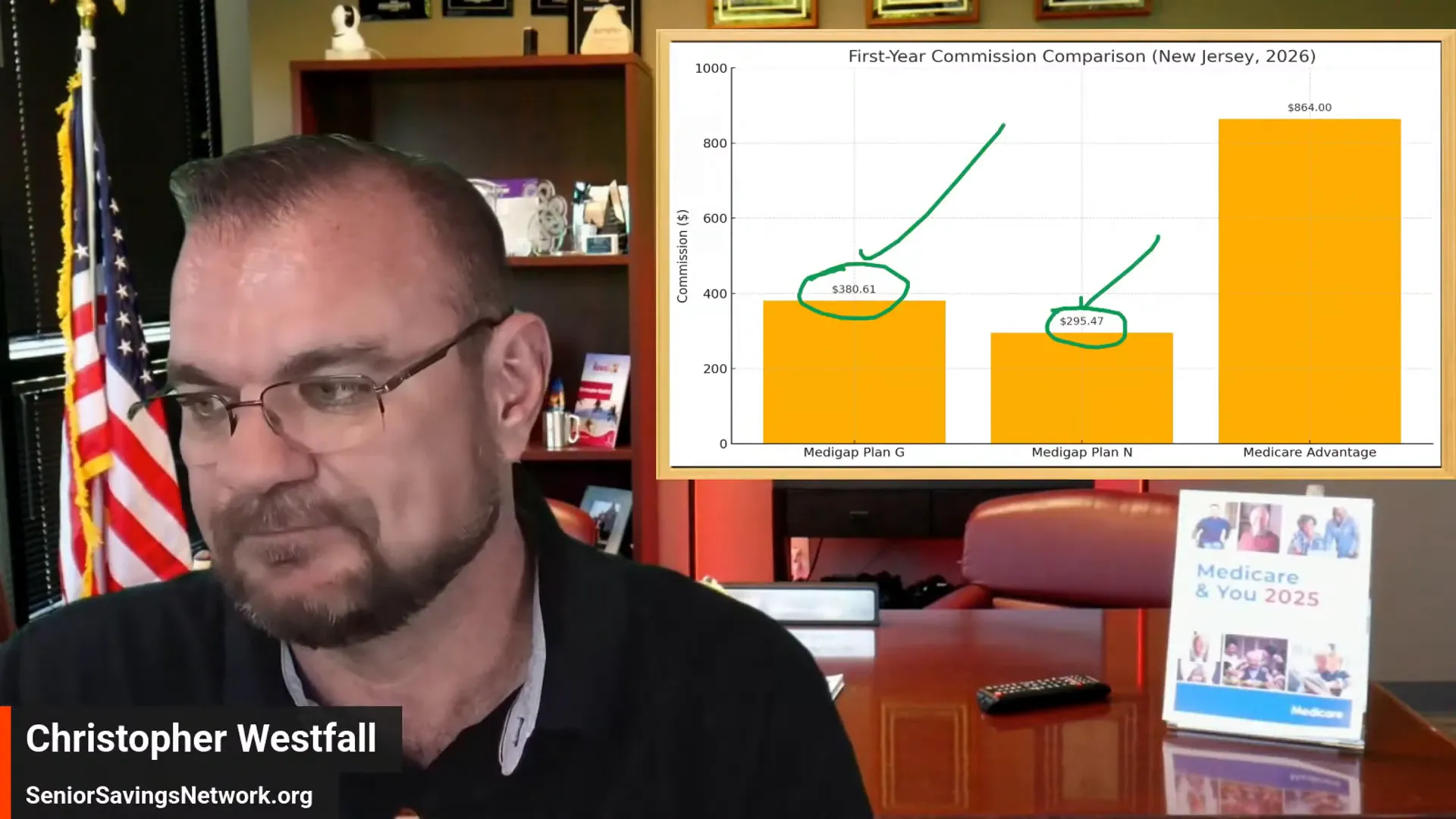

Here’s a little-known fact about Medicare Advantage: The agents who enroll you in these plans often make significantly more commission than agents who sell Medicare Supplement plans. Recently, commissions for Medicare Advantage sign-ups in 2026 have gone up, especially in states like Connecticut, Pennsylvania, DC, California, and New Jersey.

For example, the national maximum first-year commission for Medicare Advantage agents is $694; however, in some states, it can be significantly higher. Contrast that with Medicare Supplement Plan G, where the average commission is about $380 for the first year on an average premium of $1,447.

This financial incentive pushes many agents to focus heavily on Medicare Advantage plans, sometimes at the expense of presenting Medicare Supplement options that might better suit your needs.

📉 Medicare Supplement Plan G vs. Plan N: What Agents Don’t Tell You

When insurance agents DO bring up Medicare Supplements, they will talk about Medicare Supplement Plan G because it’s easy to explain—it covers almost everything after Medicare pays its share. But there’s a catch: Plan G premiums have been rising dramatically. Some states have seen rate increases of up to 40% in just a few years.

Plan N is a lesser-known Medicare Supplement option that often gets overlooked. It pays slightly less than Plan G but has historically had lower premium increases—around 28% compared to 40% for Plan G in some areas.

Why don’t more agents talk about Plan N? Because it pays them less commission, even though it could save you money in the long run.

For more information on Plan N, check out PlanNMedicare.org. It’s an excellent resource for learning about this lesser-known option that may be a better fit for your healthcare needs and budget.

🕒 Medicare Supplement Changes Can Be Made Anytime, Not Just During Fall

Unlike Medicare Advantage enrollment, which is often limited to specific periods, you can change your Medicare Supplement plan anytime during the year. This flexibility means you don’t have to wait for the annual open enrollment period to switch if you find a better plan or lower premiums elsewhere.

🤝 Why It Pays to Get a Second Opinion on Your Medicare Coverage

Choosing the right Medicare plan is a big decision, and with all the complexities involving prior authorization, commissions, and coverage options, it’s worth getting a second opinion. Even if you love your current plan and agent, a fresh perspective can reveal better options or help you save money.

Our office offers free consultations to review your Medicare coverage and help you understand your options—whether that’s Medicare Advantage, Medicare Supplement, or original Medicare. Our goal is to empower you with unbiased information, enabling you to make informed decisions for your health and finances.

🔍 Summary: What You Should Know About Prior Authorization and Medicare Advantage

- Prior authorization reforms announced by RFK Jr. and Dr. Oz aim to standardize and speed up approvals but are voluntary and won’t be fully in place until 2027.

- Continuity of care promises a 90-day transition period if you switch Medicare Advantage plans, but this also is voluntary.

- Medical professionals, not just AI should review denied claims, but this depends on insurer participation.

- Not all Medicare Advantage plans are participating in these reforms—check the AHIP list.

- Prior authorization causes significant delays and frustration for patients and providers alike.

- Original Medicare, combined with a Medicare Supplement plan, offers no prior authorization and no network restrictions.

- Appealing denied claims is essential, as most appeals are successful.

- Medicare Advantage agents earn higher commissions than Medicare Supplement agents, influencing plan recommendations.

- Medicare Supplement Plan N may offer a better long-term value than Plan G but is less promoted by agents.

- You can change Medicare Supplement plans anytime during the year.

- Getting a second opinion on your Medicare coverage can help you avoid pitfalls and find the best plan for you.

❓ Frequently Asked Questions about Prior Authorization and Medicare Advantage

What is prior authorization in Medicare Advantage?

Prior authorization is a process where your Medicare Advantage plan must approve certain medical services, tests, or treatments before you can receive them. It’s meant to control costs but often causes delays.

Are prior authorization reforms mandatory?

No, the recent reforms announced are voluntary commitments by some insurance companies and won’t be fully implemented until 2027 at the earliest.

Can I avoid prior authorization by choosing a different Medicare plan?

Yes. Original Medicare combined with a Medicare Supplement plan does not require prior authorization, giving you access to most doctors and hospitals without these hurdles.

What should I do if my prior authorization request is denied?

Always appeal the denial. More than 88% of appeals are successful, meaning you have a good chance of getting approval on appeal.

Why do Medicare Advantage agents push these plans more than Medicare Supplement plans?

Medicare Advantage agents typically earn higher commissions, especially in the first year, which influences their recommendations.

Can I change my Medicare Supplement plan anytime?

Yes, unlike Medicare Advantage, you can change your Medicare Supplement plan at any time during the year, not just during open enrollment.

Where can I check if my Medicare Advantage plan is participating in the new prior authorization reforms?

You can find an updated list on the AHIP website or linked resources provided by your insurance company or trusted Medicare advisors.

What is Medicare Supplement Plan N?

Plan N is a Medicare Supplement plan that covers most out-of-pocket costs but usually has lower premiums and lower rate increases than Plan G. It requires some copayments but can be a more affordable option for many.

For more detailed information on Plan N, visit PlanNMedicare.org.

🙏 Final Thoughts

Prior authorization has been a major source of frustration and delay in Medicare Advantage for years. While the recent pledge by insurers to reform this process is a step in the right direction, it’s voluntary and will take years to implement fully.

As someone who has worked with Medicare plans for years, I encourage you to consider your options carefully. Original Medicare with a Medicare Supplement plan can offer freedom from prior authorization and network restrictions, while Medicare Advantage may require you to navigate these hurdles.

If you’re approaching age 65 or currently on Medicare, take the time to understand what prior authorization means for your care and ask your agent the tough questions. If you want a free second opinion on your Medicare coverage, my office is here to help at no cost to you.

Thank you for reading. Stay informed and take control of your healthcare decisions.

— Christopher Westfall, Senior Savings Network 1-800-729-9590