Medicare’s New Prior Authorization Scheme: What You Need to Know

Medicare’s New Prior Authorization Scheme: What You Need to Know

Medicare is about to change in a big way, and if you or a loved one rely on Original Medicare, you’ll want to understand what’s coming. The Centers for Medicare & Medicaid Services (CMS) is rolling out a new prior authorization program called the WISeR Model—Wasteful and Inappropriate Service Reduction—that will impact millions of seniors starting in 2026. This new approach promises to crack down on waste, fraud, and abuse, but it also raises serious concerns about care delays and denials.

In this article, we’ll break down everything you need to know about this new Medicare prior authorization scheme, why it’s being introduced, how it compares to Medicare Advantage’s existing prior authorization policies, and what it means for you as a Medicare beneficiary. We’ll also share insights into the incentives driving this program and why some experts and advocates are worried about its impact on seniors’ access to care.

Let’s dive in.

Table of Contents

- Understanding Prior Authorization and Why It Matters

- The Big Surprise: Prior Authorization Coming to Original Medicare

- CMS’s June Press Conference vs. July Announcement: A Contradiction

- The Scourge of Prior Authorization: Voices from Providers and Patients

- What Exactly Is the WISeR Model?

- The True Incentives Behind WISeR: Payment Tied to Denials

- Who Are the Companies Running WISeR?

- How WISeR Could Impact Seniors

- Medicare Advantage vs. Original Medicare: A Growing Divide

- What You Can Do to Protect Yourself

- Frequently Asked Questions (FAQs)

- Conclusion: Stay Informed and Advocate for Your Care

Understanding Prior Authorization and Why It Matters

First, let’s clarify what prior authorization means in healthcare. Prior authorization is a process where your insurance company requires approval before certain medical services, procedures, or medications will be covered. It’s intended to prevent unnecessary or costly treatments, but in practice, it often leads to frustrating delays for patients and providers alike.

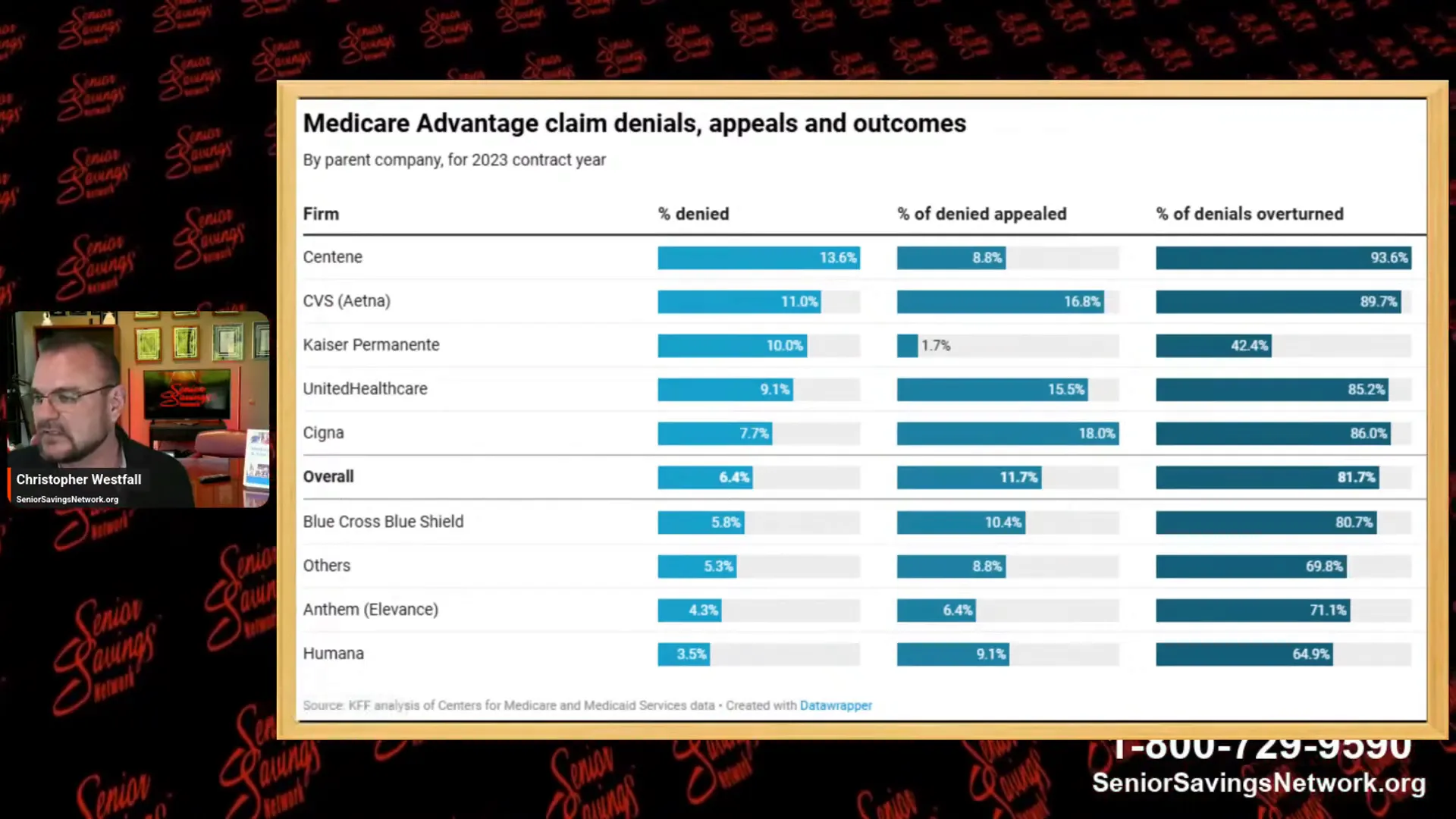

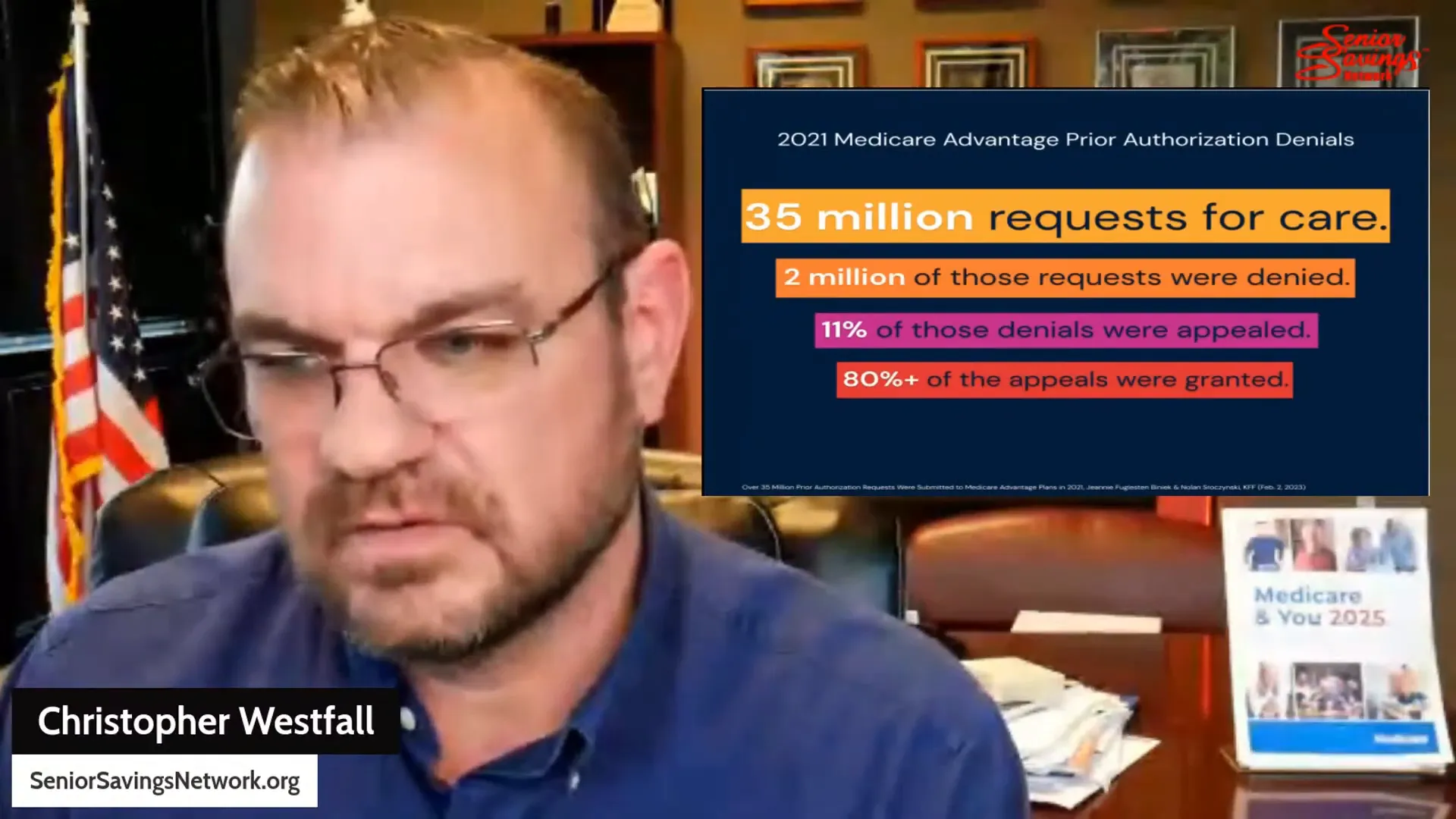

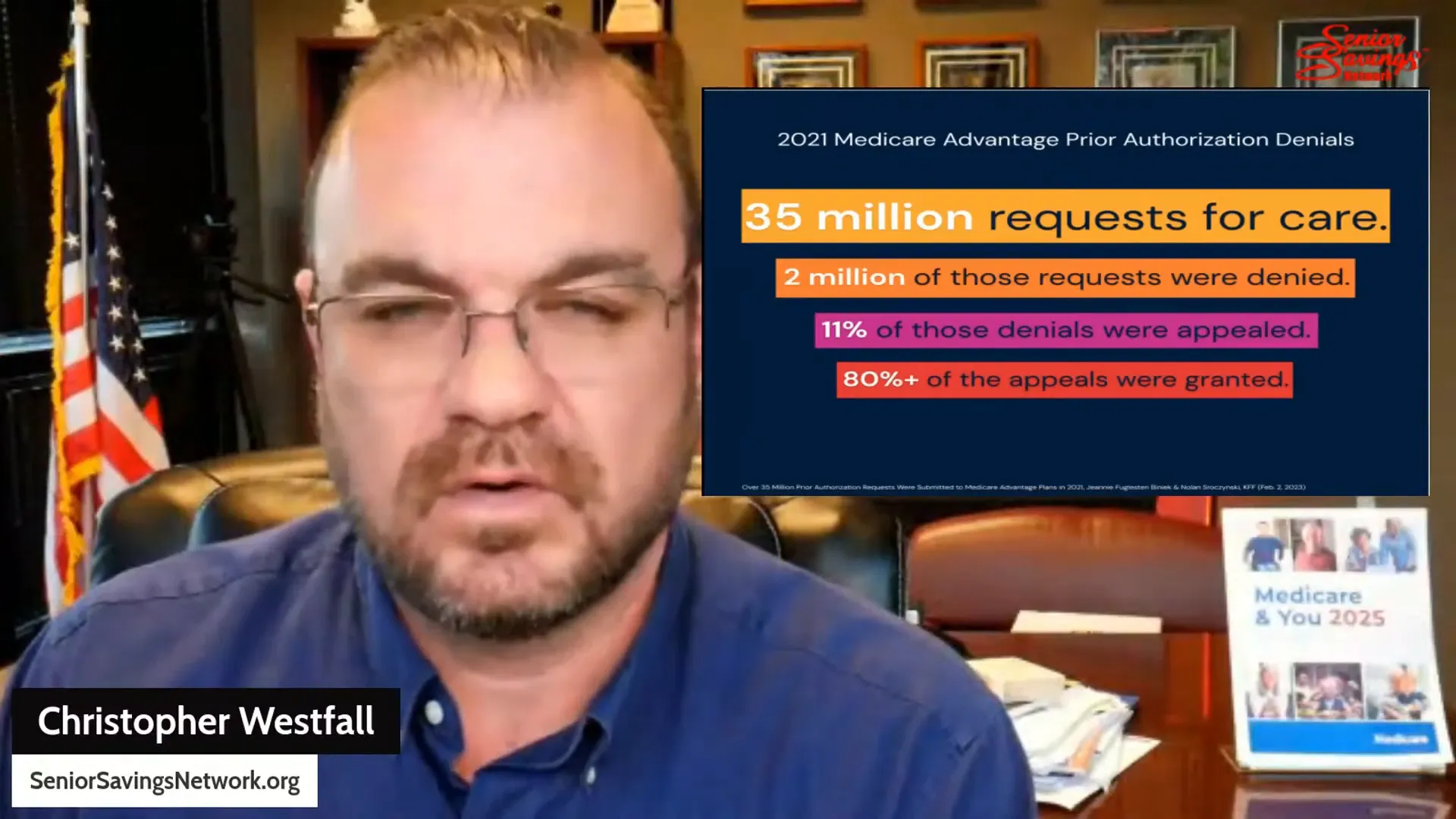

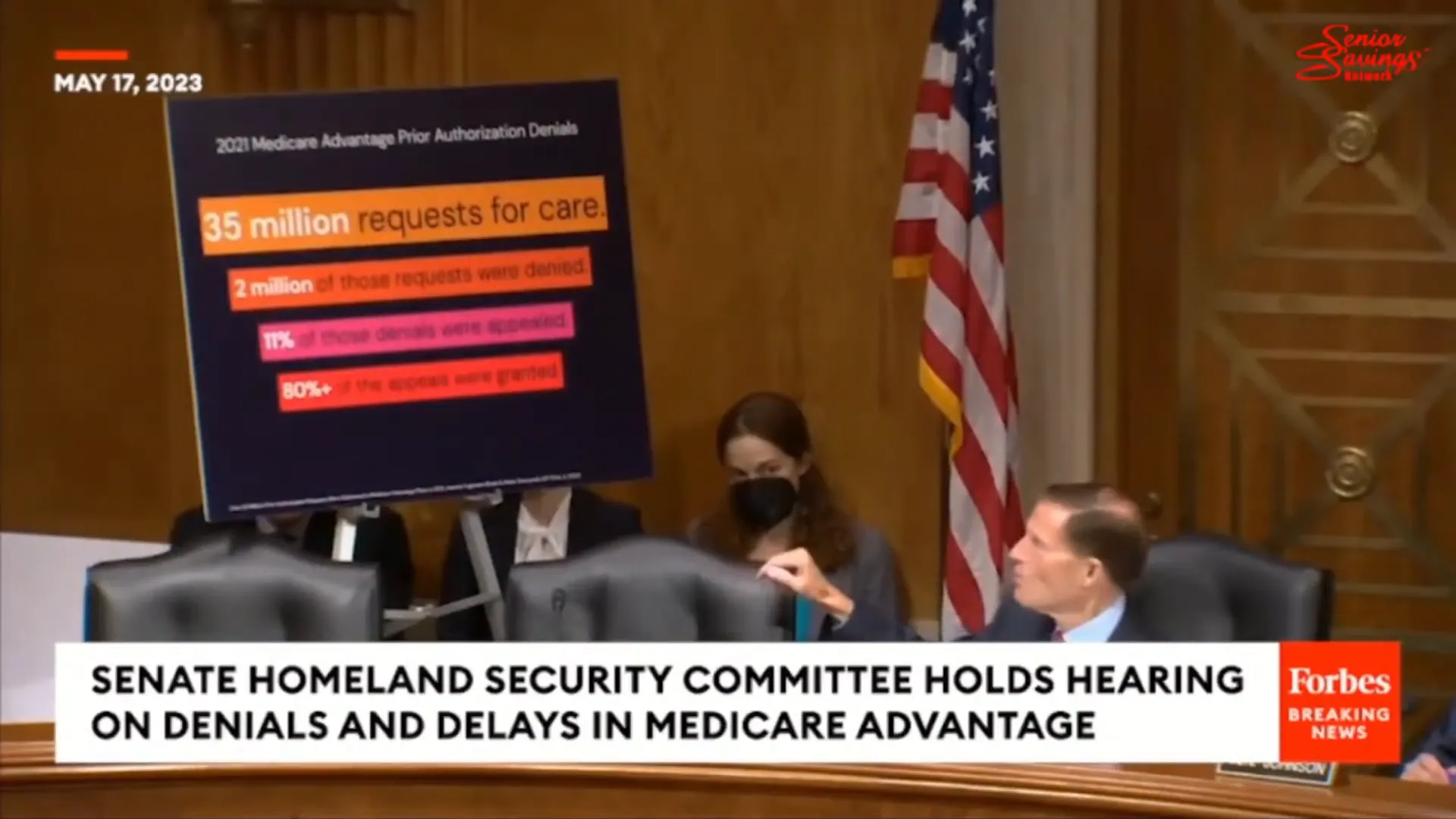

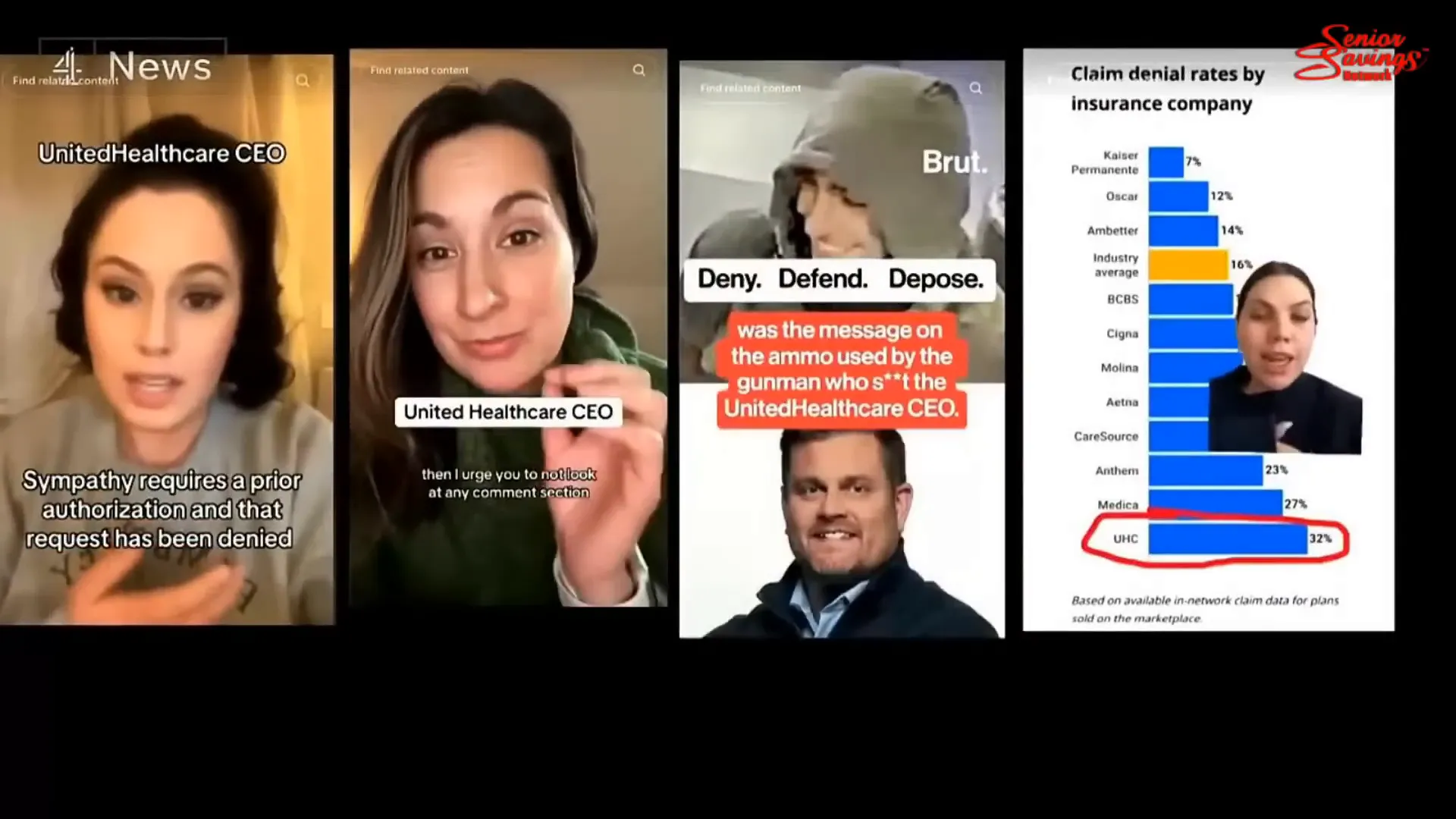

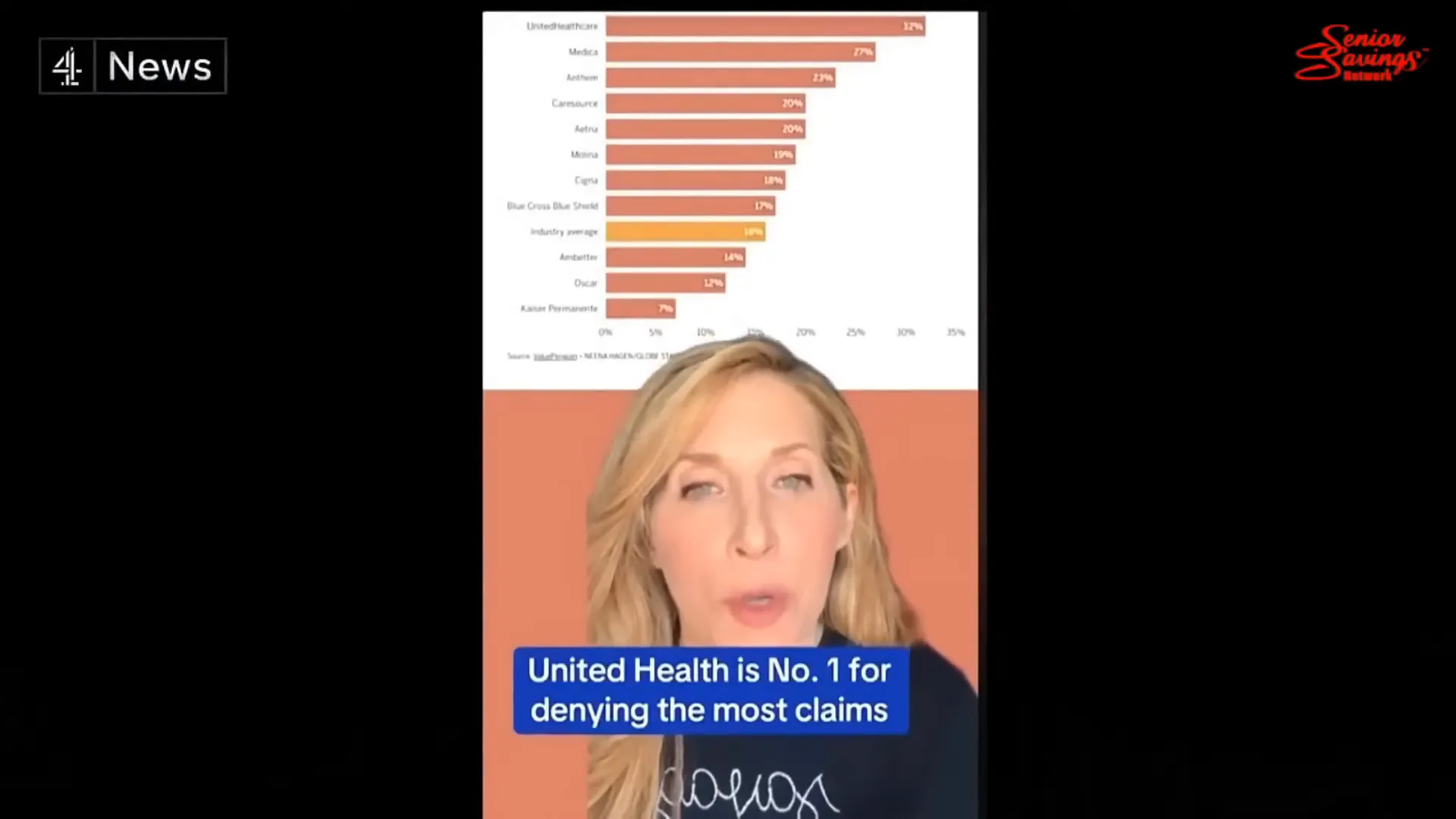

For years, prior authorization has been a major pain point in the Medicare Advantage program, which is the private insurance alternative to Original Medicare. Patients and doctors frequently complain about the paperwork, delays, and denials that come with prior authorization requests. In fact, surveys show that about 85% of Americans have experienced issues with prior authorization that negatively affected their care.

Doctors spend an average of 12 hours a week just dealing with prior authorization paperwork, which takes away time from patient care and adds to the administrative burden on healthcare providers. These delays can sometimes lead to significant harm, especially when urgent treatments are stalled.

The Big Surprise: Prior Authorization Coming to Original Medicare

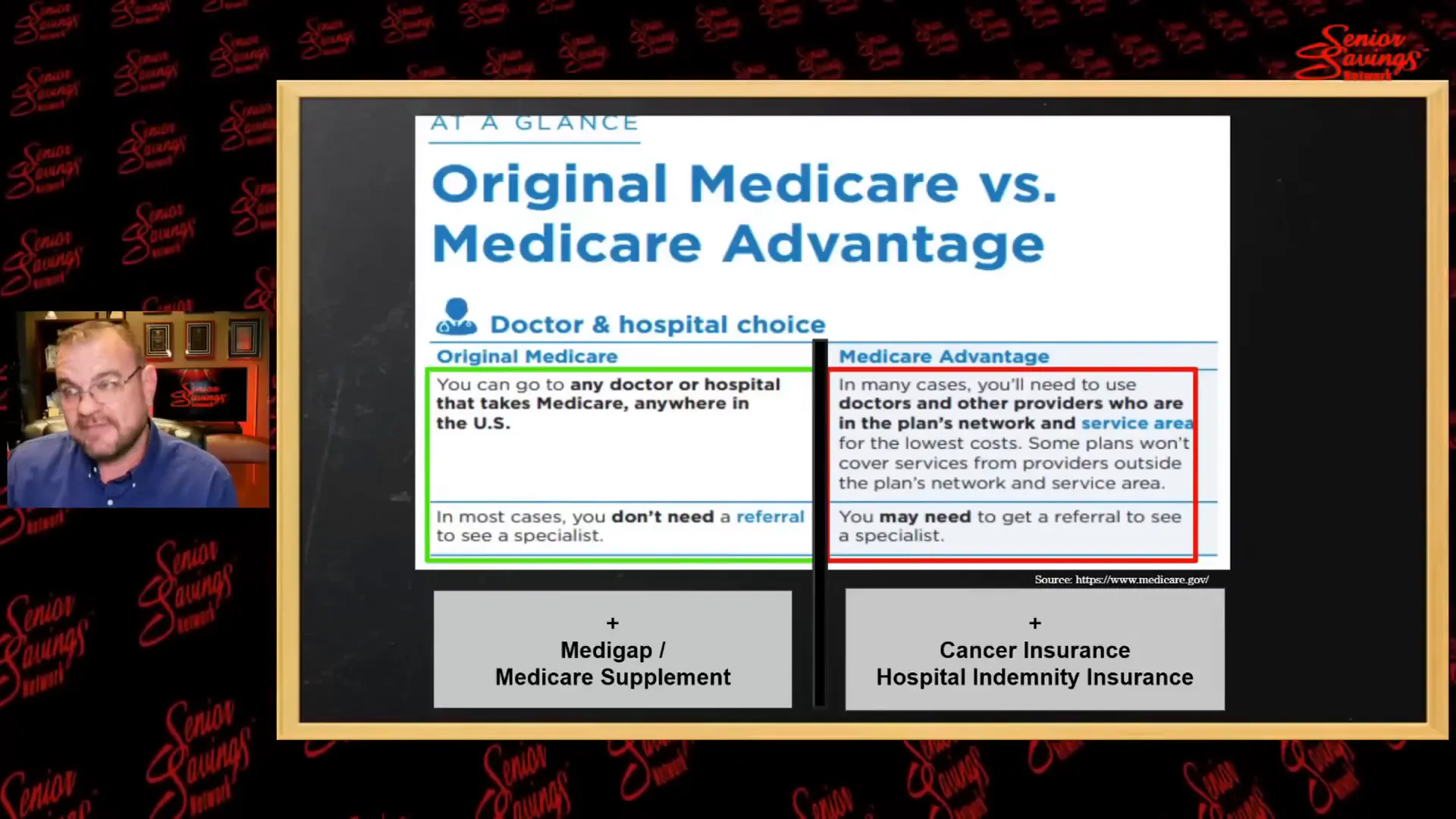

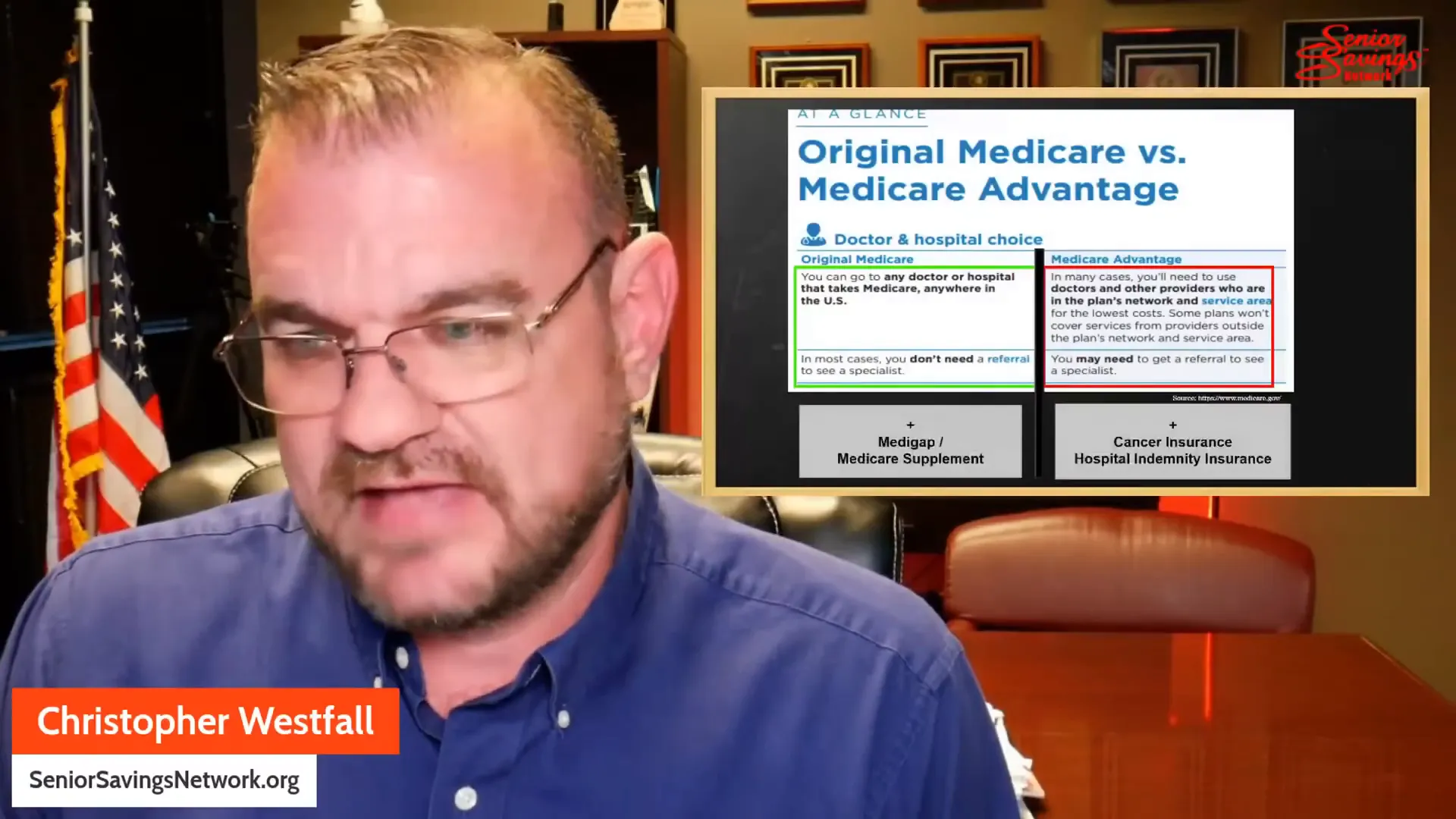

Original Medicare has traditionally been free from prior authorization requirements for most services. If you have traditional Medicare, you can generally expect coverage for up to 100 days of hospital or skilled nursing facility stays without the hassle of prior authorization. This contrasts sharply with Medicare Advantage plans, where prior authorization is routine and often results in denials before doctors even recommend discharge.

However, in July 2025, CMS announced plans to introduce prior authorization into Original Medicare through a new initiative called the WISeR Model. This move stunned many healthcare professionals and seniors alike because it extends a system that has long been criticized in Medicare Advantage into the traditional Medicare program.

The WISeR Model is designed as a trial program, initially affecting six states—Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington—and targeting 17 specific medical procedures and services. The goal is to reduce wasteful or inappropriate spending, but the way the program is structured raises questions about the true incentives behind it.

CMS’s June Press Conference vs. July Announcement: A Contradiction

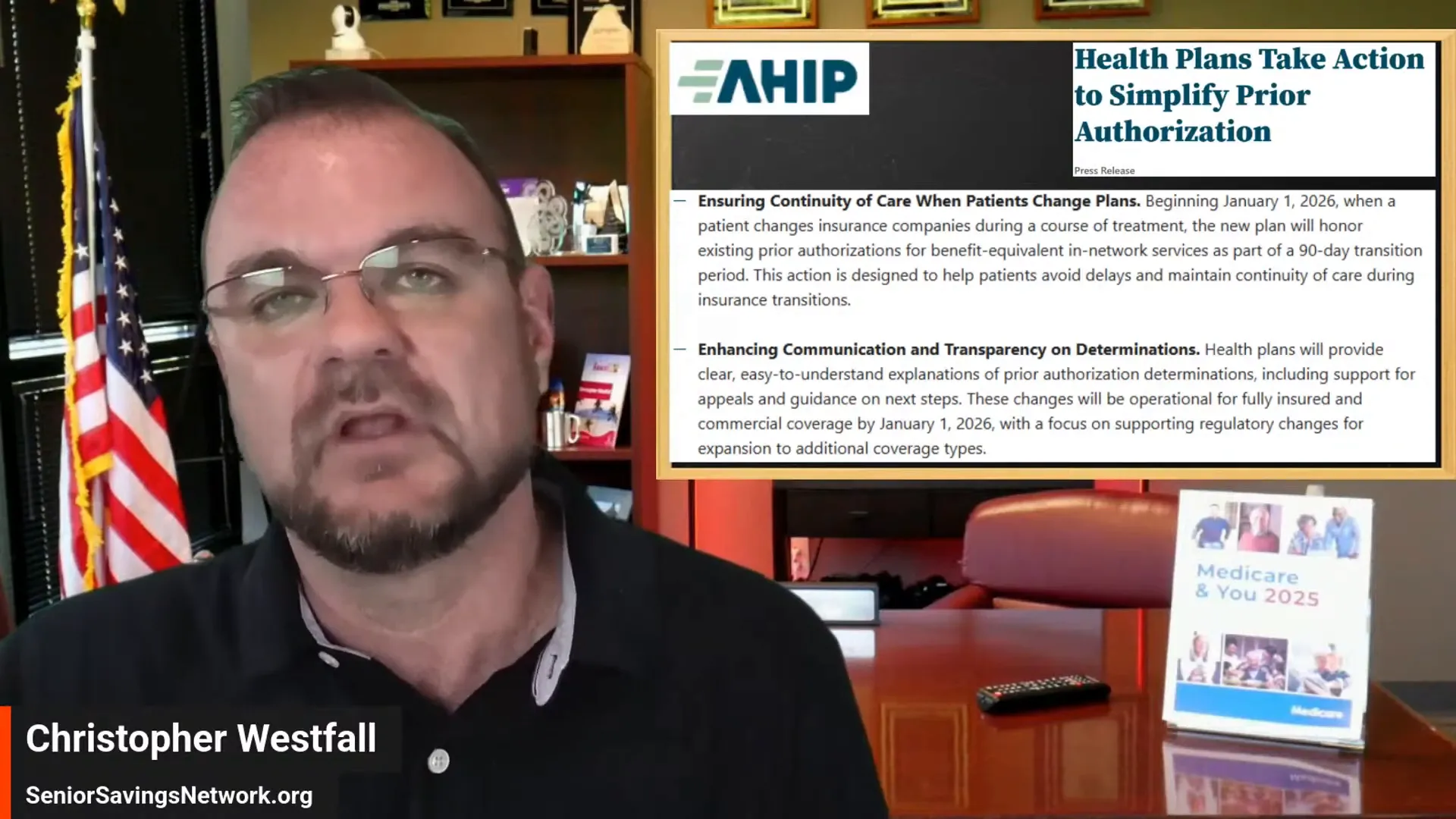

Just a month before the WISeR announcement, there was a major press conference in June 2025 where CMS Administrator Dr. Oz spoke out strongly against prior authorization in Medicare Advantage plans. He criticized the system as “the worst thing in the world,” acknowledging the widespread frustration it causes for both doctors and patients.

Dr. Oz highlighted how Medicare Advantage plans routinely deny care to save money, often at the expense of seniors’ health. He also took credit for bringing together about 50 insurance companies representing 75 million Americans to voluntarily reform prior authorization policies within Medicare Advantage and other private plans.

So, it was surprising to see just weeks later that CMS decided to extend a prior authorization scheme into Original Medicare, despite the public outcry and promises to reduce such bureaucratic hurdles.

The Scourge of Prior Authorization: Voices from Providers and Patients

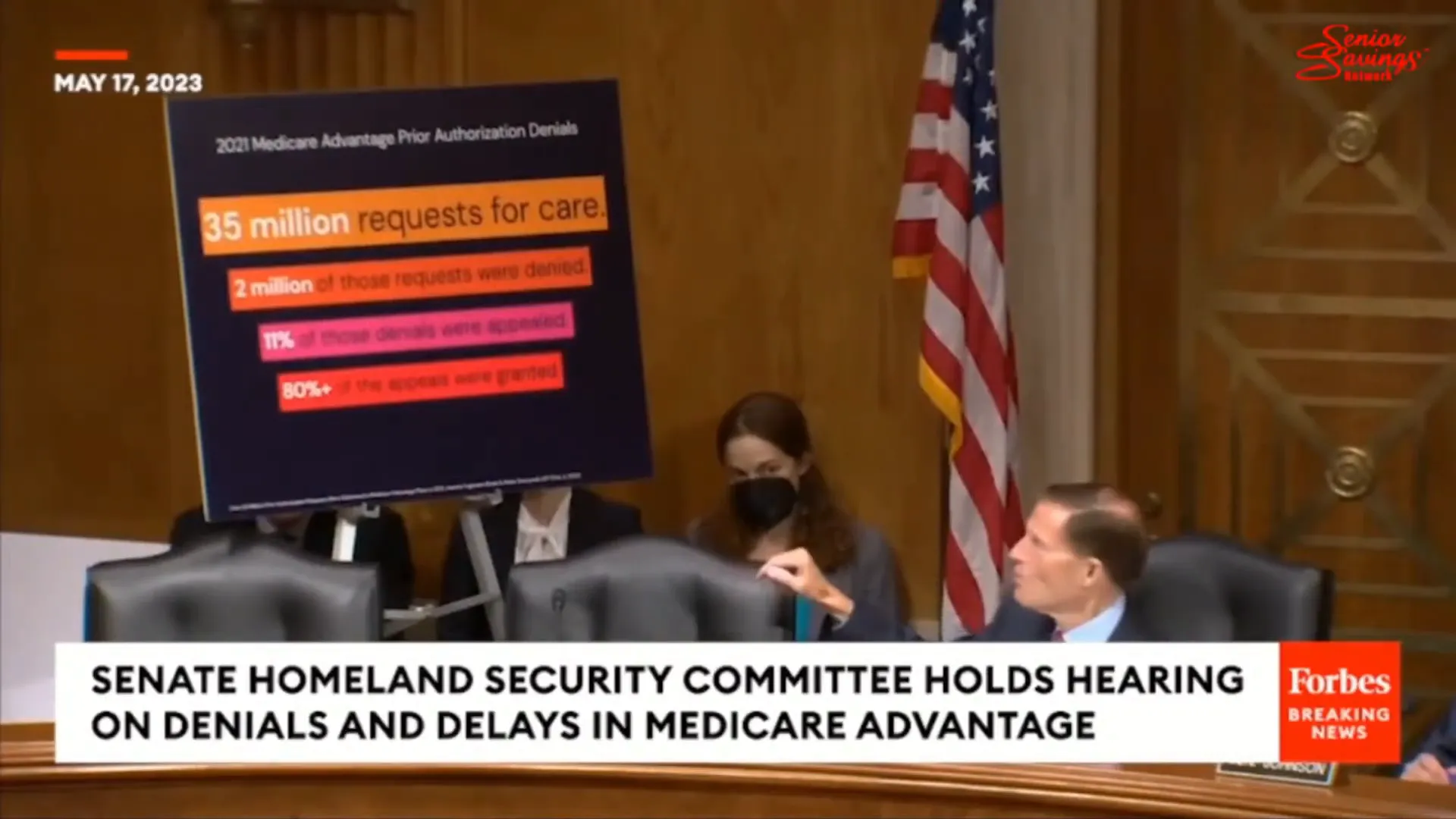

Many doctors describe prior authorization as a “bureaucratic nightmare” that places an opaque barrier between the patient and their trusted physician. Instead of a direct doctor-patient relationship, someone sitting in a cubicle with a checklist decides whether a treatment plan is approved or denied. This can lead to heartbreaking stories of patients being denied care that their doctors strongly recommend.

In Senate hearings and public forums, physicians have shared countless episodes where patients called back in tears because their insurance company refused to cover essential treatments. This system undermines trust and adds unnecessary stress during vulnerable times.

Despite these challenges, prior authorization has been largely confined to Medicare Advantage and other managed care plans. The new WISeR Model breaks with that tradition by embedding prior authorization directly into Original Medicare.

What Exactly Is the WISeR Model?

The WISeR Model stands for Wasteful and Inappropriate Service Reduction. It is a demonstration project designed to identify and reduce unnecessary or inappropriate services covered by Medicare. The program uses advanced technologies like artificial intelligence (AI) and machine learning to review claims and decide whether they should be approved or denied.

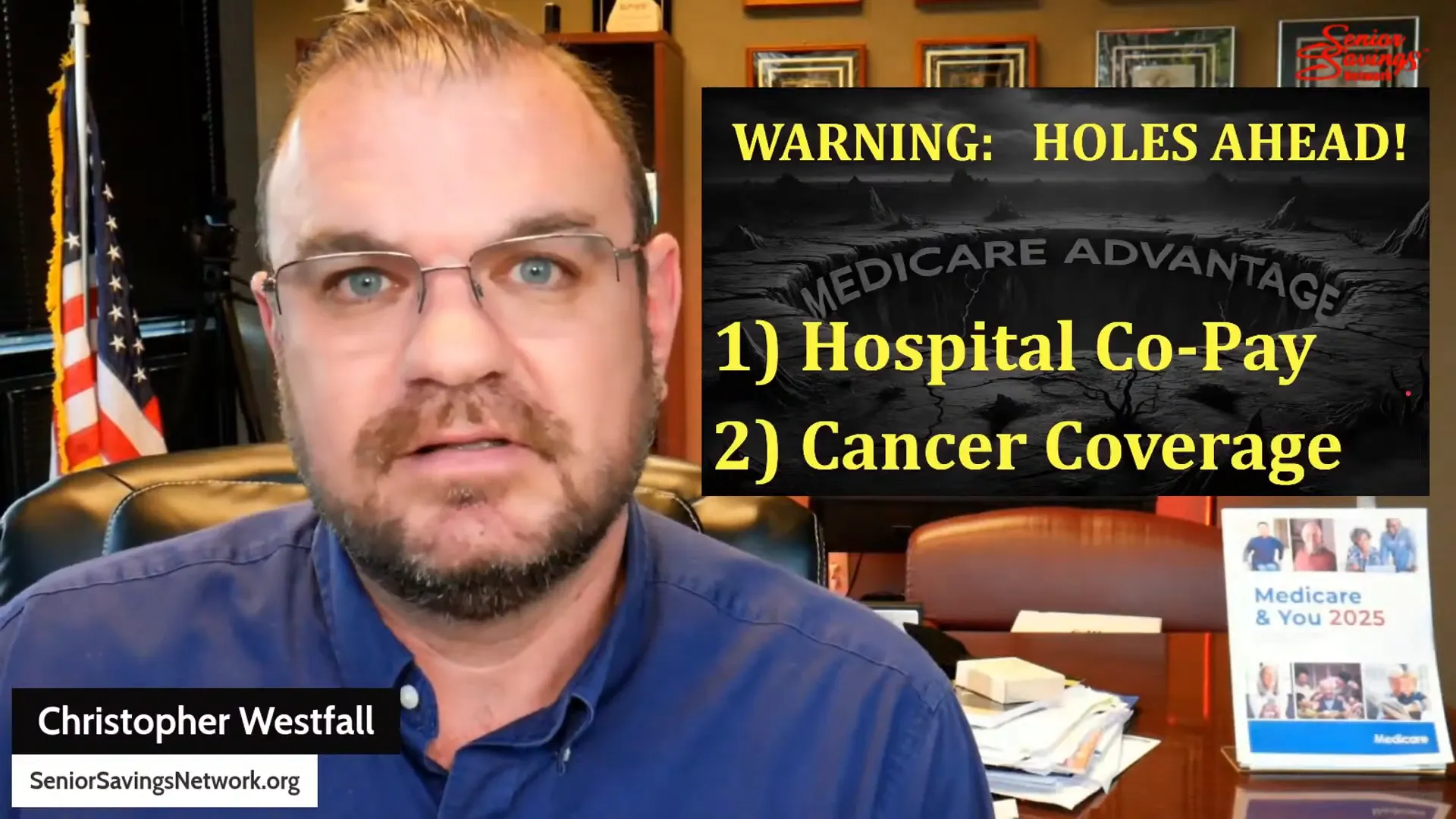

Initially, the WISeR Model will focus on 17 specific procedures and services, including knee replacements, spinal decompressions, steroid injections for pain, skin grafts, and more. These are not minor or random procedures—they are significant treatments that many seniors depend on for quality of life.

The program will operate in six states as a trial, with potential expansion nationwide depending on results and feedback.

Why These Six States and These Procedures?

The choice of Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington as pilot states seems to be a way to test the program in diverse healthcare markets. However, the targeted procedures raise questions. Despite the program’s stated goal of combating fraud and waste, none of these procedures have been historically linked to large-scale fraud schemes.

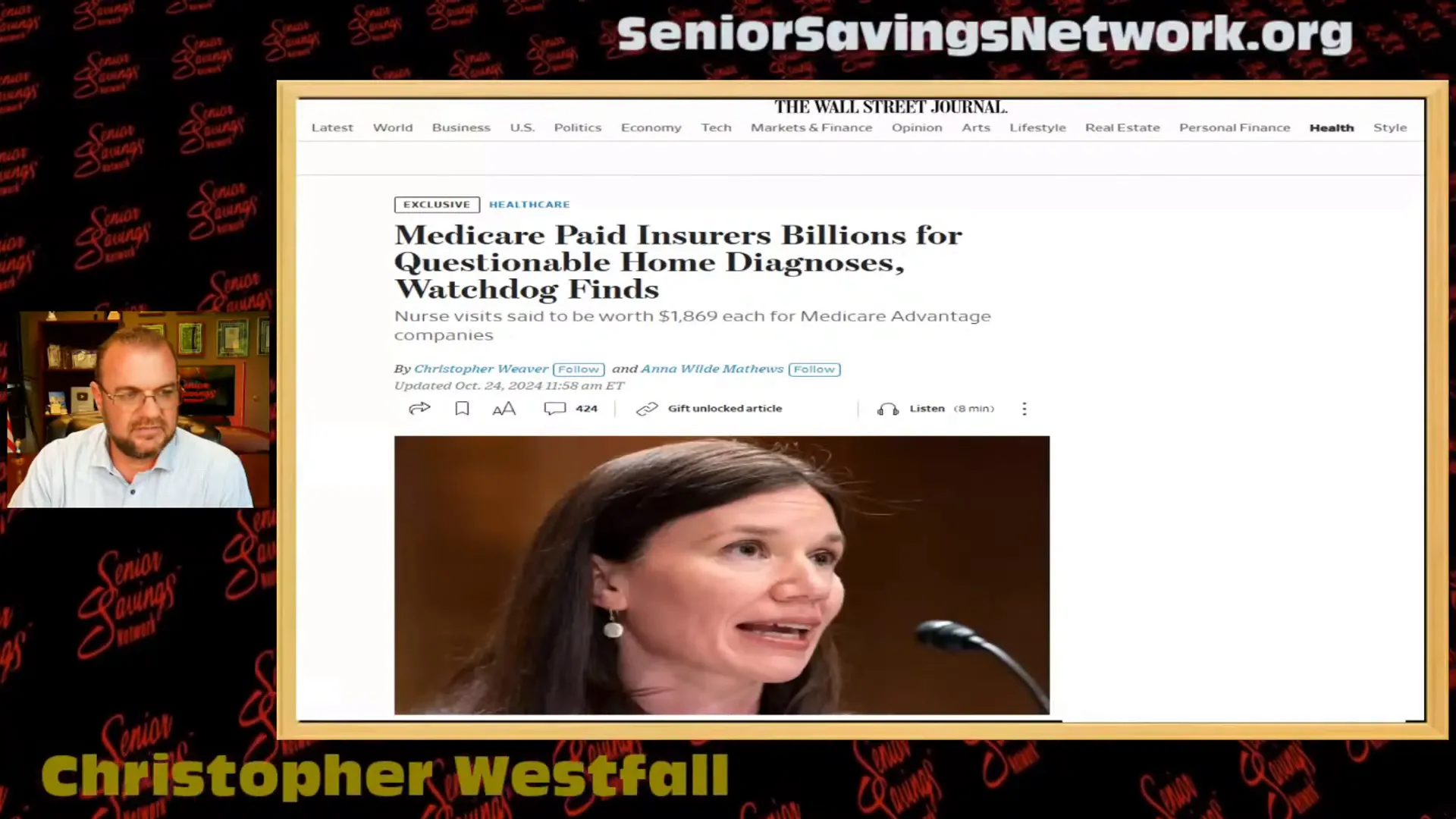

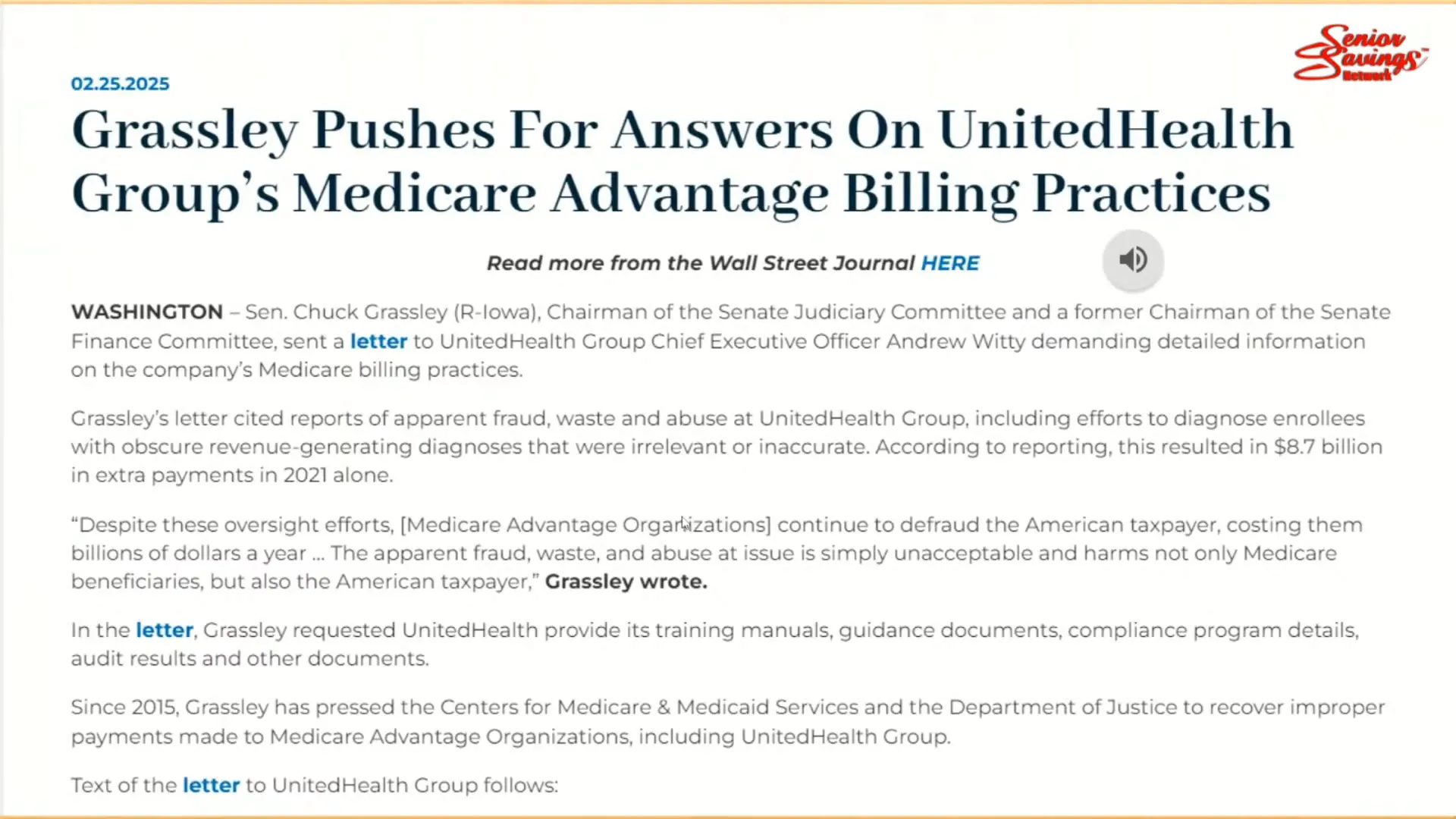

In contrast, the biggest Medicare fraud cases in recent years have centered around durable medical equipment (DME) such as wheelchairs, walkers, diabetic shoes, and catheters. For example, in 2025 alone, federal investigators uncovered a $10.6 billion fraud scheme involving fraudulent billing for medical supplies that seniors never received.

Yet, the WISeR Model doesn’t focus on these high-fraud areas. Instead, it targets treatments that patients truly need and that have not been associated with fraud, raising concerns about whether the model’s priorities are misplaced.

The True Incentives Behind WISeR: Payment Tied to Denials

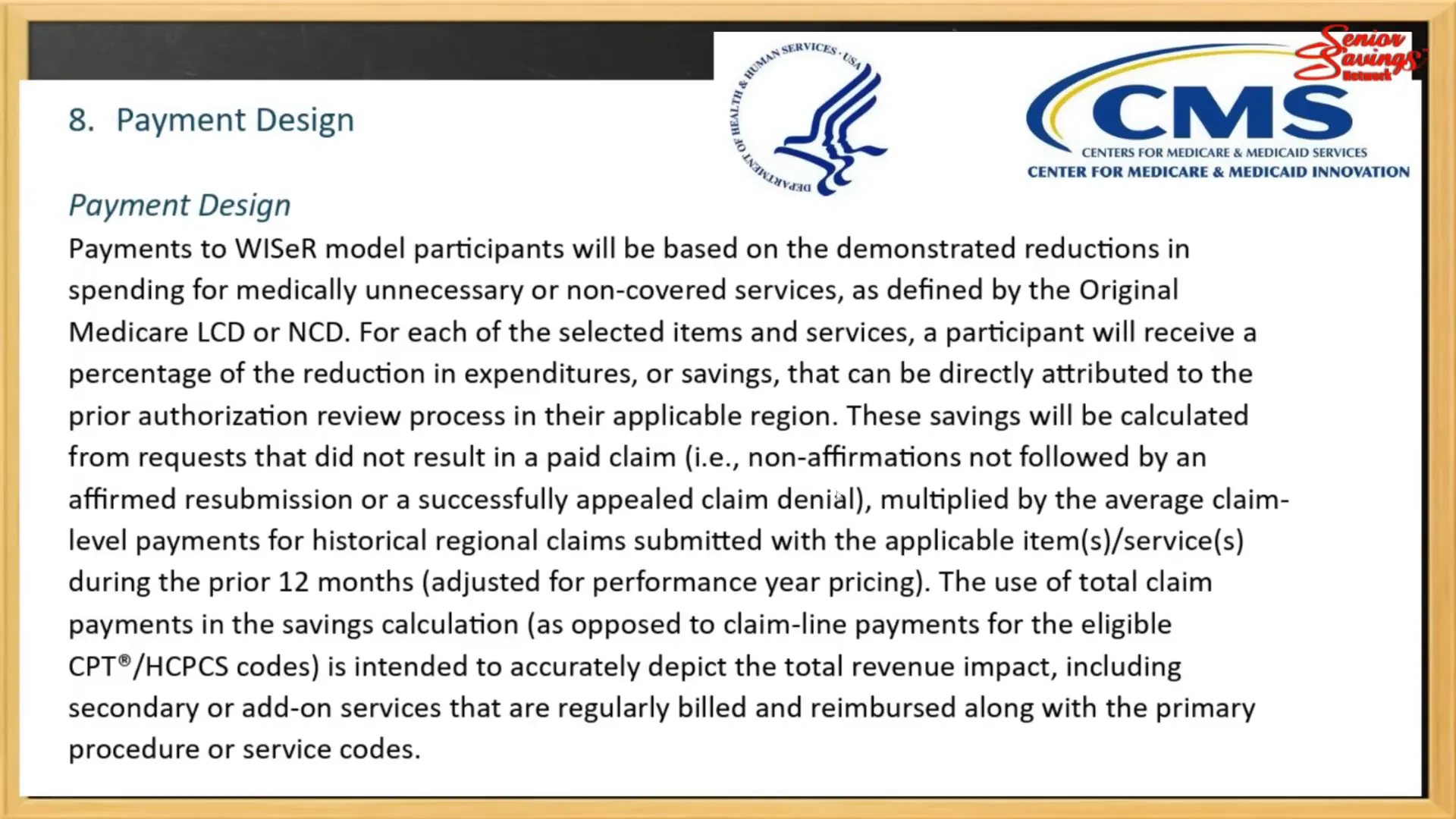

One of the most troubling aspects of the WISeR Model is how companies participating in the program get paid. CMS has made it clear that these companies will receive financial incentives based on the amount of money saved by denying claims—not simply for processing prior authorizations.

In other words, the more claims they deny, the more money they make. This creates a direct incentive to say “no” to care, rather than focusing on patient needs or clinical appropriateness.

This payment structure contrasts with a more neutral or patient-centered approach and could lead to widespread denials and delays for seniors trying to get necessary treatments. The underlying message is that saving money is the top priority, even if it means many seniors will have to jump through hoops or face care denials.

Free Medicare Insurance Help |

|

Reach out to the Senior Savings Network |

| Click Here |

Who Are the Companies Running WISeR?

The companies selected to operate the WISeR Model are expected to have expertise in managing prior authorization processes and to use advanced technologies like AI and machine learning. Interestingly, many of these companies are the same ones that currently manage Medicare Advantage prior authorizations—the very companies that have been criticized for routinely denying care to seniors.

This overlap raises concerns about whether lessons from Medicare Advantage’s prior authorization challenges will be applied to protect seniors in Original Medicare or if the same patterns of denial and delay will simply be extended.

How WISeR Could Impact Seniors

If the WISeR Model expands beyond its initial six-state pilot, it could affect up to four million seniors annually. These seniors may find their care suddenly halted as procedures are put “on hold” pending prior authorization reviews. This means delays in surgeries, treatments, injections, and other necessary services.

For seniors living with chronic pain or debilitating conditions, these delays can be devastating. Waiting for approvals, facing denials, and navigating appeals can cause unnecessary suffering and anxiety.

Moreover, if care is denied, patients and providers will be encouraged to discuss alternative, often cheaper, treatment options. This may not always align with the best clinical care or what the patient truly needs.

Medicare Advantage vs. Original Medicare: A Growing Divide

Medicare Advantage plans have long used prior authorization as a cost-control tool. Beneficiaries of these plans typically receive about 9.2% fewer services overall compared to those on Original Medicare, according to CMS data. The rationale is that Medicare Advantage plans actively manage utilization to reduce “low-value” services and cut costs.

Now, with the WISeR Model, Original Medicare is adopting some of these same utilization management strategies, including prior authorization and prepayment reviews, but with the added twist of financial incentives tied to denials.

This shift may signal a future where the differences between Original Medicare and Medicare Advantage blur, but it also risks turning traditional Medicare into a more bureaucratic program with more hurdles for seniors to access care.

What You Can Do to Protect Yourself

As these changes unfold, it’s important for Medicare beneficiaries and their families to stay informed and proactive. Here are some steps to consider:

- Understand your coverage: Know whether you have Original Medicare or a Medicare Advantage plan, and how prior authorization works in your plan.

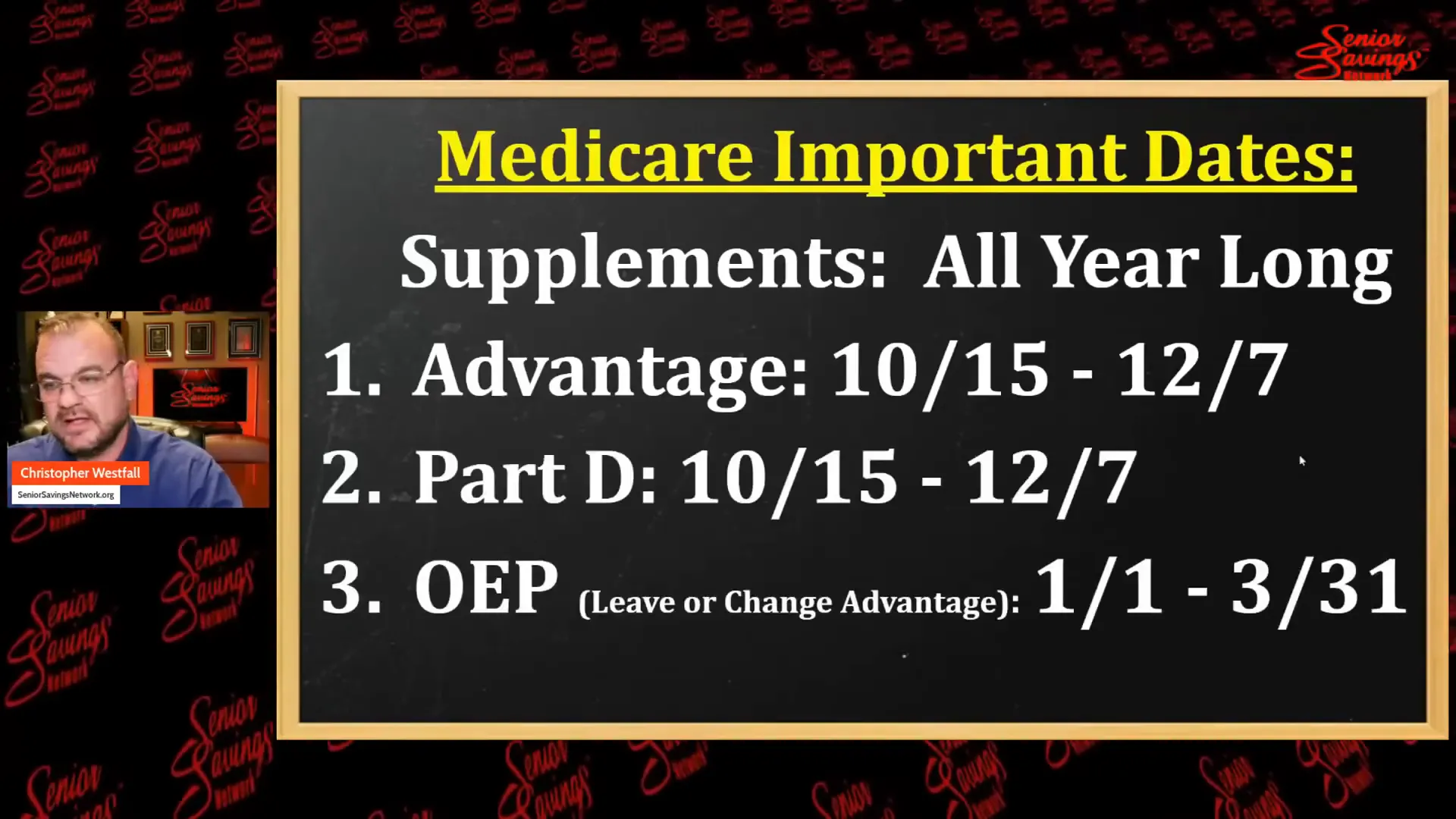

- Watch for state-specific changes: If you live in Arizona, New Jersey, Ohio, Oklahoma, Texas, or Washington, be especially vigilant about new prior authorization requirements starting in 2026.

- Advocate for your care: Work closely with your doctors to ensure they submit all necessary documentation for prior authorizations and appeals.

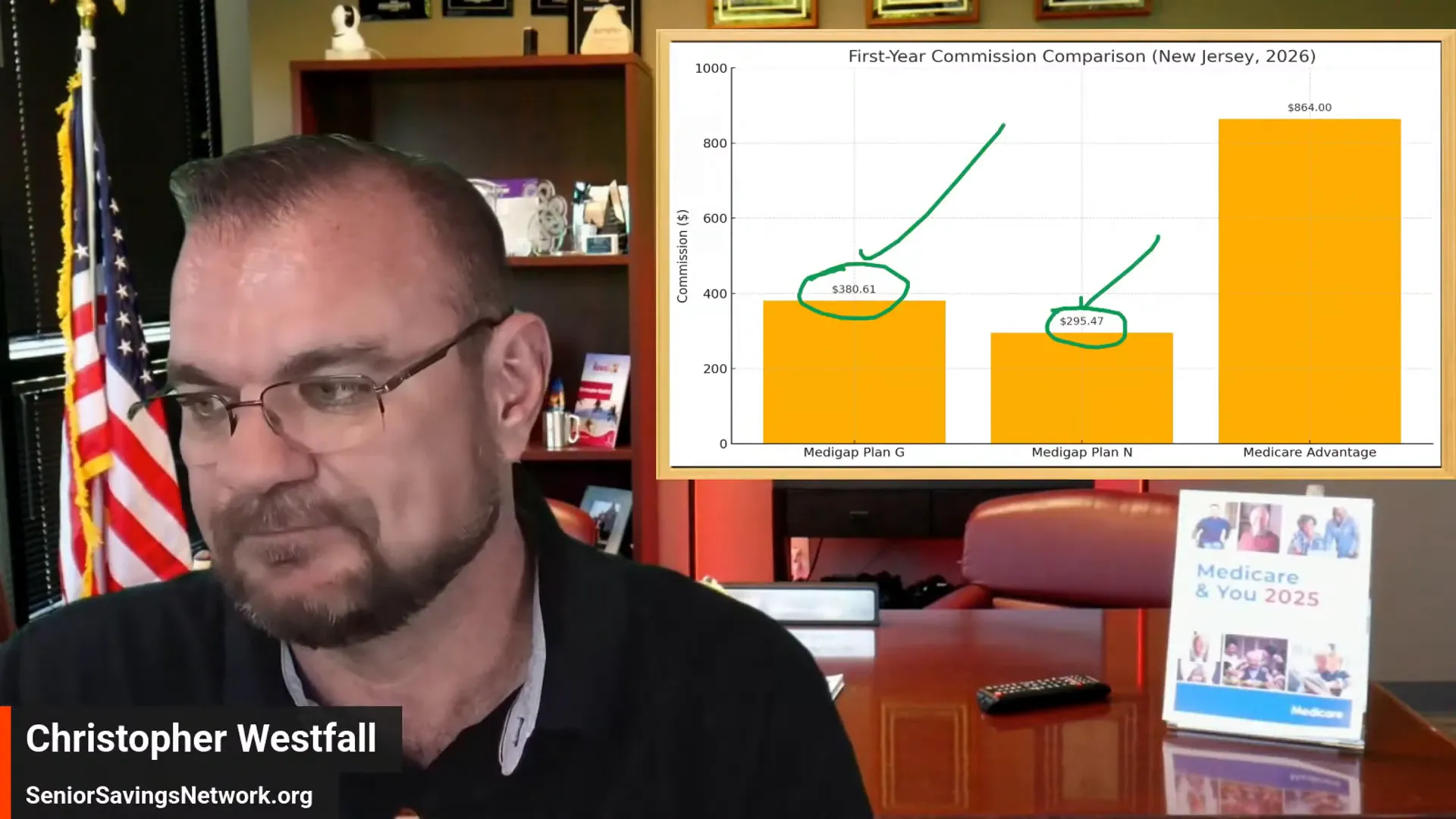

- Consider your insurance options: If you have a Medicare supplement (Medigap) plan, remember that you can change it year-round. Shopping around may save you money and improve your coverage.

- Stay connected with resources: Organizations like the Senior Savings Network can help you navigate these changes and find the best Medicare options for your needs.

Frequently Asked Questions (FAQs)

What is prior authorization in Medicare?

Prior authorization is a process where Medicare or your insurance plan requires approval before covering certain medical services or procedures. It’s meant to prevent unnecessary or costly care but can cause delays and denials.

Why is prior authorization being introduced in Original Medicare?

CMS aims to reduce wasteful or inappropriate spending in Medicare by introducing prior authorization through the WISeR Model. The program targets specific procedures and uses technology to review claims before payment.

Which states will be affected first?

The WISeR Model pilot will initially affect Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington starting in 2026.

What types of procedures will require prior authorization under WISeR?

The program focuses on 17 procedures, including knee replacements, spinal decompressions, steroid injections, skin grafts, and nerve stimulation therapies.

How will this affect my care?

Some seniors may experience delays or denials of coverage for certain procedures, requiring additional paperwork, appeals, or alternative treatment plans.

Are the companies running WISeR paid based on how many claims they deny?

Yes. Participating companies receive financial incentives based on the amount of money saved by denying claims, which raises concerns about potential over-denial of care.

What can I do if my care is denied?

You can work with your healthcare provider to appeal the denial. It’s important to keep detailed records and seek assistance from Medicare advocates or counselors if needed.

Conclusion: Stay Informed and Advocate for Your Care

The introduction of prior authorization into Original Medicare through the WISeR Model marks a significant shift in how Medicare manages healthcare services. While the goal of reducing waste and fraud is important, the system’s current incentive structure to deny care raises red flags for seniors and their families.

Delays and denials can hurt vulnerable patients, and the expansion of prior authorization beyond Medicare Advantage threatens to add bureaucratic hurdles to a program that has traditionally been more straightforward and accessible.

As these changes take shape, staying informed and proactive is key. Understand your coverage, communicate closely with your healthcare providers, and don’t hesitate to seek help if you encounter obstacles. Your health and well-being depend on it.

If you’re concerned about rising costs or potential changes to your Medicare supplement plan, now is a good time to review your options and shop for better coverage. The Senior Savings Network and other resources are here to help you navigate these complex waters.

Remember, the best way to protect yourself is by staying educated and engaged. Medicare is evolving, and with the right information, you can make the choices that keep you healthy and secure.

Thank you for reading. Please share this article with anyone you know who is on Medicare, especially if they live in the states affected by the WISeR Model. Together, we can face these challenges head-on.

Medicare’s New Prior Authorization Scheme: What You Need to Know Read More »