Murder and Fraud in Medicare Advantage

The Dark Side of Medicare Advantage: Unpacking the Controversies

In the ongoing debate surrounding Medicare Advantage, many are left questioning the true implications of this healthcare model. This blog delves into the complexities of Medicare Advantage, exploring its advantages and drawbacks, particularly in light of recent events and expert testimonies.

Table of Contents

- 🩺 Introduction: Addressing the Medicare Advantage Debate

- 🏥 Background on the United Healthcare CEO Incident

- 📋 Overview of Medicare Options: Original Medicare vs. Medicare Advantage

- 💻 Online Reactions and Industry Criticism

- 👩⚕️ Doctors’ Perspective: Real-World Consequences of Denied Care

- 📊 Senate Findings on Medicare Advantage Denials

- 📈 Data Manipulation and Financial Incentives in Medicare Advantage

- 🏥 The Role of Insurers in Shaping Healthcare Decisions

- 🧩 Addressing Medicare Advantage Misconceptions

- 📅 Key Enrollment Periods and Transition Advice

- 🛡️ Appeals Process for Denied Care: Insights and Strategies

- 🏥 Differences Between Medicare Supplement and Medicare Advantage

- 🚧 Challenges with Medicare Advantage Coverage

- 🗺️ Navigating Medicare Choices

- 📚 Importance of Staying Informed

- ❓ FAQ: Common Questions About Medicare Advantage

🩺 Introduction: Addressing the Medicare Advantage Debate

The Medicare Advantage debate has become increasingly intense, especially in light of recent events. Many people are left wondering about the implications of this healthcare model. With millions of seniors relying on it, understanding the advantages and drawbacks of Medicare Advantage is crucial. The discussions around this topic often highlight the need for transparency and education in the healthcare system.

Why the Debate Matters

As more seniors enter the Medicare system, the choice between Original Medicare and Medicare Advantage becomes critical. Many insurance agents promote Medicare Advantage plans, often because they are financially incentivized to do so. This raises questions about whether seniors are receiving the best advice for their health needs.

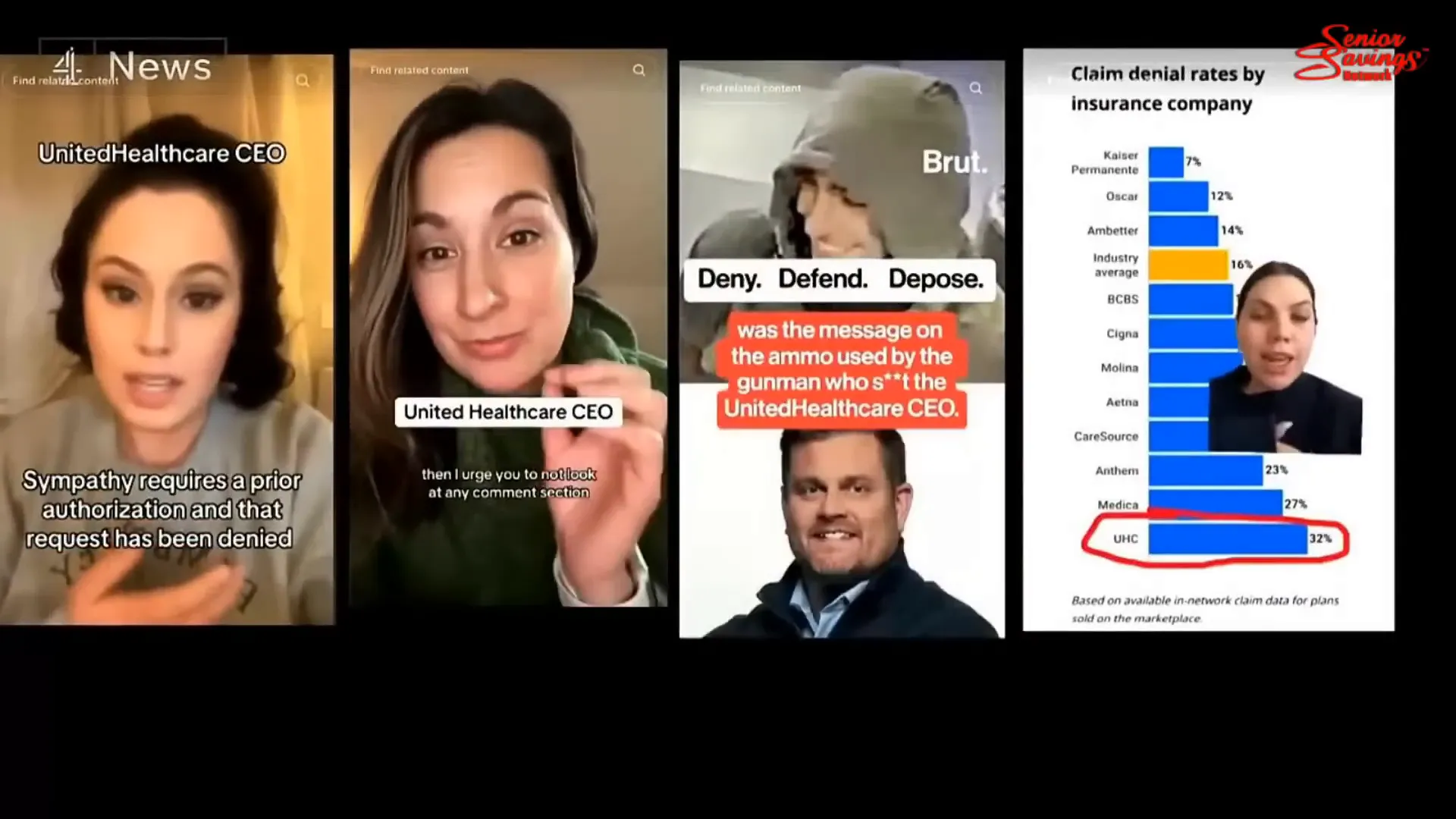

🏥 Background on the United Healthcare CEO Incident

The recent incident involving the CEO of United Healthcare has sparked outrage and debate across social media platforms. What happened? The CEO was tragically murdered, leading to a wave of online reactions that underscored the frustrations many have with healthcare insurance practices.

Public Reaction

Online discussions have been rife with mixed feelings. Some expressed a lack of sympathy, citing the struggles many face when dealing with insurance companies. Comments such as, “sympathy requires a prior authorization,” highlight the frustrations that have built up over years of dealing with denied claims and bureaucratic hurdles.

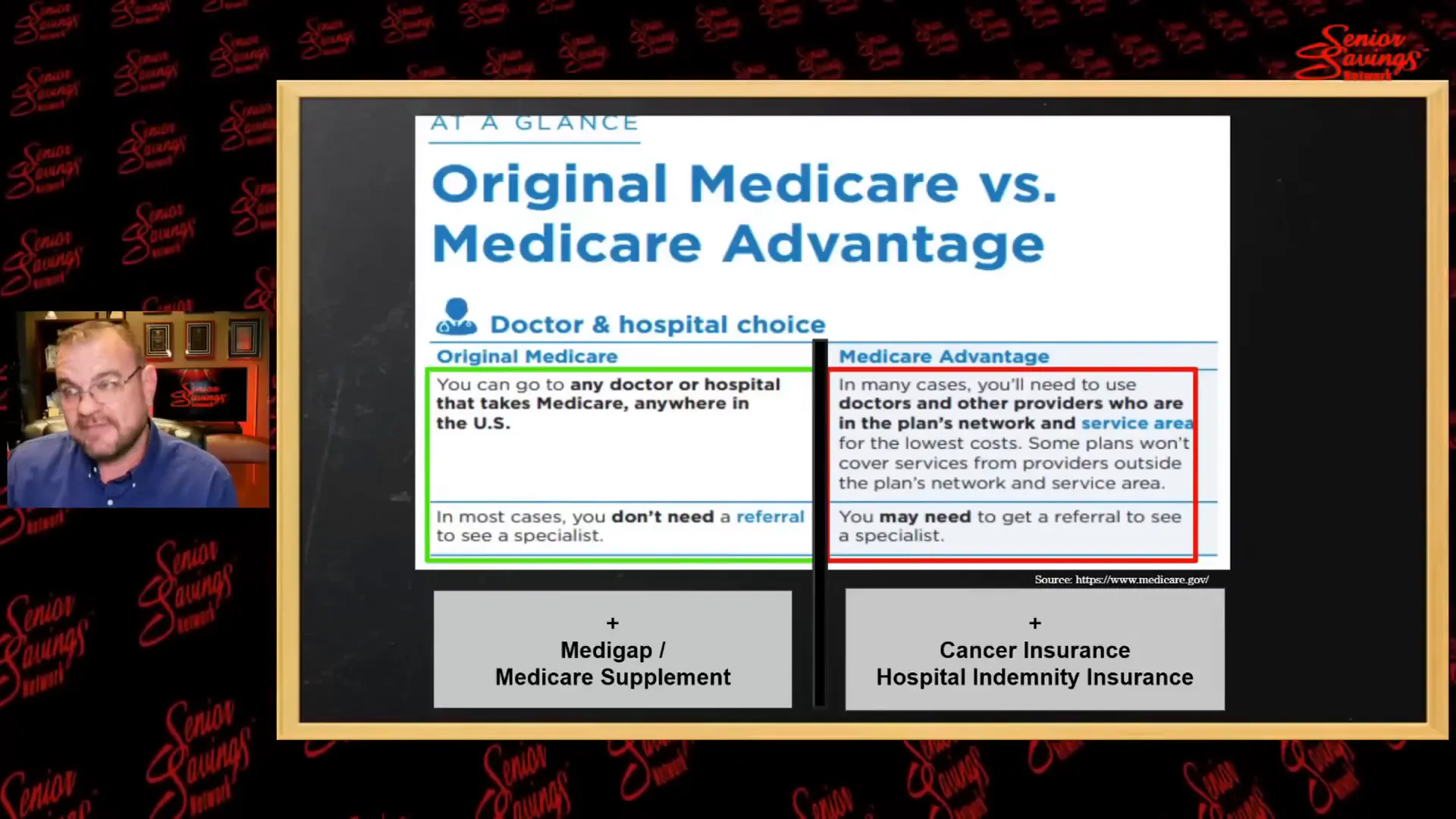

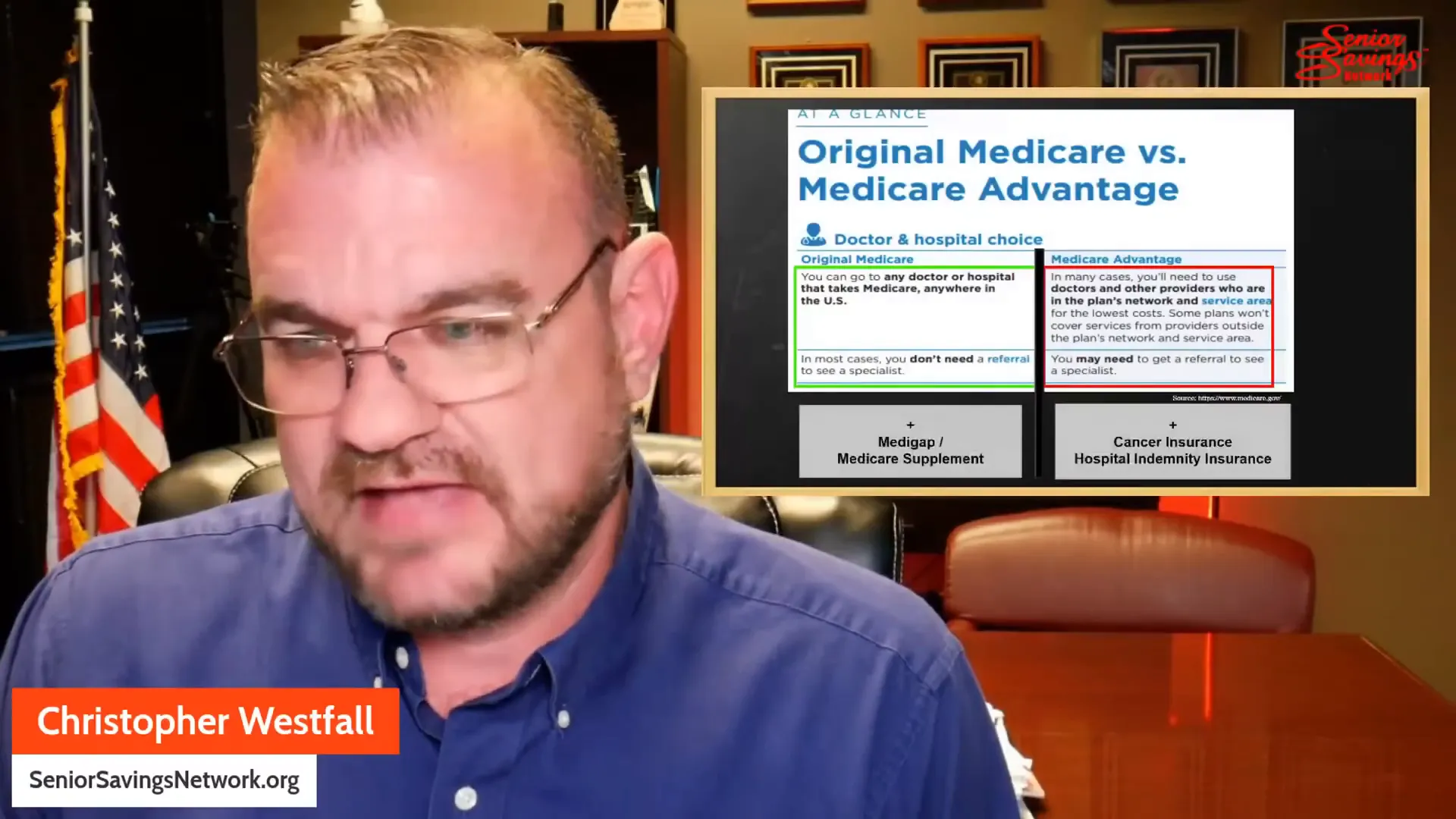

📋 Overview of Medicare Options: Original Medicare vs. Medicare Advantage

Understanding the differences between Original Medicare and Medicare Advantage is vital for making informed decisions. Both options have their pros and cons, and it’s essential to know how they affect your healthcare experience.

Original Medicare

- Comprises Part A (Hospital Insurance) and Part B (Medical Insurance).

- Generally, no prior authorization is required for medically necessary services.

- Allows patients to see any doctor or specialist without network restrictions.

Medicare Advantage

- These plans are offered by private insurance companies and include both Part A and Part B coverage.

- Often require prior authorization for services, which can delay care.

- May come with additional benefits but often have network restrictions and higher out-of-pocket costs for specific services.

💻 Online Reactions and Industry Criticism

The online discourse surrounding the United Healthcare incident reflects broader concerns about the healthcare industry. Many critics point to the insurance model as detrimental to patient care, citing the rising number of denied claims as evidence of systemic issues.

Industry Criticism

Critics argue that insurance companies prioritize profits over patient care. The phrase “deny, depose, defend,” found on bullet casings related to the incident, has become a rallying cry for those frustrated with the system. This sentiment is echoed by many healthcare professionals who feel undermined by insurance policies that dictate patient care.

👩⚕️ Doctors’ Perspective: Real-World Consequences of Denied Care

Healthcare professionals have been vocal about the real-world impacts of Medicare Advantage. Denied care can have dire consequences for patients, leading to delays in necessary treatments and worsening health outcomes.

Case Studies

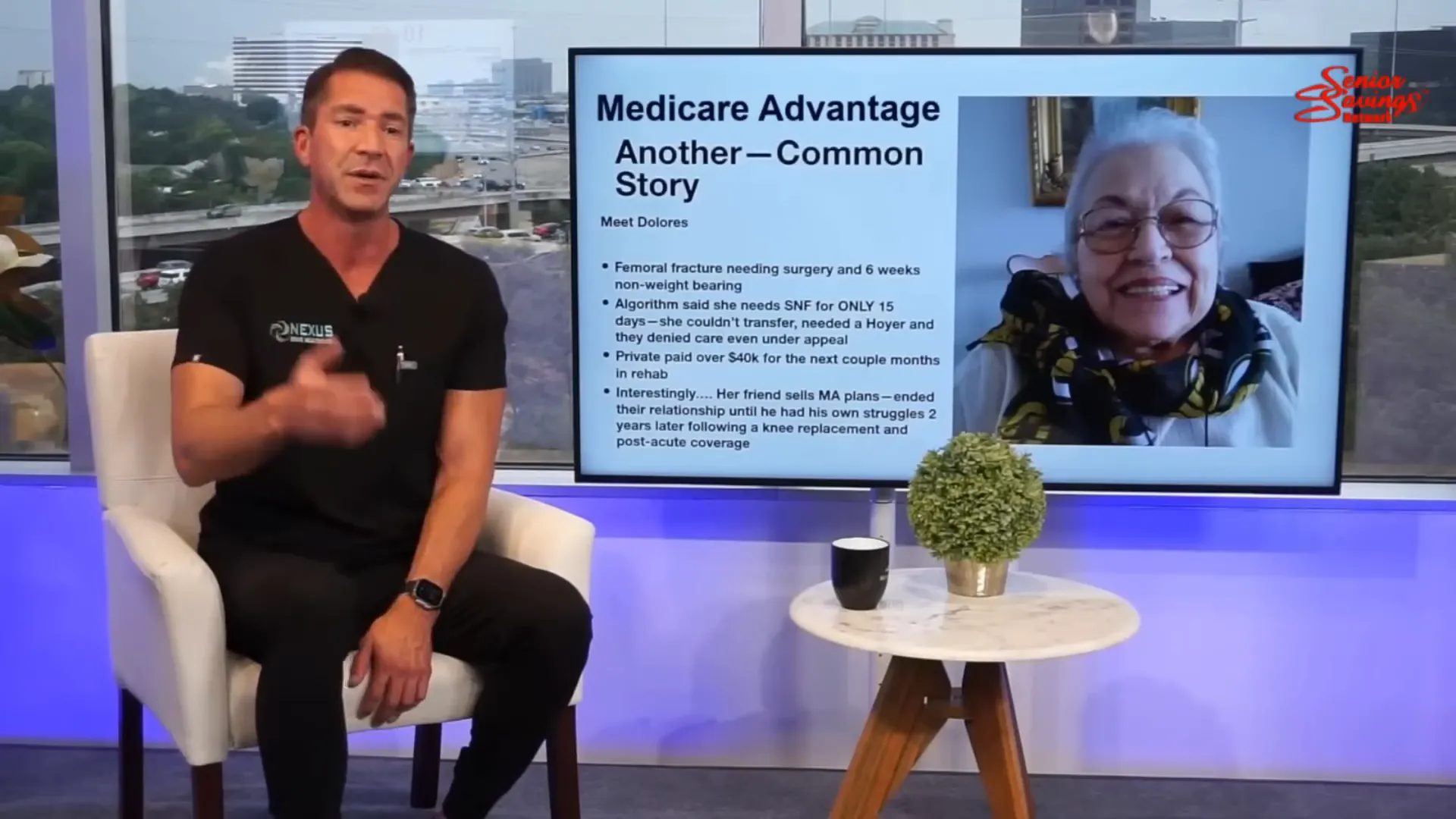

One stark example involves a patient with a history of breast cancer. After experiencing chest pain, a CT scan was deemed necessary. However, the insurance company denied the request for the test, resulting in a delay that ultimately led to the patient’s death. This is not an isolated case; many doctors share similar stories of denied care resulting in tragic outcomes.

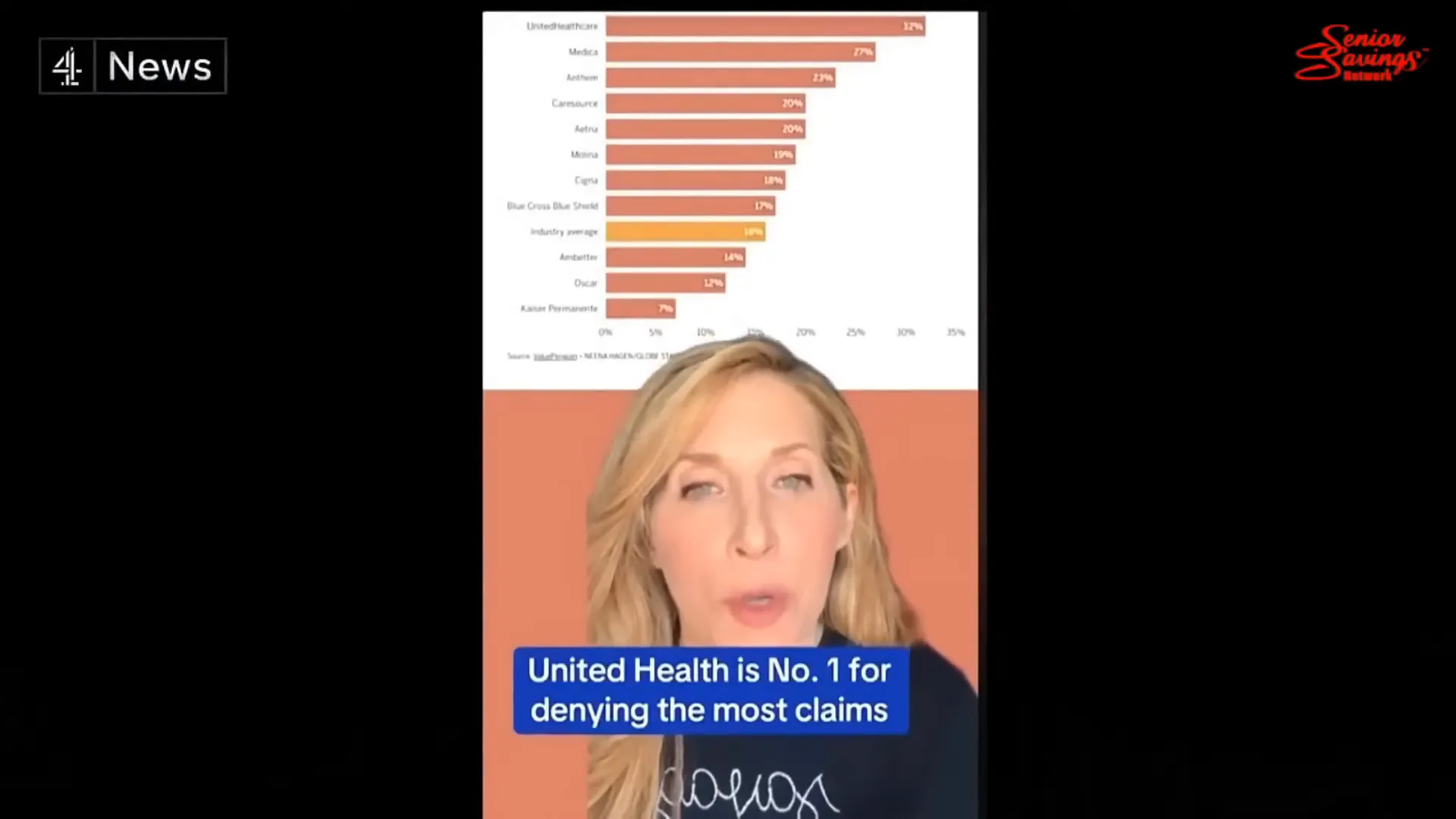

📊 Senate Findings on Medicare Advantage Denials

Recent Senate findings have shed light on the denial rates associated with Medicare Advantage plans. The data reveals alarming trends that raise concerns about the efficacy of these plans in providing care.

Key Findings

- Medicare Advantage insurers denied approximately 7% of prior authorization requests.

- Denial rates were significantly higher for post-operative care and rehabilitation services.

- These practices have led to increased scrutiny from lawmakers and healthcare advocates.

📈 Data Manipulation and Financial Incentives in Medicare Advantage

Understanding the financial dynamics behind Medicare Advantage is essential for beneficiaries. The structure of these plans often leads to data manipulation, where insurers may prioritize profits over patient care.

Insurance companies operate on a profit model. This means that they are incentivized to deny care to cut costs. A report highlighted that in 2023, United Health alone raked in $22 billion in profits. This profit margin raises concerns about the priorities of these companies.

Financial Incentives at Play

- Prior Authorization Requirements: Insurers often require prior authorization for many services. This can result in delays and denials of necessary care, impacting patient health.

- Risk Adjustment Payments: Insurers receive higher payments for patients with more complex health needs. This can lead to practices where insurers manipulate data to appear as though they have fewer high-risk patients.

- Plan Changes: Companies can alter their plans annually, often resulting in higher out-of-pocket costs for patients. This unpredictability can leave beneficiaries scrambling for care.

These tactics can create a challenging landscape for seniors, where navigating their healthcare becomes a daunting task. Understanding these financial incentives is crucial for making informed decisions regarding Medicare Advantage plans.

🏥 The Role of Insurers in Shaping Healthcare Decisions

Insurers play a significant role in shaping healthcare decisions for beneficiaries. With Medicare Advantage, the control exerted by these companies can limit patient options and dictate the course of care.

Insurers often dictate which services are covered and how much patients must pay out-of-pocket. This can lead to situations where necessary treatments are denied based on cost rather than medical necessity.

How Insurers Influence Care

- Provider Networks: Many Medicare Advantage plans have limited provider networks. This means patients may not have access to their preferred doctors or specialists.

- Restrictions on Services: Insurers can impose restrictions on certain services, making it difficult for patients to receive the care they need.

- Cost-Sharing Structures: High deductibles and copayments can deter patients from seeking necessary care due to cost concerns.

This dynamic highlights the need for beneficiaries to be well-informed about their plans and to advocate for their healthcare needs actively.

🧩 Addressing Medicare Advantage Misconceptions

Many misconceptions surround Medicare Advantage, leading to confusion for beneficiaries. Understanding the realities of these plans is essential for making informed choices.

One common misconception is that Medicare Advantage is the same as Original Medicare. While both provide coverage, the structures and limitations can differ significantly.

Common Misunderstandings

- All Plans Are the Same: Not all Medicare Advantage plans offer the same coverage. Each plan can have different networks, costs, and benefits.

- Lower Costs Mean Better Care: While some Medicare Advantage plans may have lower premiums, they can come with higher out-of-pocket costs and more restrictions.

- Guaranteed Coverage: Unlike Medicare Supplement plans, Medicare Advantage plans can change yearly, potentially impacting coverage and costs.

Clearing up these misconceptions can empower beneficiaries to make better healthcare decisions and choose plans that align with their needs.

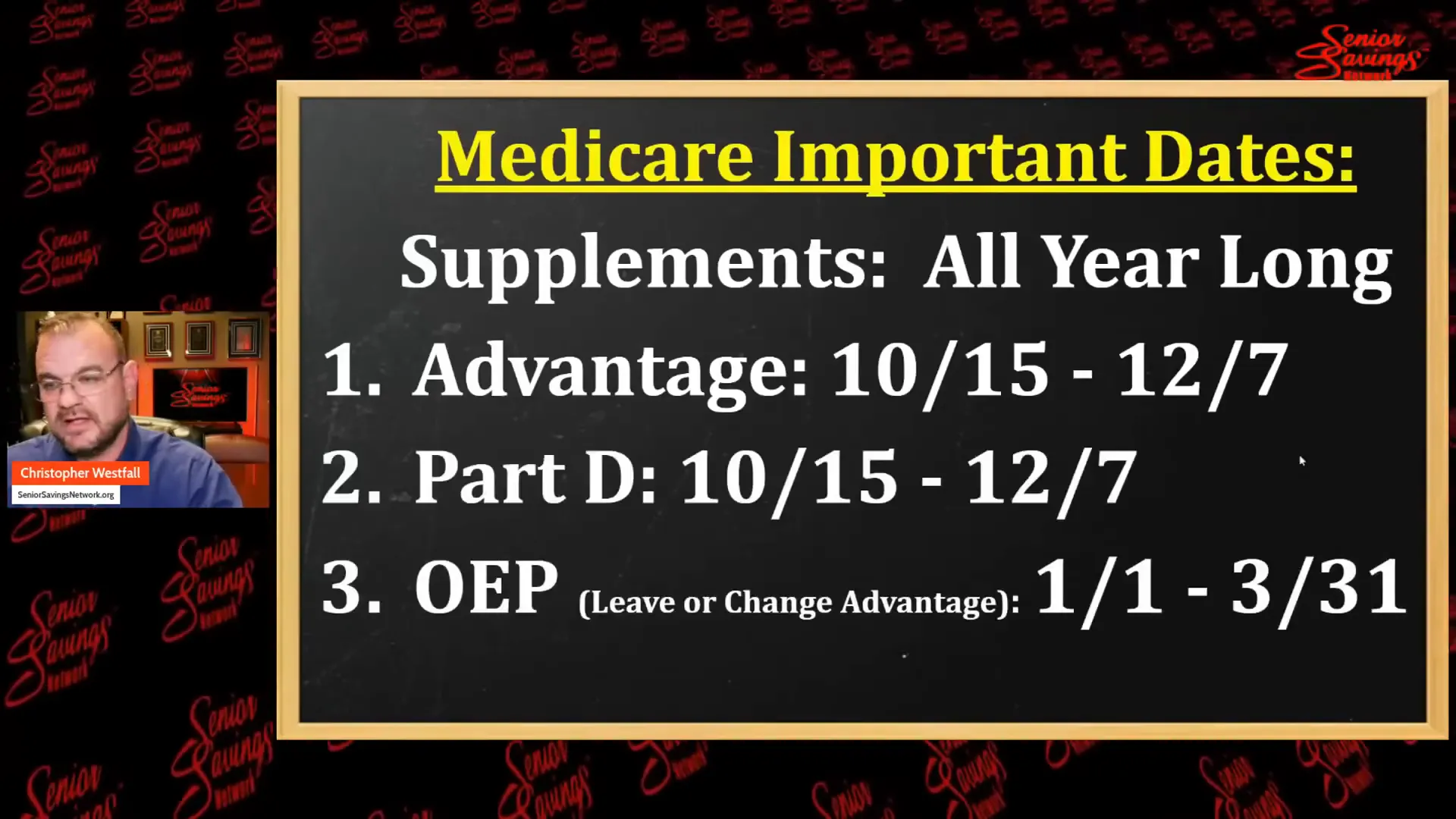

📅 Key Enrollment Periods and Transition Advice

Being aware of key enrollment periods is vital for anyone considering Medicare Advantage. These periods dictate when beneficiaries can enroll, switch plans, or return to Original Medicare.

The annual enrollment period runs from October 15th to December 7th. During this time, beneficiaries can review their options and make necessary changes to their plans.

Important Enrollment Dates

- Annual Enrollment Period: October 15 – December 7

- Open Enrollment Period: January 1 – March 31 (for switching from Medicare Advantage to Original Medicare)

- Special Enrollment Periods: Available for certain life events, such as moving or losing other coverage.

Beneficiaries should take the time to understand their options during these periods, ensuring they select the best plan for their healthcare needs.

🛡️ Appeals Process for Denied Care: Insights and Strategies

The appeals process for denied care can be overwhelming, but knowing how to navigate it can increase the chances of a successful outcome. Many beneficiaries are unaware of their rights when it comes to appealing denials.

Studies show that over 75% of appeals are successful if pursued correctly. This highlights the importance of advocating for oneself in the face of denial.

Steps to Take When Facing a Denial

- Understand Your Rights: Familiarize yourself with your rights under Medicare. You have the right to appeal any denial.

- Gather Documentation: Collect all relevant medical records and documentation to support your case.

- Involve Your Doctor: Having your doctor involved can strengthen your appeal, as they can provide necessary medical justification for the requested care.

These steps can empower beneficiaries to challenge denials effectively, ensuring they receive the care they have paid for and deserve.

🏥 Differences Between Medicare Supplement and Medicare Advantage

Understanding the differences between Medicare Supplement (Medigap) and Medicare Advantage is crucial for beneficiaries. Each option has its own set of benefits and limitations.

Medicare Supplement plans are designed to cover gaps in Original Medicare, while Medicare Advantage plans are an alternative way to receive Medicare benefits through private insurance companies.

Key Differences

- Provider Flexibility: Medicare Supplement plans typically allow beneficiaries to see any doctor that accepts Medicare, while Medicare Advantage plans may have network restrictions.

- Cost Structure: Medicare Supplement plans often have higher premiums but lower out-of-pocket costs, whereas Medicare Advantage may have lower premiums with higher out-of-pocket expenses.

- Plan Stability: Medicare Supplement plans offer stable coverage that doesn’t change yearly, while Medicare Advantage plans can change benefits and costs annually.

Being informed about these differences can help beneficiaries make better decisions about their healthcare options and choose the plan that best fits their needs.

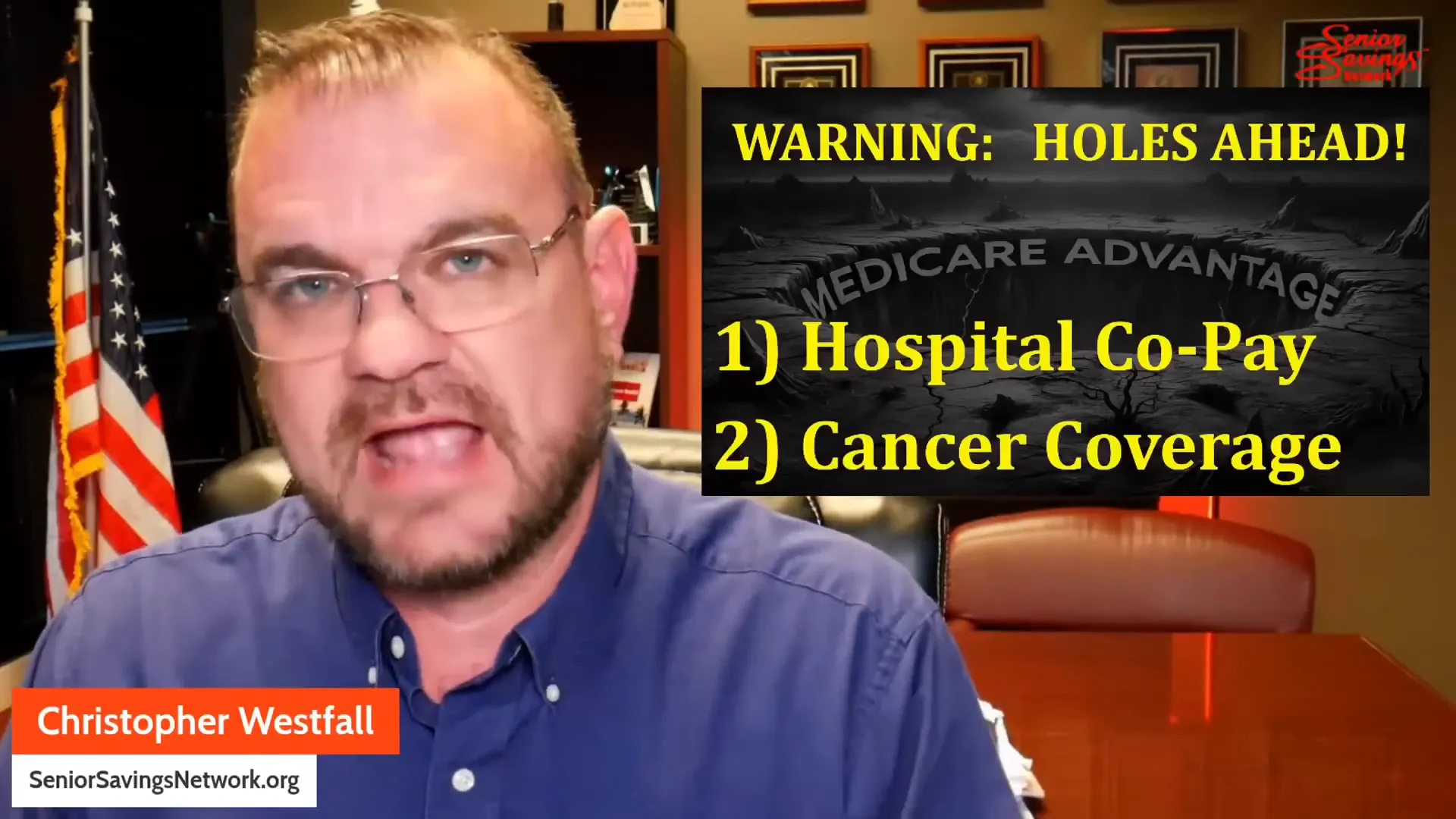

🚧 Challenges with Medicare Advantage Coverage

Navigating Medicare Advantage can be tricky, especially for seniors who depend on these plans for their healthcare needs. While there are many benefits to Medicare Advantage, there are also significant challenges that can impact the quality of care beneficiaries receive.

One major challenge is the prior authorization requirement. Many Medicare Advantage plans require patients to get approval before receiving certain treatments or tests. This can lead to delays in care, which can be detrimental, especially for those with urgent health issues.

Common Challenges Faced by Beneficiaries

- Network Restrictions: Unlike Original Medicare, which allows you to see any doctor who accepts Medicare, many Medicare Advantage plans have limited networks. This can restrict your choices and may require you to switch doctors.

- Higher Out-of-Pocket Costs: While some plans advertise low premiums, they can come with high deductibles and copayments. This can catch beneficiaries off guard when they need care.

- Complex Plan Structures: Each Medicare Advantage plan can differ significantly in terms of coverage, costs, and benefits. This complexity can make it hard for seniors to understand what their plan covers.

🗺️ Navigating Medicare Choices

Choosing the right Medicare plan can feel overwhelming. With so many options available, it’s essential to take the time to explore and understand what each plan offers.

When considering Medicare Advantage, it’s important to evaluate your healthcare needs. Are you managing chronic conditions? Do you have preferred doctors? These questions can guide your decision-making process.

Steps for Making an Informed Choice

- Research Available Plans: Use resources like Medicare Advantage Near Me to find plans available in your area.

- Compare Plan Details: Look at the benefits, costs, and provider networks of each plan. Make sure the plan fits your healthcare needs.

- Seek Assistance: Don’t hesitate to reach out to local health insurance counselors or use official resources like Joining a plan | Medicare for guidance.

📚 Importance of Staying Informed

Staying informed about Medicare Advantage is crucial for beneficiaries. Changes in plans, coverage, and regulations can happen frequently, which can affect your healthcare options.

Being proactive about understanding your plan can help you avoid unexpected expenses and ensure that you receive the care you need. Regularly reviewing your plan during the annual enrollment period is a good practice.

Tips for Staying Updated

- Follow Medicare News: Subscribe to newsletters or follow Medicare-related websites for updates on changes that may affect your coverage.

- Engage with Your Plan: Attend meetings or webinars offered by your Medicare Advantage provider to stay informed about your plan’s benefits and changes.

- Connect with Peers: Joining local support groups or online forums can provide valuable insights and experiences from others navigating Medicare.

❓ FAQ: Common Questions About Medicare Advantage

Many beneficiaries have questions about Medicare Advantage, and it’s important to address these to alleviate confusion and empower decision-making.

Frequently Asked Questions

- What is Medicare Advantage? Medicare Advantage is a type of health insurance plan that provides Medicare benefits through private insurers. It includes coverage for hospital and medical services, often with additional benefits.

- Can I see any doctor with Medicare Advantage? Not always. Most Medicare Advantage plans have network restrictions. You may need to see doctors within your plan’s network to receive full benefits.

- What should I do if my care is denied? You have the right to appeal any denial. Gather documentation and consider involving your healthcare provider to strengthen your case.

Understanding these common questions can help beneficiaries feel more confident in their choices regarding Medicare Advantage and ensure they are making informed decisions about their healthcare.

Murder and Fraud in Medicare Advantage Read More »